This post may contain affiliate links, which means I may receive a commission for purchases made through the links. I will only recommend products that I have personally used! Learn more on my Disclosure page!

Sailboat insurance cost reflects the price you pay each year to protect your boat against damage, liability, and unexpected losses. It varies based on your boat, your experience, and the waters you sail, so two owners with similar boats can see very different premiums. Imagine a squall shoving you off a mooring into a neighboring hull or a stray log chewing up your rudder at dusk. Those moments turn into invoices fast. Here is a clear, practical look at what shapes premiums in 2025, the coverage types that matter, how to trim costs, and the smart steps to pick a policy that fits your boat and your plans.

Online Boat Insurance Calculator

What Is the Average Cost of Sailboat Insurance?

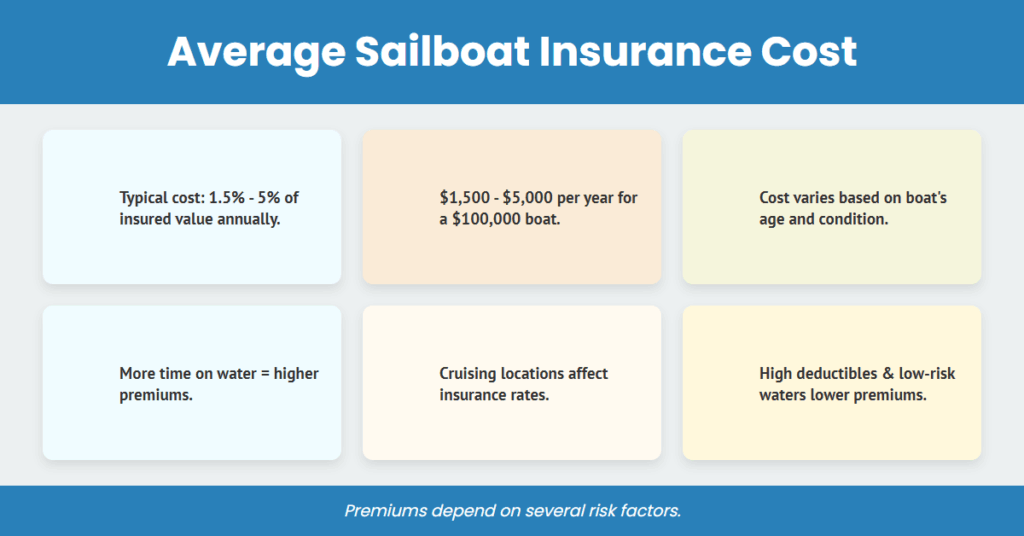

The average sailboat insurance cost usually falls between 1.5 percent and 5 percent of your insured value per year. In plain numbers, a boat insured for 100,000 dollars often runs 1,500 to 5,000 dollars annually. That range tightens or widens based on your boat’s age and condition, your time on the water, and the places you cruise. Policies that only carry liability sit at the lower end, while broad coverage with high limits, low deductibles, and storm protections drive the figure higher.

How to File a Boat Insurance Claim for Hurricane Damage: Securing Peace After the Storm

Here is how that plays out in the real world.

- A thirty five foot cruiser on the Chesapeake with an experienced owner and a clean history can land around 2,000 dollars per year with reasonable deductibles.

- A brand new forty five foot performance cruiser roaming the islands through hurricane season often draws premiums well above 5,000 dollars.

- Owners who carry higher deductibles and sail in lower risk waters like the Great Lakes often see premiums trend toward the lower band.

Coverage Types You Are Likely to See

Every sailboat policy is built on a few core pillars. Liability covers damage or injuries you cause, hull coverage protects your boat, and uninsured or underinsured boater coverage helps if the other skipper carries little or no insurance. Beyond that, policies layer in extras such as towing, hurricane haul out, medical payments, personal effects, and more.

Liability Coverage

Liability coverage pays for injuries or property damage you cause to others, and many marinas insist on it. Typical limits sit between 300,000 and 500,000 dollars, and higher limits are available for owners with more assets at stake. Picture easing into a tight slip in Newport Harbor, a gust shoves your bow, and you tap a neighbor’s topsides. The sound of gelcoat cracking is small, but the bill is not. Liability helps with repair costs and legal fees tied to covered incidents. Skippers who race or host many guests often lift limits to 500,000 dollars or 1 million dollars for added protection.

