This post may contain affiliate links, which means I may receive a commission for purchases made through the links. I will only recommend products that I have personally used! Learn more on my Disclosure page!

Florida boat insurance runs $652 to $839 annually, protecting you from the 836 boating accidents that bloodied Florida waters in 2020. Seventy-nine people died. Another 534 got hurt bad enough to file reports. That retired teacher from Kendall? His uninsured Sea Ray slammed into a channel marker near Stiltsville last April. The passenger’s spinal surgery cost $380,000. The lawsuit took his house, his savings, everything he’d worked 30 years to build. All because he thought saving $700 on insurance made sense.

Florida’s got over one million registered boats, more than any other state. Yet zero insurance requirements exist by law. Crazy? Absolutely. Smart captains know better. They’re paying those premiums, getting protected, sleeping soundly while others gamble their entire futures on calm seas and perfect luck.

How Much is Boat Insurance in Florida?

Here’s what you need to know about protecting your vessel, your assets, and your sanity in Florida waters. We’ll cover why Marathon boaters pay triple what Pensacola captains spend, which companies actually pay claims versus playing games, and the exact discounts that’ll slash your premium 30% by next Tuesday.

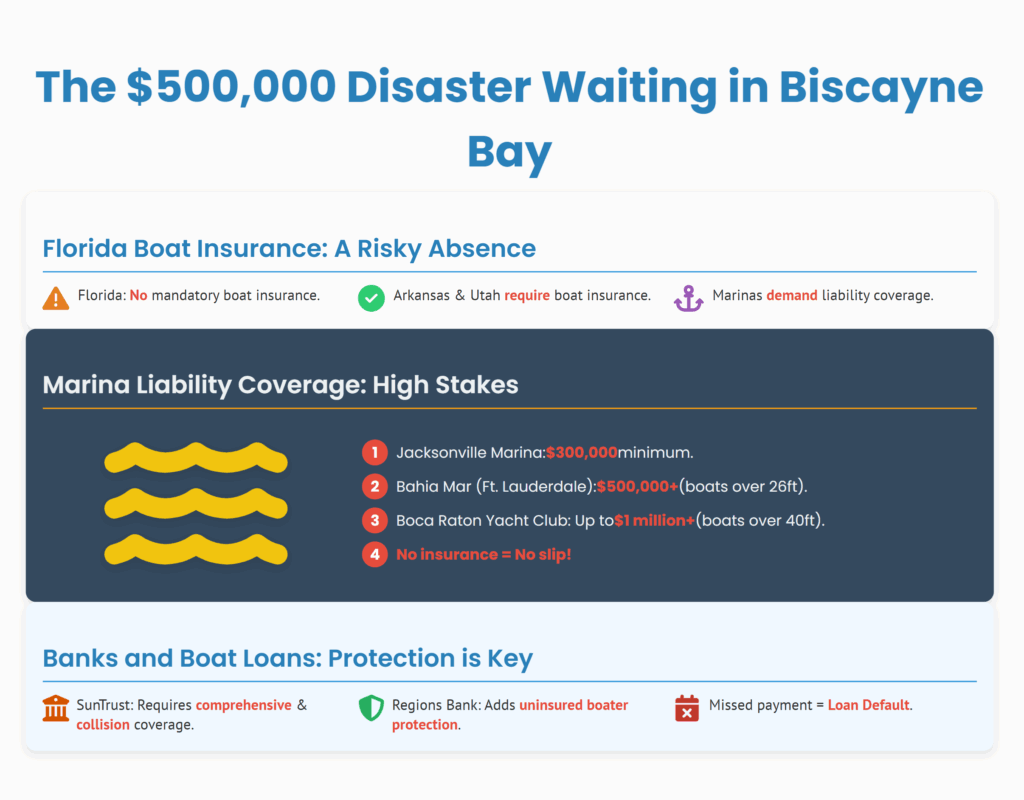

The $500,000 Disaster Waiting in Biscayne Bay

Florida doesn’t require boat insurance, not one penny of coverage mandated by Tallahassee. Arkansas requires it. Utah requires it. Florida? Nothing.

