This post may contain affiliate links, which means I may receive a commission for purchases made through the links. I will only recommend products that I have personally used! Learn more on my Disclosure page!

Commercial boat insurance is a specialized policy that protects businesses using vessels for income. It systematically covers three critical areas: physical damage to your boat itself, your legal liability for injuries to passengers or damage to others’ property, and specialized risks like commercial towing, crew injuries, and environmental cleanup from fuel spills. This coverage acts as a financial anchor, securing your maritime business against the unique perils of operating on the water.

It is the anchor that keeps your enterprise secure amidst the uncertainties of maritime commerce. This guide will provide a clear and detailed understanding of commercial boat insurance coverage, empowering you to make informed decisions that protect your aquatic business.

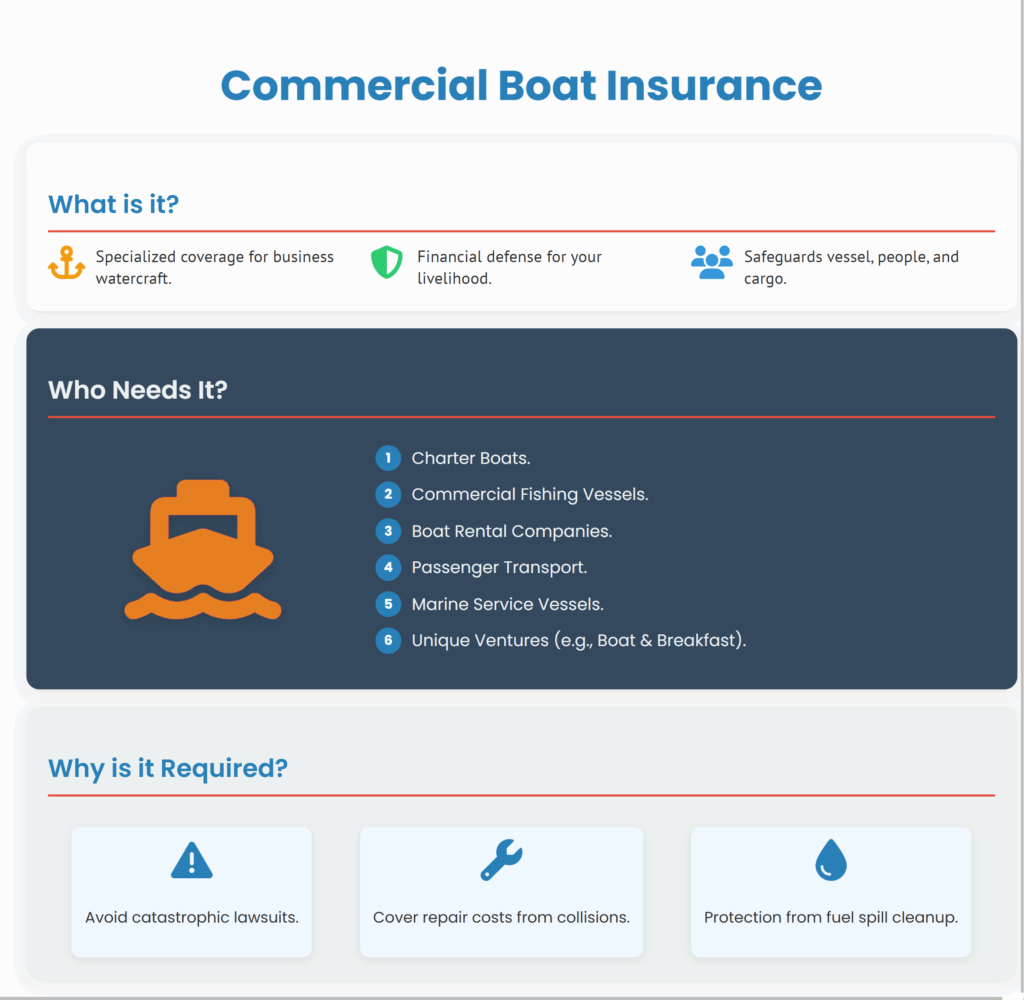

What Is Commercial Boat Insurance and Who Requires It?

