This post may contain affiliate links, which means I may receive a commission for purchases made through the links. I will only recommend products that I have personally used! Learn more on my Disclosure page!

Houseboat insurance without a survey is coverage issued for a vessel without requiring an official marine survey or condition inspection. In most cases, insurance companies insist on such a report before they offer policy terms for large personal watercraft. The survey is their equivalent of a technical health check. It tells the insurer exactly what they are agreeing to cover. Yet there are situations in which you can secure insurance for a houseboat without presenting this formal document.

Houseboat Insurance Calculator

Some owners find themselves in this bind after buying an older vessel where the seller did not have recent survey results. Others live far from major marine surveyors and cannot schedule an inspection easily. Still others may be dealing with smaller houseboats or low value crafts where the cost of a survey feels disproportionate.

In this full guide we will explore:

- Why insurers normally require a survey.

- When exceptions can be made.

- How insurers evaluate risk without a survey.

- Strategies to improve your chances of getting coverage without one.

- Risks and trade-offs involved in skipping the survey.

Why Insurers Usually Require a Survey

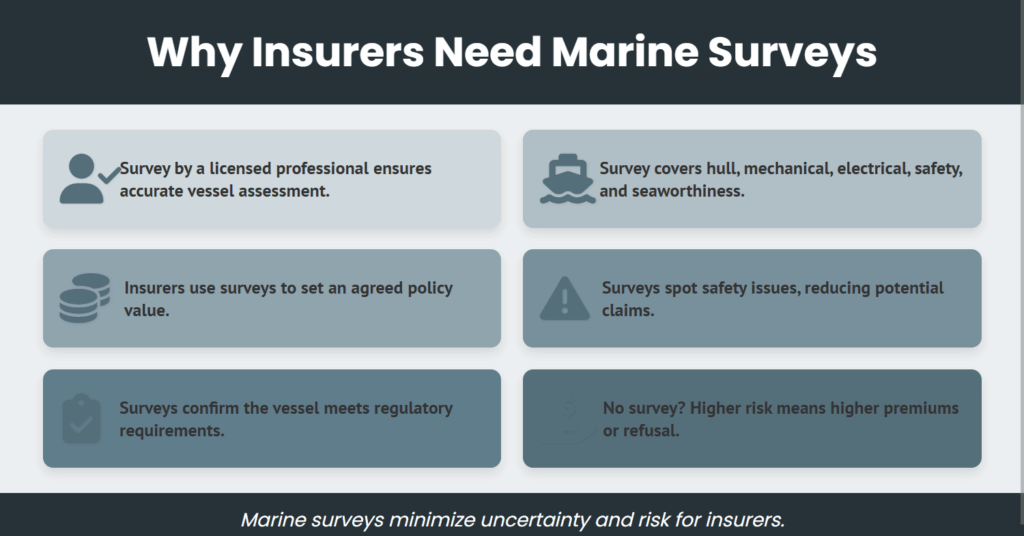

A marine survey is conducted by a licensed or accredited professional, often someone recognized by organizations like the Society of Accredited Marine Surveyors or the International Institute of Marine Surveying. For a houseboat, the survey covers hull integrity, mechanical systems, electrical wiring, safety gear, and overall seaworthiness.

Insurers rely on this document to:

- Set an agreed value for the policy.

- Spot safety issues that could lead to claims.

- Confirm the vessel meets regulatory requirements.

Without a survey, the insurer has to guess at the vessel’s condition. That introduces uncertainty. In the world of underwriting, uncertainty is simply another word for higher risk. Higher risk either raises premium prices or leads to outright refusals.

The Circumstances Where No Survey Policies Exist

Even with the usual procedure, there are cases where insurers write houseboat insurance without requiring a survey, especially when risk factors align in their favor.

Here are the most common exceptions:

- New Houseboats Bought from Licensed Dealers – A factory fresh boat purchased from a reputable seller often comes with manufacturer specs, build certificates, and warranty documents. These can act as a substitute for a survey in the eyes of insurers.

- Small or Low Value Houseboats – For craft under certain size or value limits, some companies will skip the survey requirement entirely. A ten thousand dollar older pontoon houseboat in a freshwater marina may qualify where a two hundred thousand dollar liveaboard would not.

- Existing Customers with History – If you already insure other boats with the company and have a strong claims-free history, your relationship may persuade them to underwrite a policy without new inspection paperwork.

- Renewals with No Changes – If you are simply renewing an existing policy on the same boat with no modifications or claims, you may avoid a fresh survey requirement for another term.

- Short Term Policies – Occasionally insurers offer temporary coverage of thirty to ninety days without a survey, expecting the owner to provide one later.