Hull Coverage

Hull coverage pays to repair or replace your boat after covered losses such as collision, storm damage, fire, vandalism, or sinking. That gut punching crunch of fiberglass meeting an unmarked rock ledge becomes a repair order, and hull coverage steps in after your deductible. Many owners carry a deductible of 1,000 to 2,500 dollars, though higher deductibles drop premiums. You will see two valuation methods most often. Agreed value pays the full insured amount for a total loss, while actual cash value factors in depreciation and usually costs less upfront but pays less after a loss.

Uninsured and Underinsured Boater Coverage

Uninsured and underinsured boater coverage pays your losses if a careless skipper with no policy or too little coverage hits you. It fills a gap that too many owners discover only after the damage is done. Struck at anchor at dusk by a runabout that speeds away, you are left with a bent pushpit and a cracked rudder bearing. Without this coverage, those repairs can land squarely on your tab. With it, you are not left chasing a ghost.

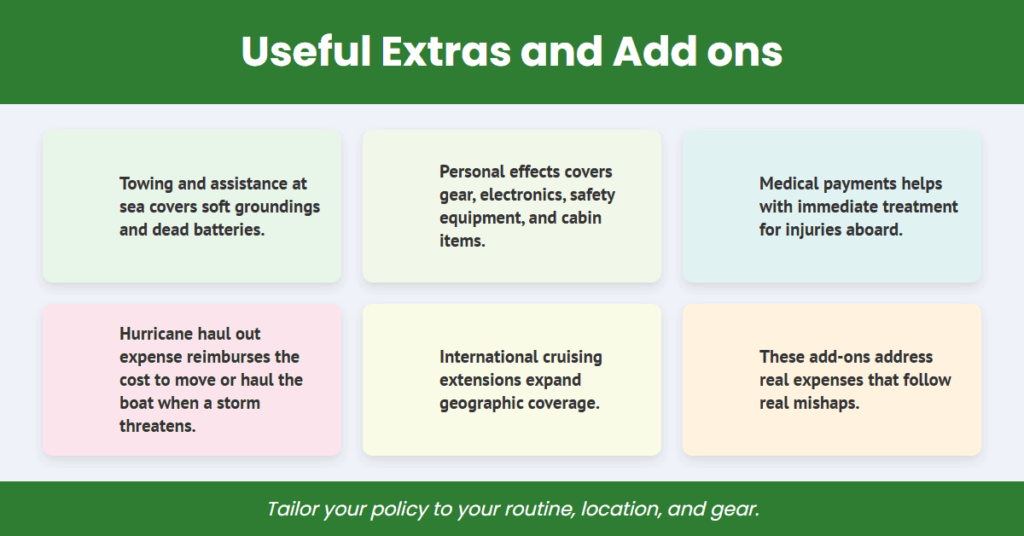

Useful Extras and Addons

These add ons tailor a policy to your routine, location, and gear. They are not fluff. They address real expenses that follow real mishaps.

- Towing and assistance at sea covers soft groundings and dead batteries that lead to tow bills. A single long tow can run four figures.

- Personal effects covers your gear such as electronics, safety equipment, and even cabin items like dishes or bedding within set limits.

- Medical payments helps with immediate treatment for injuries aboard, even for a friend who slips on a rain slick deck.

- Hurricane haul out expense reimburses part of the cost to move the boat to a safer yard or haul it when a named storm threatens. In Miami and the Florida Keys, this one matters during late summer and fall.

- International cruising extensions expand the geographic area to cover visits to places like the Bahamas, Bermuda, or the Caribbean, often with conditions on storm season plans.

What Drives Premiums Up or Down

Premiums reflect risk. Newer and higher value boats cost more to insure, experience helps, and storm prone waters raise rates. Deductible levels and coverage limits matter as well, along with discounts for training and clean histories. The insurer reads your story across all these details, then prices the policy to match.

Boat Value and Age

Higher value boats demand bigger checks to repair or replace, so premiums climb as value climbs. Age can cut both ways. An older but well kept thirty year old cruiser with records and a strong survey can rate favorably, though tired systems and deferred maintenance push costs the other direction. Many carriers ask for a recent marine survey once a boat reaches a certain age, and a thorough survey from a respected surveyor often runs several hundred to around 1,000 dollars. A five hundred thousand dollar performance cruiser in pristine shape naturally draws a higher premium than a twenty five year old cruiser valued at fifty thousand dollars.