Commercial boat insurance is a specialized type of coverage designed specifically for watercraft used in business operations. Unlike personal boat insurance, which is for pleasure cruising, this protection is built for the unique risks you face when your vessel is your workplace. It is a financial defense for your livelihood, engineered to safeguard three core elements: the vessel itself, the people on board, and the products or cargo you transport.

Any business that uses a vessel to generate revenue needs this specialized policy. The scope is broad, covering a diverse fleet of maritime enterprises :

- Charter Boats: Including fishing guides, sightseeing tours, and dinner cruises.

- Commercial Fishing Vessels: From small inshore boats to large offshore trawlers.

- Boat Rental Companies: Ranging from small pontoon boats to peer-to-peer rental platforms.

- Passenger Transport: Such as water taxis and ferries.

- Marine Service Vessels: Including tugboats, barges, dredgers, and boats used for research or environmental work.

- Unique Ventures: Like “boat and breakfast” operations or underwater tourist submarines.

Operating without this coverage exposes you to profound financial risk. Imagine a scenario where a passenger is injured, your boat is damaged in a collision, or a fuel spill occurs. The costs from lawsuits, repairs, and environmental cleanup can be catastrophic. Furthermore, many marinas, lenders, and business partners will require you to show proof of insurance before they allow you to dock, finance a vessel, or commence operations.

The Essential Components of Your Policy

A commercial boat insurance policy is not a single, monolithic product. It is a coordinated package of several coverages, each designed to protect a different part of your business. Understanding these components is the first step in building your financial lifeline.

Hull and Machinery Coverage

This is the foundation of your policy, the part that protects the physical assets of your business. Hull coverage addresses damage to the boat itself, including the hull, machinery, and permanently installed equipment. It acts as a shield against perils like storms, fire, theft, collision, or sinking. When you select this coverage, you will encounter a critical choice that defines your financial protection in the event of a major loss.

| Feature | Agreed Value Policy | Actual Cash Value (ACV) Policy |

|---|---|---|

| Basis of Payout | Pre-agreed value set at policy inception | Market value at the time of loss, accounting for depreciation |

| Total Loss Payout | Full agreed value, no deduction for depreciation | Replacement cost minus depreciation |

| Partial Loss Payout | Typically “new for old” replacement, less deductible | Cost of repair minus depreciation for parts, less deductible |

| Premium Cost | Higher | Lower |

| Best For | Newer vessels, high-value boats, or owners wanting predictable payouts | Older vessels or owners seeking a lower-premium option |

Protection and Indemnity (P&I) Liability

While hull coverage protects your vessel, Protection and Indemnity (P&I) protects your assets from your legal liabilities to others. This is arguably the most critical component for any commercial operator. P&I provides broad liability coverage for situations including :

- Bodily Injury: Medical expenses, lost wages, and legal fees if a passenger, crew member, or someone on another boat is injured due to your operations.

- Property Damage: The cost to repair or replace a dock, another vessel, or any other property damaged by your boat.

- Wreck Removal: The significant expense of removing your sunken or damaged vessel if it becomes a hazard to navigation.

- Cargo Liability: Damages related to the loss or damage of cargo being transported on your vessel.

Crew Coverage

Your crew faces a high-risk work environment every day. The commercial fishing industry, for instance, has a fatality rate 29 times the national average. Crew coverage, often structured as Jones Act coverage or Maritime Employers Liability (MEL), is designed to protect you from liabilities to your employees under federal maritime law. It protects your legal liability if a crew member is injured or becomes ill in the course of their work. It is essential to recognize that this differs from a standard state workers’ compensation policy, which typically does not apply to seamen.

Pollution Liability

As a vessel operator, you are a steward of the marine environment. An accidental discharge of fuel or oil can lead to devastating cleanup costs and substantial fines. The Oil Pollution Act of 1990 currently sets a statutory liability limit of nearly $940,000 for these incidents. Pollution liability coverage helps cover the costs of containment, cleanup, and third-party claims arising from a sudden and accidental spill . Many marinas now require proof of this coverage before granting a slip.