How Insurers Assess Risk Without a Survey

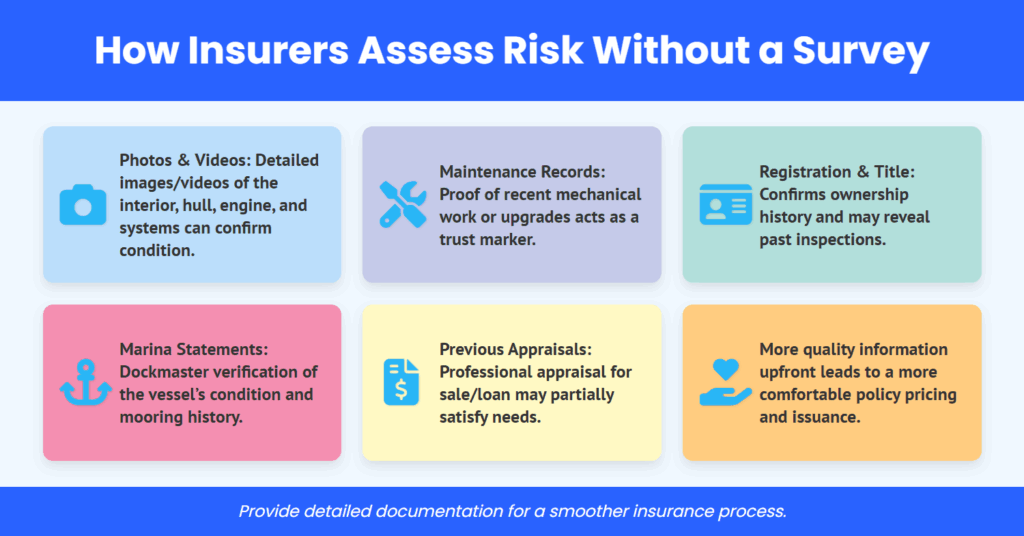

Without a survey report, the underwriter turns to other data sources to judge whether they feel good about covering the houseboat.

- Photos and Videos: They may request detailed images of the interior, hull, engine, and safety systems. Videos of the boat running or docked can help confirm condition.

- Maintenance Records: Documented proof of recent mechanical work or upgrades can act as a trust marker.

- Registration and Title: Confirms ownership history and may reveal documentation of past inspections.

- Marina Statements: A letter from the dockmaster verifying the vessel’s condition and mooring history can have influence.

- Previous Appraisals: Even if not a formal survey, a professional appraisal conducted for sale or loan purposes may partially satisfy their needs.

The more quality information you give them up front, the more comfortable they can feel pricing and issuing the policy.

Trade-offs in Skipping the Survey

Securing insurance without a survey may be possible, but it comes with consequences.

- Limited Coverage: Some insurers will only offer liability protection without physical damage coverage until a survey is provided. That means your hull is uninsured against damage or loss.

- Higher Premiums: Lack of inspection results makes them price in a perceived risk buffer.

- Lower Payout Confidence: In the event of a claim, disputes over preexisting damage become more common. Without a survey baseline, it can be harder to prove the damage was new.

- Value Limits: Very high value boats almost always need a survey. Without one, you may face strict caps far below replacement cost.

Improving Your Approval Chances Without a Survey

If you genuinely cannot arrange a survey right away, you can still present yourself as a low risk client.

- Prepare Detailed Documentation

Collect receipts for repairs, professional inspections of components like the engine, and photographs from multiple angles. Include the vessel name and registration number in each image for authenticity. - Highlight Safety Equipment

List all lifejackets, fire extinguishers, navigation lights, alarms, and other gear onboard. Safety focus can influence underwriters positively. - Choose the Right Insurer

Search for companies known to insure older or unique watercraft. Regional marine insurers may be more flexible than national carriers with rigid frameworks. - Offer a Temporary Condition Agreement

Propose a short term coverage term with the understanding that a formal survey will follow at renewal. This shows willingness to comply within reasonable limits. - Leverage Existing Relationships

If you have home, auto, or other marine coverage through a company, ask them directly for accommodation on the houseboat. Loyalty can nudge decisions.

Why Some Owners Intentionally Avoid Surveys

While cost is an obvious reason, there are other motivations. A poor survey report can lower resale value or force repair work before an insurer will bind coverage. Older boats that have been maintained by owners without professional oversight sometimes include noncompliant modifications. These can be red flags in formal reports.

By skipping the survey, an owner delays potential conflicts. That said, this is a short sighted approach. Insurers are still within their rights to inspect the vessel at claim time, and undisclosed issues could jeopardize payouts.