Yet every marina from Fernandina Beach to Key West demands liability coverage before they’ll rent you a slip. Jacksonville Marina wants $300,000 minimum. Bahia Mar in Fort Lauderdale? They’re asking for $500,000 if your boat’s over 26 feet. The Boca Raton Yacht Club pushes that to $1 million for anything over 40 feet. No insurance means no slip. Period.

Banks Don’t Play Games With Your Loan

Finance that Grady-White through SunTrust Marine? They’re demanding comprehensive and collision coverage matching your loan amount plus $500,000 liability. Regions Bank adds uninsured boater protection on top. Miss one insurance payment, just one, and you’re in default.

They’ll repo that boat faster than you can say “manatee zone.”

| Financing Source | Liability Required | Hull Coverage | What Happens If You Skip |

|---|---|---|---|

| Credit Union | $300,000 | Full loan amount | Immediate default notice |

| Marine Lender | $500,000 | Agreed value | Repo within 30 days |

| Big Bank | $1,000,000 | Replacement cost | Lawyers calling daily |

| Dealer Finance | $300,000 | Actual cash value | GPS kill switch activated |

Your cousin bought a $75,000 Robalo last summer. Thought he’d save money skipping insurance after making the down payment. The dealer’s finance company found out three weeks later. They demanded immediate payment in full, all $60,000 remaining. He couldn’t pay. They took the boat, kept his $15,000 down payment, and sued him for the $8,000 difference after the auction.

Expensive lesson.

Real Numbers: What Florida Captains Actually Pay

Florida boat insurance averages $652 yearly, nearly double what boaters pay in Georgia ($344) or Alabama ($263). But that average hides massive swings based on where you dock.

Key West? Forget about it. You’re paying $1,800 for that 22-foot Mako. Same boat costs $600 to insure in Pensacola. The difference? Hurricanes love the Keys. They’ve been hammered 41 times since 1900. The Panhandle? Way less attractive to storms somehow.

Miami-Dade County boaters get absolutely destroyed on premiums. Too many boats, too many accidents, too many lawyers on billboards. A buddy in Coconut Grove pays $2,400 yearly for his 28-foot Contender. His brother in Gainesville? Same exact boat, same coverage—$750.

The Real Cost Breakdown Nobody Shows You

| Boat Type | Destin | Tampa | Naples | Miami | Key Largo |

|---|---|---|---|---|---|

| Jet Ski | $300 | $400 | $450 | $600 | $750 |

| Bay Boat (21ft) | $450 | $600 | $750 | $1,000 | $1,300 |

| Pontoon (24ft) | $400 | $525 | $625 | $825 | $1,000 |

| Center Console (28ft) | $750 | $1,100 | $1,400 | $1,900 | $2,400 |

| Sportfish (35ft) | $1,200 | $1,700 | $2,200 | $3,000 | $3,800 |

| Yacht (45ft) | $2,500 | $3,500 | $4,500 | $6,000 | $7,500 |

Horsepower jacks up prices fast. That single 150HP Yamaha? Add $400 yearly. Twin 300s on your Freeman? That’s $1,200 extra. Go crazy with triple 400HP Mercurys? You’re looking at $2,000 more just for the engines.

Experience matters huge. Five years without claims? Premiums drop 25%. Take a boating safety course? Another 15% off. Store your boat in Ocala during hurricane season instead of staying in Marathon? Save 30% instantly.

