This post may contain affiliate links, which means I may receive a commission for purchases made through the links. I will only recommend products that I have personally used! Learn more on my Disclosure page!

Sit with me for a moment and think about your pontoon. Is it the relaxing stage for family dinners beneath pink skies? Or the floating platform for tubing, swimming, and memories you’ll retell years from now? Whatever role it plays, one thing is universal in 2025: ownership brings costs, and insurance rests squarely at the center.

The cost of pontoon insurance isn’t guesswork anymore. Lenders, marinas, and insurers rely on data, risk models, and detailed histories to price premiums. If you’re wondering how much to budget, let’s untangle the factors that raise or lower your bill.

National Averages in 2025

According to the Insurance Information Institute (2024 data, updated projections for 2025):

- Average pontoon insurance premium nationwide: $275 to $600 per year.

- High‑risk coastal states (e.g., Florida, Louisiana): closer to $650–$1,000 annually.

- Lower‑risk Midwestern states (Minnesota, Michigan): hold steady at $200–$400 annually.

Given that a new pontoon’s price tag averages close to $45,000 today (NMMA 2024), most owners consider insurance cheap compared to repairs or lawsuits.

👉 Want a quick number that matches your own boat, location, and coverage preferences? Try the Pontoon Insurance Calculator to cut straight through averages and see your personal estimate.

Factors That Shape Your Premium

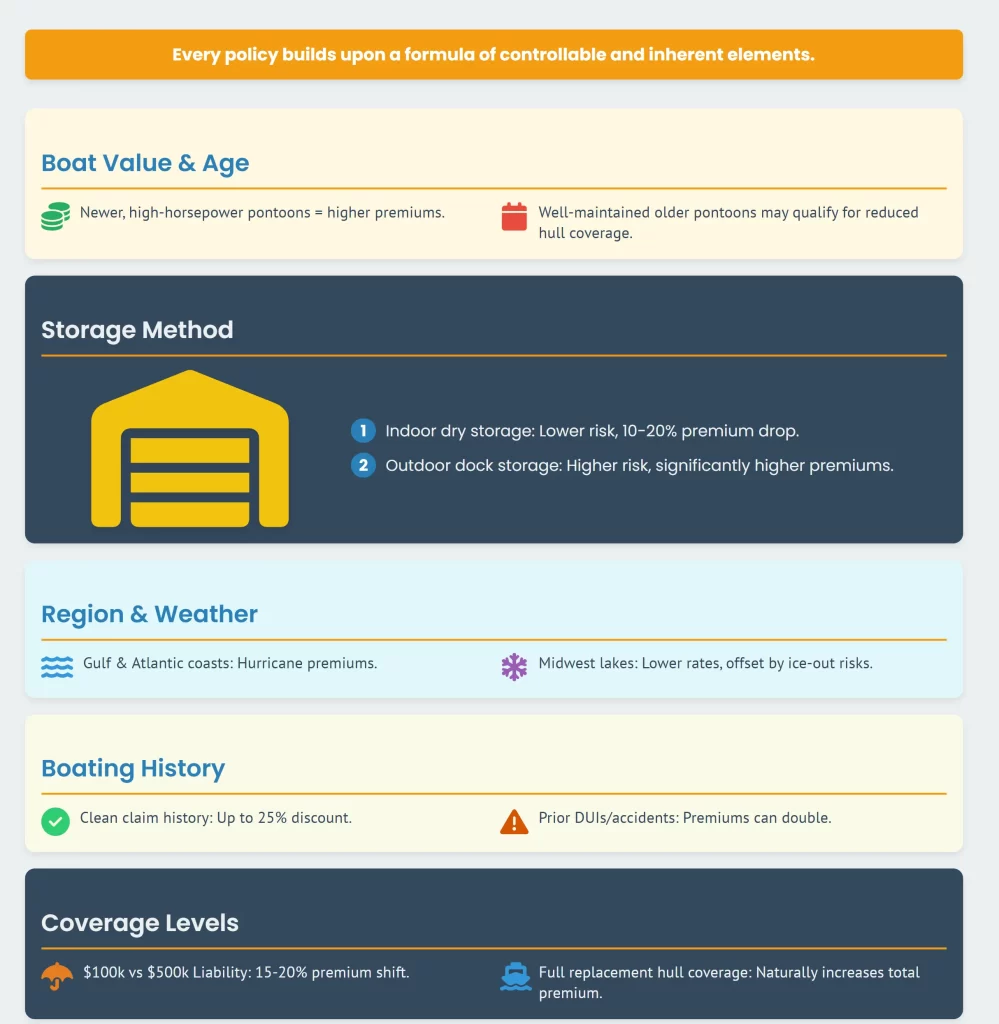

Every policy builds atop a formula. Some elements you control, others you inherit. Together, they decide your annual cost.

