This post may contain affiliate links, which means I may receive a commission for purchases made through the links. I will only recommend products that I have personally used! Learn more on my Disclosure page!

Picture this: You’re sipping morning coffee on your houseboat’s deck, sunlight dancing on the water, when a neighbor’s runaway dinghy slams into your floating porch. The railings splinter, your custom teak furniture tumbles into the lake, and suddenly, your peaceful oasis feels as fragile as a paper boat. This isn’t just a bad day—it’s a wake-up call. Houseboats aren’t rebellious suburban homes or stubborn yachts. They’re shape-shifters, part cozy cottage, part watercraft, and standard insurance policies treat them like misfits. Welcome to our houseboat insurance guide!

Homeowners’ insurance stares blankly at your floating address. Boat insurance squints at your full-sized refrigerator and queen bed. You need a hybrid guardian—a policy that understands your houseboat moonlights as both a sanctuary and a ship. Let’s unravel why cookie-cutter coverage fails and what actually protects your aquatic haven.

Your Floating Fortress – Must-Have Protections for Houseboat Living

Houseboat insurance isn’t a luxury—it’s a life raft for your wallet. Imagine your policy as a team of bodyguards, each specializing in different threats. Here’s your VIP protection squad:

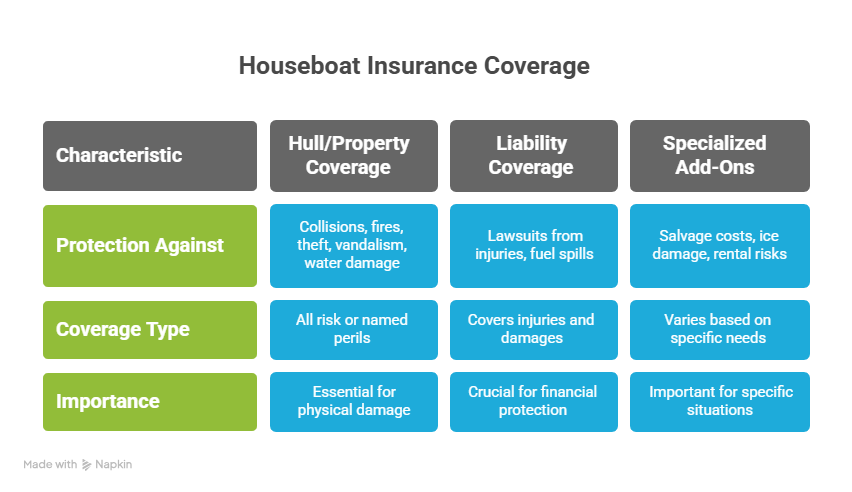

1. The Bouncer (Hull/Property Coverage)

This is your first line of defense against the world’s chaos. When hurricane winds peel off your roof or a tipspeed jet-skier rams your kitchen, hull coverage steps in. But here’s the twist: Unlike your cousin’s sailboat, your floating home has plumbing, wiring, and maybe even a mini-library.

- What it fights: Collisions, fires, theft, vandalism, and water’s sneaky tricks (like electrolysis corroding metal parts).

- The fine print: Policies often split coverage into “all risk” (everything unless excluded) and “named perils” (only listed disasters). Go broad—you never know when a rogue wave will fancy your sunroom.

- Reality check: Marina neighbors once forgot their anchor, letting their houseboat drift into ours during a storm. Hull coverage rebuilt our shattered deck…and their apology casserole helped too.

2. The Shield (Liability Coverage)

Your deck party goes sideways when a guest trips over a mooring line and fractures their wrist. Liability coverage is the friend who handles the awkwardness—and the lawsuit.

- Why it’s non-negotiable: Even cautious owners get sued. A family friend’s dog once knocked a tourist into the harbor from their houseboat porch. The settlement? More than their life savings.

- Coverage sweet spot: $1 million is the new $300k. Hospital bills balloon fast, and legal fees bite harder than a misbehaving propeller.

- Bonus armor: Ensure it covers fuel spills. That 5-gallon diesel leak during refueling? Without coverage, you’re funding the cleanup and the fines.

3. The Guardian Angel (Specialized Add-Ons)

These unsung heroes tackle the “wait, that’s not covered?!” surprises:

- Salvage coverage: If your houseboat sinks in 20 feet of water, raising it costs more than the boat’s value. One couple learned this the hard way—their insurer covered repairs but left them paying $50k to lift their sunken home.

- Ice damage riders: Northern dwellers, listen up! Freezing temps can crack pipes and heave docks. Standard policies often skip ice-related damage unless you beg.

- Airbnb clauses: Renting your houseboat for weekends? Most personal policies void coverage if you’re hosting paying guests. A stealthy exclusion that’s sunk many unwary owners.