Coverage That Actually Matters (And Stuff That Doesn’t)

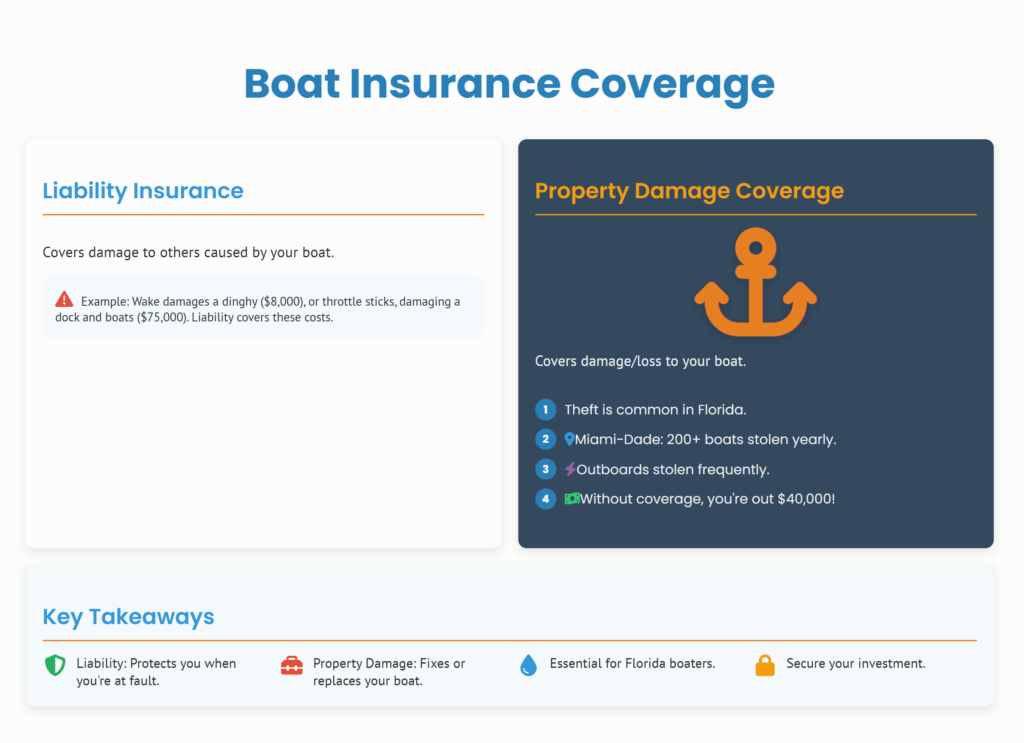

Liability insurance pays when bad things happen to other people because of your boat. Fundamental protection.

You’re cruising past Sunset Key. Your wake swamps a dingy. Their outboard dies, electronics fried. That’s $8,000 you owe them. Or you’re backing into a slip at Sailfish Marina in Stuart. Throttle sticks. You demolish the dock and scratch three boats. There’s $75,000 in damage. Liability coverage handles it all.

Property damage coverage fixes or replaces your boat after trouble finds you. Thieves love Florida boats. Miami-Dade alone sees 200+ boats stolen yearly. They’re grabbing outboards off boats at Matheson Hammock like it’s a shopping spree. One night, five engines gone. Without coverage? You’re out $40,000.

Medical Payments: The Friendship Saver

Your best friend slips stepping onto your boat at Dinner Key Marina. Compound fracture. $35,000 in surgery and rehab. Without medical payments coverage, guess what? He’s suing you. With it? Insurance pays, friendship survives.

Uninsured boater coverage—essential in Florida. Most boaters here carry nothing. Zero. Nada. They T-bone you in the Intracoastal near Jupiter. They’ve got no insurance, no assets, no way to pay for your $20,000 in fiberglass repairs. This coverage saves you.

Hurricane Coverage Florida Boaters Can’t Skip

Hurricane haul-out coverage reimburses $1,000 for moving your boat when storms threaten. Seems small until you’re scrambling to get your boat out of the water with everyone else. Yards jack prices to $2,000 when a Cat 4 aims at Fort Myers. This coverage helps.

Fishing equipment coverage replaces gear up to $10,000 total. That $800 Penn International reel disappears at Flamingo? Covered. Your entire tackle box, worth $2,000, walks off at the Skyway? Replaced. Limit’s $1,000 per item, though.

Fuel spill liability: Progressive includes it automatically. Others charge extra. Your tank ruptures after hitting a log near Chokoloskee. The cleanup runs $15,000 minimum. EPA fines add another $25,000. Without coverage? You’re bankrupt.