Experience and History

Time at the helm matters. A seasoned owner with documented training and a clean record is seen as lower risk. New sailors or owners with recent claims tend to pay more for the same boat and waters. A long time skipper who knows the fog banks and currents of the Pacific Northwest is a different risk profile than someone fresh from a weekend course. Even minor claims can echo in renewal pricing for a few seasons.

Cruising Area

Where you keep and use the boat matters as much as what you sail. The Caribbean, South Florida, and the Gulf Coast carry elevated storm exposure during long parts of the year, so premiums reflect that. The Great Lakes, many inland reservoirs, and certain protected sounds tend to come in lower. A boat spending peak storm months in Grenada or the Virgin Islands will be rated differently than the same model living on Lake Tahoe or Lake Champlain. Some policies ask for a named storm plan or impose location limits during hurricane season.

Deductibles

Higher deductibles lower premiums and shift more of the early cost of a claim to you. The trick is to set a number you can pay comfortably after a rough day. Many owners land at 1,000 to 2,500 dollars as a workable middle ground. Raising a deductible from 500 to 2,500 dollars usually trims the annual premium meaningfully, though exact savings vary.

Coverage Limits

Higher limits cost more but guard against large losses that can liquidate savings or invite legal headaches. Liability at 300,000 dollars is common, but many owners move to 500,000 dollars or even 1 million dollars for peace of mind. Hull limits equal your agreed value amount or, in actual cash value policies, reflect depreciation. Owners with racing schedules, offshore plans, or frequent guest lists often lift both liability and medical payments limits.

Discounts That Actually Help

Discounts exist, and they are worth chasing thoughtfully. Training courses, clean claims histories, layup periods, and multi policy bundles all move the needle.

- Approved training from groups such as US Sailing or the Coast Guard Auxiliary often reduces premiums.

- A steady claim free stretch can unlock loyalty credits over time.

- Declaring a winter layup period if you pull the boat ashore for several months usually trims cost for that timeframe.

- Bundling your home, auto, and boat with the same company can bring a multi policy discount.

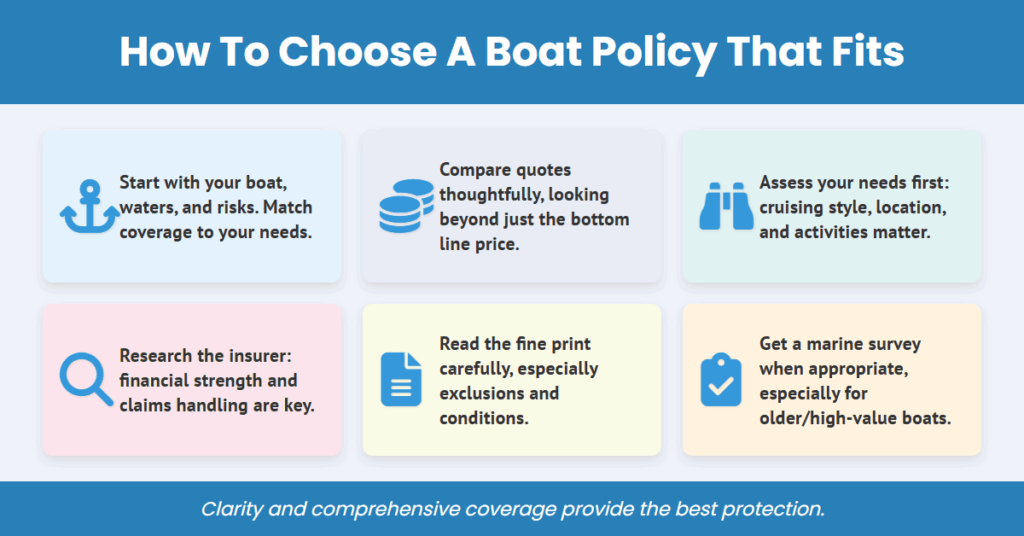

How To Choose A Policy That Fits

Start with the boat you own, the waters you frequent, and the risks you truly face. Then match coverage, deductibles, and limits to your tolerance for out of pocket cost and your appetite for protection. Price matters, but claims service and clarity of terms matter too. Cheap can turn expensive after the first denied claim.