Additional Crucial Coverages

Beyond the core components, several other coverages address specific risks and can be tailored to your precise operations.

- Commercial Towing and Assistance: Breakdowns happen far from port. This coverage, sometimes called emergency towing, reimburses you for the cost of towing, fuel delivery, or emergency labor when your vessel is disabled. Some providers, like BoatUS, offer unlimited towing plans for a small additional fee.

- Uninsured/Underinsured Boater Coverage: Not every boater carries adequate insurance. This protection covers injuries to you and your passengers if you are hit by a boater who has little or no liability insurance.

- Marine Cargo and Equipment: This safeguards the goods you are paid to transport and the specialized, mobile tools of your trade, fishing nets, dive gear, scientific instruments, whether they are on board, in transit, or stored ashore.

- Business Interruption: When your vessel is damaged and out of service, your revenue stream stops. This coverage can help replace lost income and cover fixed expenses during the repair period, helping you weather the financial storm.

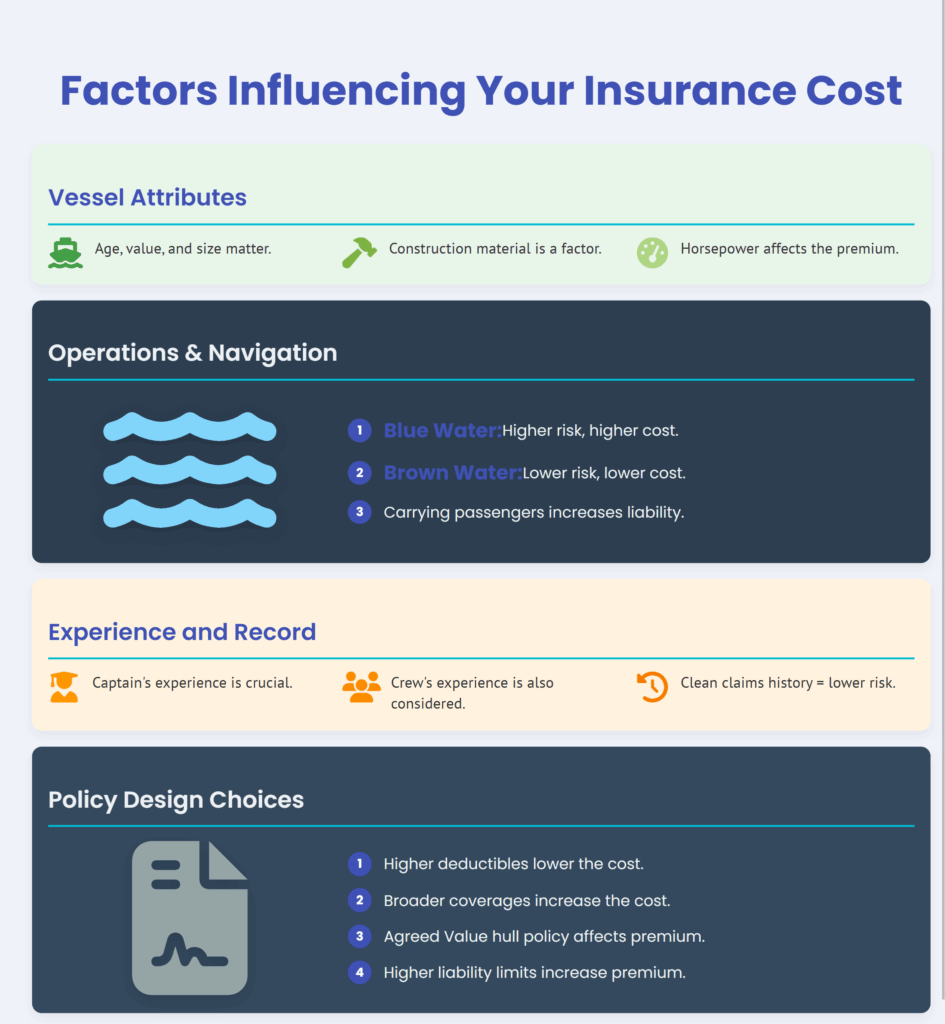

What Factors Influence Your Insurance Cost?