Case Example: Freshwater Pontoon Houseboat

Consider a 28 foot pontoon houseboat used seasonally on a private lake with no commercial activity. The owner keeps it in covered dry storage and uses it only in summer weekends. The value is under fifteen thousand dollars. The insurer sees that loss exposure is relatively low. With photos, maintenance receipts, and proof of sheltered storage, they agree to provide agreed value coverage without a survey.

The key factors were low replacement cost, protected environment, and transparent owner records.

Case Example: Luxury Liveaboard Houseboat

Now picture a 55 foot custom built luxury houseboat moored year round in a tidal marina. The vessel includes multiple staterooms, twin diesel engines, and a market value above three hundred thousand dollars. An insurer in a regulated market will categorically require a recent survey here. The risks in both liability and hull damage are too large to underwrite without detailed inspection.

In such a case, attempting to bypass the survey is impractical and will likely result in refusals or offers with extremely limited coverage.

Regulatory Variations in Survey Requirements

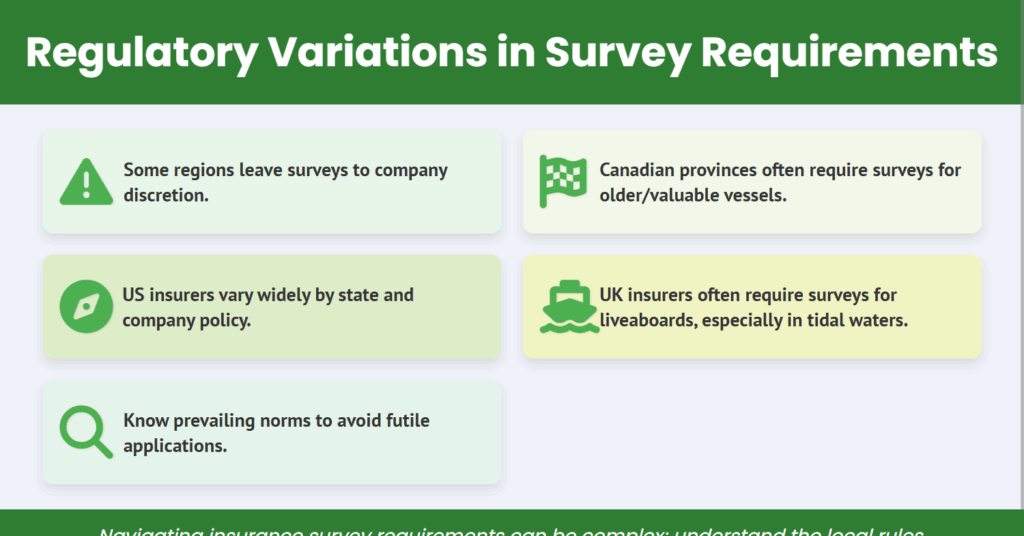

In some regions, insurance regulation does not directly demand a survey but leaves it to company discretion. In others, like certain Canadian provinces, surveys are standard procedural practice once a vessel hits a certain age or value threshold. United States insurers vary widely by state and by company policy. UK insurers tend toward formal surveys for liveaboards, especially on tidal waters.

In every market, knowing the prevailing norms helps you avoid wasting time applying where approval is impossible.

Long Term Benefits of Having a Survey Anyway

Even if your current goal is coverage without one, a good survey benefits the owner. It can identify maintenance needs early, improve resale prospects, and create a baseline in case of damage. It also gives you negotiating power on premium rates since a clean report reduces risk perception.

Many seasoned boat owners commission surveys every three to five years not only for their insurer but for their own operational safety.

Conclusion

Houseboat insurance without a survey is possible in specific situations. New low value purchases, strong existing relationships with insurers, or short term provisional policies are the most common pathways. Success in getting coverage relies on proving low risk through detailed documentation, photographs, and evidence of responsible ownership.

While avoiding the survey might save time or money now, it can limit coverage options and create challenges during claims. If your vessel is high value, complex, or moored in an environment with greater hazards, expect the survey requirement to be firm.

For peace of mind and long term asset protection, think of the survey not as a bureaucratic hurdle but as an investment in both your safety and your insurance security.

Frequently Asked Questions

Can I get full coverage on my houseboat without a survey

Yes in rare instances, usually for low value or new vessels. Many insurers will restrict coverage to liability only until a survey is provided.

Will my premiums be higher without a survey

They often are because the insurer prices in uncertainty.

Can photos replace a survey for insurance purposes

They can help an underwriter make a decision but rarely replace a survey for high value boats.

Do lenders require surveys for financed houseboats

Almost always. Loan approval generally depends on a current marine survey regardless of insurance.

What if my state has no survey requirement

Company policy still controls, so you must meet their underwriting terms even if the state has no mandate.