The Hidden Currents – What Secretly Sways Your Insurance Costs

Insurers don’t just see a houseboat—they see a math problem of risk factors. Here’s what tips the scales:

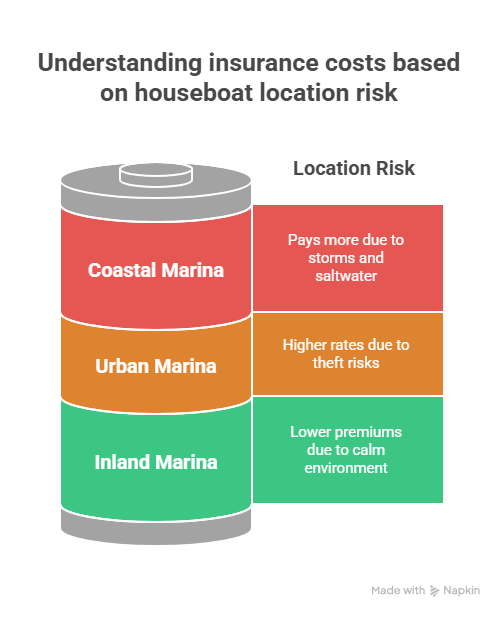

1. Location Roulette

Docked in a sleepy Appalachian lake? Insurers smile. Moored in hurricane alley? They’ll wince.

- The ZIP code effect: Marinas near open ocean pay 30% more than inland counterparts. Saltwater’s corrosive, storms are fiercer, and “named windstorm” deductibles can hit 5% of your home’s value.

- Dock drama: Private slips with security cameras score discounts. Shared urban marinas? Expect rate hikes for theft risks.

- Storage secrets: Winterizing on land? Some policies suspend coverage during storage unless you add a “lay-up” endorsement.

2. The Age Tango

Older houseboats have charm…and higher premiums.

- Vintage vessel tax: A 1970s houseboat with original wiring? Insurers see fire hazards and rot risks. One owner restored a ‘76 model beautifully but paid double premiums until upgrading the electrical system.

- Survey saviors: Marine surveys ($500-$1,500) can lower rates by proving your classic is shipshape. No survey? Insurers assume the worst.

3. Your Resume as a Captain

Insurers stalk your boating past like jealous exes.

- The “no claims” jackpot: Five accident-free years? You’re golden. That fender-bender at the marina fuel dock? It lingers like anchovy breath.

- Certification perks: A U.S. Coast Guard license or NASBLA course completion can slice 10% off premiums. It’s like a report card for grown-ups.

- Liveaboard lifestyle: Full-timers pay more—you’re there 24/7, so leaks get noticed slower, and your blender’s always threatening the electrical system.

The Devil’s Bargain – Actual Cash Value vs. Agreed Value

This choice haunts every owner: Do you want pennies or peace of mind?

Actual Cash Value (ACV): The Slow Letdown

How it stings: Your 10-year-old houseboat burns down. The insurer deducts a decade of depreciation. That $80k original cost? They pay $45k.

- Who it’s for: Budget-conscious owners okay with swallowing losses. Fine for old boats you’d replace with something cheaper anyway.

- The trap: Rebuilding costs often exceed ACV payouts. Post-hurricane material shortages left one owner $30k short of repairing their ACV-covered houseboat.

Agreed Value (AAV): Sleep-At-Night Insurance

The promise: You and the insurer agree on the value upfront. Total loss? You get every dollar (minus deductible).

- Cost: Premiums run 20-40% higher than ACV. Worth it for newer or custom houseboats.

- Pro tip: Update valuations every 2-3 years. Market surges (like the 2020 houseboat boom) can leave you underinsured.

The Silent Policy Killers – Exclusions That Capsize Claims

Even platinum policies have trapdoors. Here’s what slips through the cracks:

1. The Slow Rot of Neglect

The rule: Insurance loves sudden disasters, not slow-motion decay. Let your hull’s antifouling paint peel for years? Rot damage claims get denied.

- Survival tactic: Document maintenance religiously. Photos of annual hull cleanings and engine servicing can defeat “wear and tear” denials.

2. The Fine Print Flood Fiasco

The shocker: Many policies exclude floods—even for houseboats. Yes, the thing floats, but rising river waters? That’s a separate rider.

- Geographic gamble: Mississippi River dwellers pay up to $2k extra annually for flood endorsements. Skip it, and Katrina-level damage comes from your pocket.

3. The “You’re On Your Own” Zone

Navigation limits: Sail beyond your policy’s map (often 50 coastal miles), and you’re uninsured. A family learned this after coastal hopping to Mexico—their claim for storm damage got voided.

- Solution: “Cruising extensions” exist but cost like a first-class ticket. Plan routes before buying coverage.