The price of your policy is as unique as your business. Insurers assess a variety of factors to determine your premium, which typically falls between 1% and 5% of your vessel’s insured value each year.

- Vessel Attributes: The age, value, size, construction material, and horsepower of your boat are primary factors. A newer, more expensive vessel will cost more to insure than an older, simpler one.

- Operations and Navigation Limits: What you do and where you go matters profoundly. A fishing boat operating in the open ocean (“blue water”) faces greater risks and higher costs than a tour boat in a calm, sheltered bay (“brown water”). Carrying passengers for hire generally increases liability premiums compared to carrying cargo.

- Your Experience and Record: Your history as a captain, along with the experience of your crew and your business’s claims history, plays a significant role. A clean record demonstrates lower risk.

- Policy Design: The choices you make directly impact your premium. Higher deductibles will lower your cost, while opting for broader coverages like an Agreed Value hull policy or higher liability limits will increase it.

Commercial vs. Personal Insurance: A Critical Distinction

Attempting to run a commercial operation under a personal boat insurance policy is a recipe for financial disaster. The two are fundamentally different.

| Feature | Commercial Boat Insurance | Personal Boat Insurance |

|---|---|---|

| Purpose | Revenue-generating business | Recreational pleasure use only |

| Liability Limits | High (designed for crew, passengers, cargo) | Lower |

| Covered Parties | Paying passengers, employees, commercial cargo | Family and friends |

| Policy Cost | Higher, reflecting greater risks | Lower |

Personal policies almost universally exclude commercial use. If you are running charters or fishing commercially and have an accident, a personal policy will almost certainly deny the claim, leaving you to bear the full financial burden.

Specialized Policies for Maritime Businesses

For businesses that support the maritime industry without necessarily owning vessels, related policies exist.

- Marine General Liability (MGL): This protects land-based marine businesses like marina operators, boat dealers, ship repairers, and marine contractors from shoreside liabilities, such as a customer slipping on a dock or damage to a boat in their care, custody, or control.

- Bumbershoot Insurance: This is a marine umbrella policy that provides excess liability coverage over both marine and non-marine underlying policies. It offers an extra layer of protection for businesses with significant exposures.

Frequently Asked Questions

What is the difference between “blue water” and “brown water” hull coverage?

This distinction refers to your vessel’s primary operating area. “Blue water” coverage is for the deep, open ocean, involving longer voyages and international travel. It accounts for more challenging conditions and carries a higher premium. “Brown water” coverage is for vessels that operate on rivers, lakes, harbors, and near-shore coastal areas. The risks are different, and premiums for this coverage are generally lower.

Does commercial boat insurance cover my crew under workers’ compensation?

The coverage for crew injuries is handled differently than for land-based employees. Your Protection & Indemnity (P&I) coverage provides vital liability protection for crew members under federal maritime law, specifically the Jones Act. However, this is not a standard state workers’ compensation policy. You may need an additional Maritime Employers Liability (MEL) policy to fully cover your liability for crew injuries, especially if they work on vessels you do not own.

Can I get coverage if I rent my boat out on a peer-to-peer platform?

Yes. The rise of peer-to-peer (P2P) boat rental platforms has been met with specialized commercial insurance products. It is absolutely essential to have this coverage, as your personal policy will not protect you. A specialized policy for P2P rentals is designed to cover physical damage to your boat and third-party liability while it is being rented out.

How much commercial vessel insurance coverage do I need?

The amount of coverage you need is deeply personal to your business. There is no single average. Key variables include your location, operating areas, the number of vessels, your specific operations, claims history, and the number of employees. A professional insurance agent who specializes in marine coverage can help you assess your risks and tailor a policy that provides adequate protection without gaps.

Your business on the water is a testament to your independence and hard work. Protecting it with the right commercial boat insurance is not merely an administrative task; it is an act of stewardship for the enterprise you have built. It grants you the confidence to face the challenges of the maritime world, knowing that you have a strong partner ready to help you weather any storm.