Insurance Companies Ranked by Reality, Not Marketing

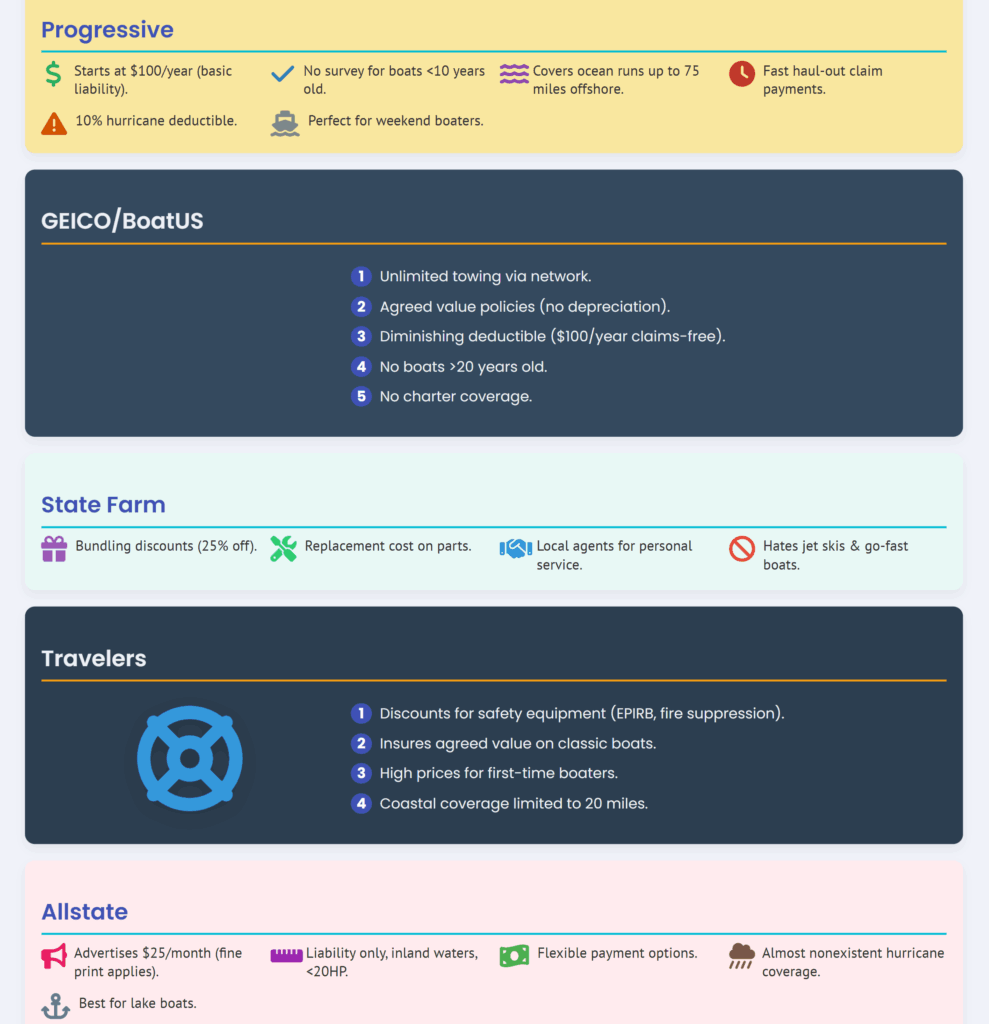

Progressive starts at $100 yearly for basic liability. No joke. No marine survey needed for boats under 10 years old. They cover ocean runs up to 75 miles offshore. When Dorian threatened, they paid haul-out claims within two weeks. Downside? Hurricane deductibles hit 10%. They’re perfect for weekend warriors with newer boats.

GEICO/BoatUS brings unlimited towing through their network. Broke down near Marquesas Keys? They’ll drag you back to Stock Island. Their agreed value policies mean no depreciation arguments after total losses. The diminishing deductible drops $100 yearly without claims. Sweet deal. But they won’t touch boats over 20 years old. And forget charter coverage.