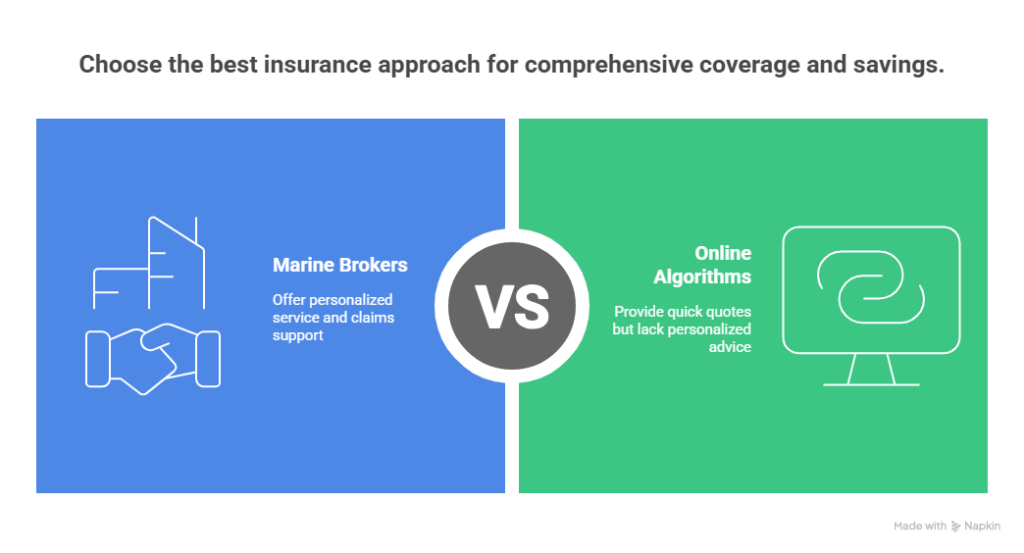

The Broker vs. Algorithm Smackdown – How to Shop Smart

Online quotes are easy. Good coverage? That’s a treasure hunt.

1. Why Marine Brokers Outwit Bots

They speak insurer: Brokers decode phrases like “included lay days” (free storage time during repairs) and “protection & indemnity” (liability nuances).

- Claims clout: After a wildfire near Shasta Lake, a broker-client’s claim sailed through while DIYers fought adjusters for months. Relationships matter.

2. The Comparison Cheat Sheet

Don’t just eye premiums. Compare:

- Hurricane deductibles (flat fee vs. percentage of value)

- Personal effects limits ($10k standard—too low if you’ve got designer furniture)

- Medical payment coverage (covers guests’ ER visits without lawsuits)

3. Discount Hacks They Hide

Security gear: Install a GPS tracker and fire suppression system? That’s 15% off.

- Pay annually: Monthly fees add 5-8% in service charges.

- Bundle creatively: Some insurers give “loyalty” discounts for bundling houseboats with motorcycles or RVs.

The Maintenance Gospel – Keep Coverage From Abandoning Ship

Insurers reward the meticulous. Here’s your piety checklist:

1. The Seasonal Rituals

- Winterizing: Not just draining pipes—document it. Time-stamped videos of antifreeze in the plumbing prevent “neglect” disputes.

- Engine hours log: Like a car’s odometer, it proves you’re not overworking the motor.

2. The Upgrade Balancing Act

- Report renos: That new solar panel array? It raises your home’s value—and requires adjusting coverage.

- Silent upgrades: Replacing old wiring? Tell your insurer—it might lower premiums.

3. The Paper Trail Doctrine

- Save every receipt: From life jacket purchases to dock fee payments. After a total loss, these prove you valued the houseboat properly.

- Photograph quirks: Custom built-ins or rare wood finishes? Without photos, insurers value them as IKEA-grade.

The Claim Survival Guide – Navigate the Aftermath

When disaster strikes, your response decides the payout.

1. The First 60 Minutes

- Safety first: But snap phone pics before rescuing your cat. Burnt curtains or waterlines prove damage extent.

- Mitigate smartly: Patch a broken window to prevent further damage—but don’t toss soggy furniture. Adjusters need to see it.

2. The Art of Negotiation

- Never accept the first offer: One owner got an extra $22k by proving their “used” appliances were commercial-grade.

- Hire a public adjuster: For large claims, their 10% fee often pays for itself. They speak the insurer’s dialect fluently.

3. The Rebuild Chess Game

- Contractor clauses: Some policies require insurer-approved repairers. Others let you choose. Know your rules.

- Code upgrades: Old houseboats rarely meet new codes. Ensure coverage includes “ordinance or law” riders for mandatory upgrades during repairs.

Conclusion: Houseboat Insurance

Houseboat living is a dance with nature—a waltz where waves lead and insurance is your safety net. The right policy isn’t about predicting every storm; it’s about knowing someone’s got your back when the weather turns. As you drift into sunset cruises and starlit decks, let your coverage be the quiet hum in the background, the unseen anchor keeping your dreams afloat. Because on the water, the only thing better than a beautiful view is the confidence to enjoy it.