Assess Your Needs First

Clarity here saves money and future stress. Are you a weekend cruiser on inland lakes or a liveaboard pointing toward bluewater passages. Do you race. Do you host large crews. Your answers shape the right liability limits, hull valuation method, and endorsements. A coastal cruiser in the Carolinas that sits ashore for the winter needs a different setup than a seasonal racer in San Diego.

Compare Quotes Thoughtfully

Gather quotes from multiple marine friendly insurers and look beyond the number at the bottom. The cheapest premium often comes with narrower coverage, higher deductibles, or geographic limits that do not match your plans. Compare valuation method, towing limits, hurricane haul out terms, salvage coverage, and named storm clauses. Put the policies side by side and ask where each one shines and where it is thin.

Research The Insurer

Financial strength and claims handling track record matter the day you need help. Look for carriers with strong ratings and solid reputations among boaters in your region. Talk to dock neighbors, yard managers, and sailing clubs. A low premium loses its charm if the company drags through repair approvals or disputes clear losses.

Read The Fine Print

Exclusions and conditions deserve a slow, careful pass. Wear and tear, corrosion, manufacturer defects, and lack of maintenance are common exclusions. Geographic zones, racing exclusions, and storm season requirements can surprise owners who skim. A slow leak from a tired thru hull might be excluded, while a collision induced breach is covered. Know where the lines are drawn.

Get A Marine Survey When Appropriate

Older boats and higher value vessels benefit from a current survey that documents condition and market value. Surveys help set appropriate insured value and give underwriters confidence in seaworthiness. A thorough survey examines hull and deck moisture, standing and running rigging, electrical systems, fuel systems, steering, and safety gear. That report can prevent headaches at claims time since it creates a baseline.

Table 1. A Sample Comparison Of Three Providers

Below is a simple example that shows how different carriers can structure similar policies. The numbers are illustrative and help you see how features trade off against price.

| Feature | Company A | Company B | Company C |

|---|---|---|---|

| Estimated Annual Premium | 2,500 dollars | 3,000 dollars | 2,200 dollars |

| Liability Limit | 500,000 dollars | 500,000 dollars | 300,000 dollars |

| Hull Valuation | Agreed Value | Replacement Cost | Actual Cash Value |

| Hull Deductible | 1,000 dollars | 1,500 dollars | 2,000 dollars |

| Hurricane Coverage | Included with conditions | Available for extra premium | Unavailable in high risk zones |

Key Factors That Shape Cost At A Glance

The next table summarizes how the usual suspects move premiums. Bigger values and higher risk zones raise costs, while higher deductibles and training can help bring them down.

Table 2. Factors That Influence Sailboat Insurance Cost

| Factor | Effect On Premium | Example |

|---|---|---|

| Boat Value | Higher value increases premium | Two hundred thousand dollars costs more to insure than fifty thousand dollars |

| Experience | Less experience increases premium | New sailor pays more than a veteran |

| Cruising Area | Higher risk waters increase premium | Caribbean costs more than Great Lakes |

| Deductible | Higher deductible lowers premium | Two thousand five hundred dollar deductible costs less than five hundred dollars |

| Coverage Limits | Higher limits increase premium | One million dollar liability costs more than three hundred thousand dollars |