State Farm bundles better than anyone—25% off when you combine home, auto, and boat. They pay replacement cost on parts, not depreciated value. Your three-year-old GPS worth $500 new but $200 used? They pay $500. Local agents mean face-to-face conversations, not call centers in India. Problem is they hate jet skis and go-fast boats.

Travelers loves safety equipment. Every piece of safety gear lowers your rate. EPIRB? Discount. Automatic fire suppression? Discount. They’ll insure agreed value on classic boats others won’t touch. First-time boaters get destroyed on pricing, though. And their coastal coverage stops at 20 miles offshore.

Allstate advertises $25 monthly, which sounds great until you read the fine print. That’s liability only, inland waters, under 20HP. Still, they’re flexible with payments. Hurricane coverage? Basically nonexistent. They’re scared of saltwater. Best for lake boats around Okeechobee.

Why Florida Eats Boats for Breakfast

Florida caught 41% of every hurricane that hit America since 1851. Not a typo. Almost half.

Your premium reflects this insanity.

Hurricane deductibles aren’t like regular deductibles. Storm approaches, your deductible jumps from $500 to 10% of hull value. Your $80,000 Yellowfin? That’s an $8,000 deductible if Bubba the Hurricane says hello. Regular thunderstorm damage? Back to $500. Makes no sense but that’s the game.

The Theft Capital of Boating

Thieves work Miami marinas like professionals. Two guys, one cordless grinder, three minutes—your twin Yamaha 300s vanish. They’re on a truck heading to a container ship before you finish dinner at Monty’s.

GPS trackers cut premiums 10%. More importantly, recovery rates hit 85% with tracking versus 15% without. Spend $500 on a SPOT Trace. Save $100 yearly on insurance. Do the math.

The Keys present special problems. Shallow water everywhere. Coral heads hiding just below the surface near Pennekamp. Shifting sand at Cape Sable. Every year hundreds of boats get intimate with the bottom. Standard policies exclude grounding. You need specific coverage or you’re looking at $30,000 repair bills.

Manatees create expensive problems. Federal fines for strikes reach $50,000. Your insurance better include federal penalty coverage. Plus you’re replacing props, maybe lower units. A manatee strike near Blue Spring cost one captain $65,000 total between fines and repairs.

Discounts That Actually Work

Bundle everything. Home, auto, boat—combine them all. State Farm gives 25% off. Progressive hits 20%. Even just pairing boat and auto saves 15%. On an $800 premium, that’s $200 back in your pocket.

Safety courses pay forever. Eight hours at a Coast Guard Auxiliary class saves 15% on premiums for life. BoatUS offers online courses for $39. Complete it Sunday, submit the certificate Monday, save $120 yearly starting immediately.

Clean record? Cash in. Three years claim-free earns 10% off. Five years gets you 20%. Some companies drop deductibles $100 yearly without claims. After five years, your $1,000 deductible becomes $500.

Storage Location Games That Save Thousands

Store your boat in Brooksville from June through November. Premium drops 30% compared to keeping it in Islamorada. Indoor storage adds another 10% discount. Climate-controlled? Another 5%. That’s 45% savings for moving your boat three hours north during hurricane season.

| Storage Strategy | Location | Season | Annual Savings |

|---|---|---|---|

| Basic Wet Slip | South Florida | Year-round | $0 (baseline) |

| Dry Stack | South Florida | Year-round | $200-$300 |

| Indoor Storage | Central Florida | June-Nov | $400-$600 |

| Climate Controlled | North Florida | June-Nov | $600-$900 |

Join a marina with group insurance deals. Sailfish Marina in Stuart partners with Progressive for 10% member discounts. Bahia Mar works with BoatUS for similar savings. Ask your dockmaster—most big marinas have deals they don’t advertise.