1. Boat Value and Age

- Newer pontoons with high horsepower command higher premiums.

- Older pontoons, if well‑maintained, may qualify for reduced hull coverage costs.

2. Storage Method

- Indoor dry storage: Lower risk, premiums drop 10–20%.

- Outdoor dock storage: Higher theft and storm exposure, premiums rise significantly.

3. Region and Weather

- Gulf and Atlantic coasts face hurricane premiums.

- Midwest lakes see lower rates, tempered by ice‑out season risks in spring.

4. Boating History

- Clean claim history yields discounts up to 25%.

- Prior DUIs or accidents can double premiums.

5. Coverage Levels

- Liability at $100,000 vs. $500,000 shifts premiums by an average of 15–20%.

- Hull coverage equal to the full replacement cost naturally increases totals.

Side‑By‑Side Cost Comparisons

| Scenario | Coverage Selected | State | Expected Annual Premium (2025) |

|---|---|---|---|

| Family pontoon, $35,000 hull, $300k liability | Basic liability + physical damage | Minnesota | $300–$420 |

| Luxury twin‑engine pontoon, $85,000 hull, $500k liability | Full coverage + uninsured boater rider | Florida | $750–$1,050 |

| Modest used pontoon, $15,000 value | Liability only | Michigan | $175–$250 |

| Mid‑tier pontoon, $45,000 hull, $300k liability + medical | Expanded coverage w/ riders | Texas | $450–$600 |

These projections reflect state‑level averages and common lifestyle choices.

Lifestyle Choices Save or Spend

Picture two owners:

- Owner A stores the pontoon in a heated barn every winter, installs GPS tracking, and has never filed a claim. Their premium hovers near the low end of the state range.

- Owner B leaves the vessel tied up at a marina through storm seasons, has two prior collision claims, and frequently hosts large groups. Their premiums can double.

The moral? Ownership habits aren’t just maintenance—they’re part of an insurer’s math.

👉 Plugging your storage, claims history, and accessories into the Pontoon Insurance Calculator shows adjustments in real time. Small changes—like opting into GPS discounts—illustrate how lifestyle decisions shape protection.

The Hidden Factor: Inflation in 2025

Boat repair costs climbed 9% over the past 18 months (Bureau of Labor Statistics 2025). Upholstery replacements, engine parts, and skilled labor all spike premiums indirectly, since insurers forecast claim payouts against real repair costs.

It means even if you’ve had no accidents, national repair inflation alone may raise your bill at renewal.

Should You Bundle?

Insurance carriers consistently advocate for bundling. Pair your pontoon with home or auto and discounts of 10–20% appear. While bundling often feels like a marketing tactic, numbers show it produces real savings for households carrying multiple assets.

That extra margin lets you raise liability coverage without feeling the pinch.

Cost of Under‑Insuring

Think shaving down your policy saves money? One pontoon damage claim tells a harsher story. Average collision repair: $8,300 (BoatUS Member Claims, 2024). Even “minor” dock mishaps cross $1,200 quickly.

Medical liability spikes higher. Slip‑and‑fall claims average $18,000, while water sport‑related injuries can climb beyond $80,000. In both cases, dropping coverage levels means facing those numbers directly.

2025 Outlook on Premiums

Industry analysts predict slight upward pressure on premiums through 2026 due to storm frequency and lithium battery adoption on hybrid pontoons. As boating tech evolves, underwriters adapt. Expect your policy to reflect those factors even if your habits remain steady.

Why Clarity Fuels Confidence

Understanding how policy numbers link to premiums isn’t just practical—it’s empowering. When you know how boat value, location, and habits shape costs, you’re no longer subject to “mystery math.” Instead, you choose policies with intention.

The right insurance is less about trimming dollars and more about protecting what truly matters: the people laughing on your deck and the investments tied to your vessel.

👉 If you’d like to shift from generic averages to numbers tailored to your story, use the Pontoon Insurance Calculator now. The inputs are simple, the insights lasting.

References

- National Marine Manufacturers Association (NMMA), Boating Market Data 2024.

- Insurance Information Institute, Average U.S. Boat Insurance Rates, 2024–2025.

- U.S. Coast Guard, Recreational Boating Statistics 2024.

- BoatUS Claims Study, Pontoon Collision Data 2024.

- Bureau of Labor Statistics, Marine Repair Services Inflation Index, 2025.