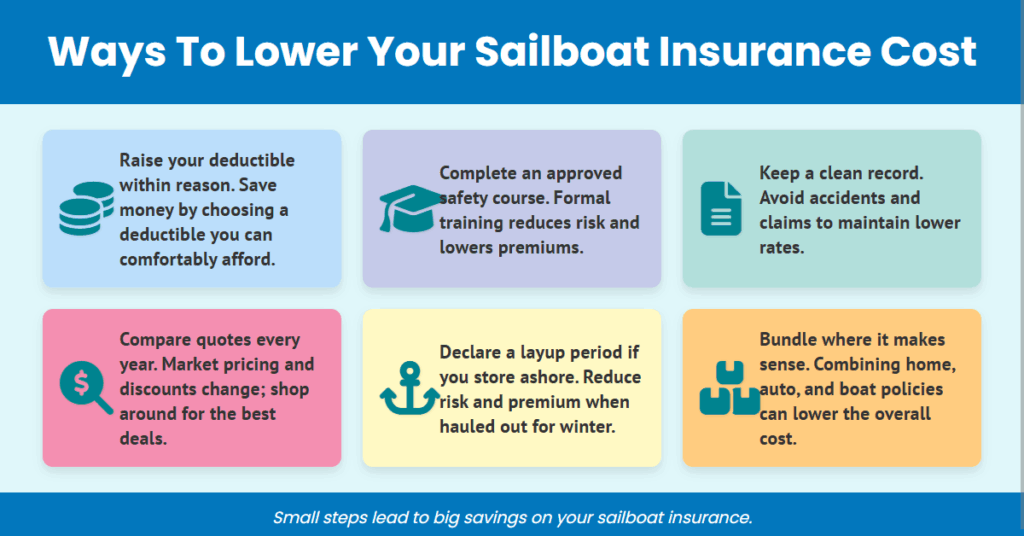

Ways To Lower Your Sailboat Insurance Cost

You can reduce premium outlay without gutting protection. The most reliable levers are deductibles, training, clean records, smart storage, and regular quote checks. Each step helps a little, and together they add up.

- Raise your deductible within reason

A higher deductible lowers annual cost, as long as you choose a number you can pay comfortably after a mishap. Many owners move from 500 dollars to 2,500 dollars and pocket a noticeable annual savings. - Complete an approved safety course

Formal training shows commitment and reduces risk, and many carriers reward it. Courses from US Sailing or the Coast Guard Auxiliary are widely recognized. - Keep a clean record

Accidents and claims follow you for a few seasons. Slow down in tight marinas, verify charts and tides, check rigging, and log maintenance so small issues do not balloon into claims. - Compare quotes every year

Market pricing changes, underwriting appetite shifts, and new discounts appear. A yearly round of quotes keeps your policy sharp and honest. - Declare a layup period if you store ashore

Owners who haul out for winter or long maintenance cycles can tag those months for reduced risk and reduced premium. Be sure your policy spells out what is allowed during layup. - Bundle where it makes sense

Placing home, auto, and boat with the same company can push the price down. Just confirm coverage quality stays high across the bundle.

Closing Thoughts

Sailboat insurance cost sits between 1.5 percent and 5 percent of insured value for most owners, and your position in that band reflects your boat, your skills, your waters, and your policy choices. The right coverage is the one that pays promptly for the losses you are most likely to face without draining your savings in premium. Gather fresh quotes, set deductibles you can live with, lift limits to guard your assets, and confirm storm season terms align with your plans. Ask about training discounts, layup credits, and towing limits. A few calls now can save a season later.

Frequently Asked Questions

How is sailboat insurance cost calculated?

It is based on boat value, age, where you sail, your experience, your claims record, coverage limits, and deductibles. Insurers weigh these factors to estimate risk and set a price. Newer and higher value boats cost more to repair, storm zones bring higher loss odds, and seasoned skippers with training and clean records often pay less. Deductibles and valuation method matter as well, since agreed value and low deductibles increase premium.

What does a typical sailboat policy cover?

Most policies include liability, hull coverage, and uninsured or underinsured boater coverage. These protect other people and property, your own boat, and you in hits with poorly insured skippers. Many owners add towing, medical payments, personal effects, and hurricane haul out. Offshore or international cruising may require a geographic endorsement.

How can I lower my premium without losing key protection?

Raise deductibles to a level you can handle, complete recognized training, compare quotes each renewal, bundle policies, and use layup periods if you store ashore. These steps reduce cost while keeping core protection in place. Maintenance logs, claims discipline, and a clear storm plan help too.

Is sailboat insurance mandatory?

State rules differ and marinas set their own requirements, but many marinas require liability coverage to dock or moor. Some states tie insurance to registration status for certain boats. Even where it is not mandated, carrying liability and hull coverage protects your assets and your boating life.

What is the difference between agreed value and actual cash value?

Agreed value pays the insured amount for a total loss and does not deduct for depreciation, while actual cash value factors in depreciation and usually costs less per year. Owners of newer or higher value boats often choose agreed value to avoid tough depreciation math after a major loss. Owners of older boats sometimes pick actual cash value to lower annual cost, knowing payout will be reduced if the worst happens.