Hurricane Season Reality Check

Write a hurricane plan. Document everything. Where you’ll haul out. How you’ll secure the boat. Who does the work. Submit this to your insurer by May 1st. Get 5-10% off just for having a plan on paper.

Pre-arrange haul-out space now, not when a storm’s coming. Yards charge $500 reservation fee, applied to actual haul-out costs. Without reservations? You’re paying $2,000 cash when everyone panics. Or worse—no space available anywhere.

Insurance companies stop writing new policies 48 hours before storms threaten. Already insured? You must execute your hurricane plan or lose coverage. “I couldn’t get it out in time” doesn’t fly. They’ll deny everything.

After the Accident: What Really Happens

Take photos before anything moves. Video’s better. Get registration numbers, insurance info, witness contacts. Call the Coast Guard if anyone’s bleeding. File a report for damages over $2,000.

Call your insurer within 24 hours max. Weekend accident? Monday morning at latest. Document who you spoke with, when, claim number. Email a summary immediately after calling. Creates a paper trail that protects you later.

Marine surveyors show up within 72 hours usually. Don’t admit fault to anyone. Let insurance companies fight it out. Use their approved repair yards—work’s guaranteed and they handle the paperwork.

Claims typically close in 15-30 days. Collision accounts for 35% of claims. Storm damage 25%. Theft 20%. Average payout? $8,500.

Smart Buying Moves

Get five quotes minimum. Rates vary 40% for identical coverage. Use an independent agent who shops multiple companies. Online quotes miss discounts constantly.

Read exclusions like your life depends on it. “Named storm” differs from “hurricane” coverage. Racing exclusions matter if you fish tournaments. Charter coverage needs specific endorsements. Miss these details? Claim denied, you’re screwed.

Check navigation limits carefully. Standard policies cover different distances offshore. Planning Bahamas runs? Need international coverage. Fishing the Gulf Stream? Needs oceanic endorsement. Exceed your navigation limits? Coverage vaporized.

Pick agreed value over actual cash value for anything under 10 years old. Costs 20% more but pays off huge during total losses. Your five-year-old $100,000 Pursuit becomes worth $60,000 under actual cash value. Agreed value? Full $100,000. No arguments.

Your Next Move

Florida boat insurance protects smart captains from financial ruin. That $652 to $839 yearly premium prevents bankruptcy when accidents happen. And they happen constantly—836 times in 2020 alone.

Get quotes from Progressive, GEICO/BoatUS, and State Farm today. Bundle your policies—save 25% immediately. Take a safety course this weekend—another 15% off. Move your boat north for hurricane season if you’re in South Florida. These three moves drop an $850 premium to under $500.

Don’t become another cautionary tale at the marina bar. Don’t lose your house over a moment’s inattention near Government Cut. Get covered. Stay covered. Boat without fear.

Frequently Asked Questions

Do I need insurance to register my boat in Florida?

Nope. Florida registration needs zero insurance, just ownership proof and fees. But try getting a decent slip without liability coverage. Try financing without full coverage. Registration’s easy—everything else requires insurance.

Does my homeowners policy cover my boat?

Maybe $1,000 for your kayak. Your real boat? Forget it. Homeowners might cover a tiny jon boat with a trolling motor. Your 21-foot Pathfinder? Not a chance. You need real marine insurance or you’re completely exposed.

What happens if I hit someone without insurance?

You lose everything. Medical bills hit $500,000 fast. Property damage adds another $100,000. They’ll sue, win, take your house, garnish wages, drain retirement accounts. Bankruptcy might not even save you from personal injury judgments. One accident without insurance equals financial death.

Can I get insurance during hurricane season?

If you already have it, yes. New policy? Companies stop writing 48 hours before storms threaten. June through November gets tricky. Better to buy in February when nobody’s thinking about hurricanes. Plus rates are lower in spring.

Will anyone insure my 25-year-old boat?

Most insurers run away from boats over 20 years. Some specialists handle classics. You’ll need a marine survey ($500-$800). Agreed value gets tough. Actual cash value might be your only choice. Premiums run higher too. But coverage exists if you search hard enough.