This post may contain affiliate links, which means I may receive a commission for purchases made through the links. I will only recommend products that I have personally used! Learn more on my Disclosure page!

Does boat insurance cover the motor? Yes, standard boat insurance does cover your motor, but with critical caveats. Motors are typically protected under hull coverage for attached engines (inboard/sterndrive) or via separate policies for portable outboards. Coverage applies to sudden, accidental damage like collisions, theft, or storms, not wear-and-tear or neglect.

Understanding Boat Insurance Motor Coverage Basics

What Does Boat Insurance Actually Cover for Your Motor?

You’re idling through reeds when a hidden log shatters your propeller shaft, or winter freeze cracks your block. Does boat insurance cover the motor in these nightmares? Typically yes, but how it’s covered depends on your policy’s DNA. Motors usually fall under “hull coverage,” bundled with the boat itself. But exceptions lurk everywhere. Let’s decode protection levels before you file that claim.

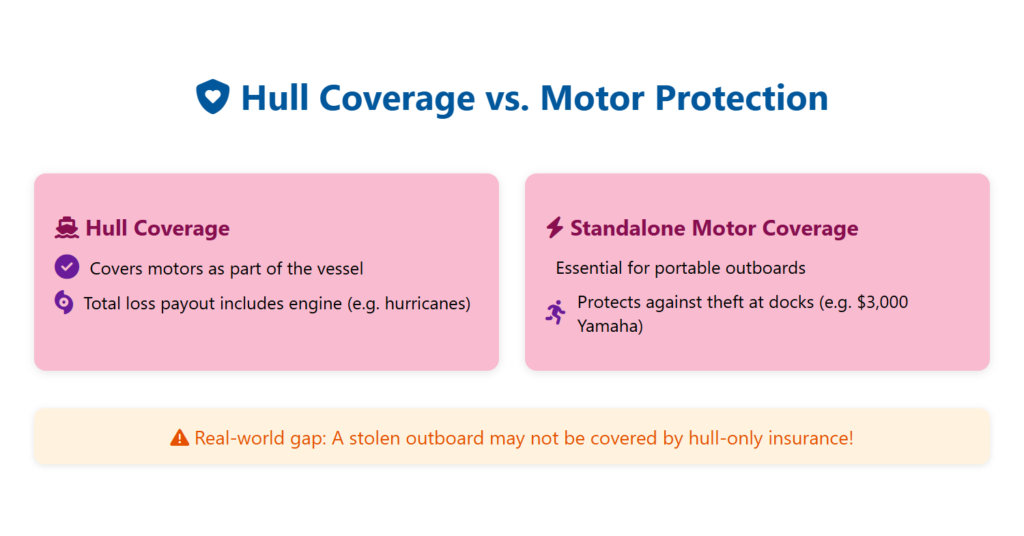

Hull Coverage vs. Separate Motor Protection

- Hull Policies: Cover motors as part of the vessel (e.g., a totaled boat in a hurricane includes engine payout)

- Standalone Motor Coverage: Critical for portable outboards (e.g., theft of your $3,000 Yamaha from a dock)

Real-world gap: If only insured under hull coverage, a stolen detached outboard might not be covered.

Outboard vs. Inboard Motor Rules

| Motor Type | Coverage Scope | Common Exclusions |

|---|---|---|

| Outboard | Theft, collision, fire, storms | Corrosion, wear-and-tear |

| Inboard/ Stern Drive | Full replacement if sunk | Mechanical breakdown |

Saltwater vs. Freshwater Nuances:

- Saltwater corrosion damage? Rarely covered without additional endorsements

- Freshwater overheating from clogged intake? Often excluded as “lack of maintenance”

How Comprehensive & Liability Policies Differ

- Comprehensive: Covers non-collision disasters (theft, fire, sinking)

- Liability-Only: Zero motor protection—only pays for damage you cause to others

Example: An electrical fire destroys your inboard motor. Comprehensive pays. If you crash into a dock, liability covers the dock—not your shattered engine.

Types of Motor Coverage in Boat Insurance

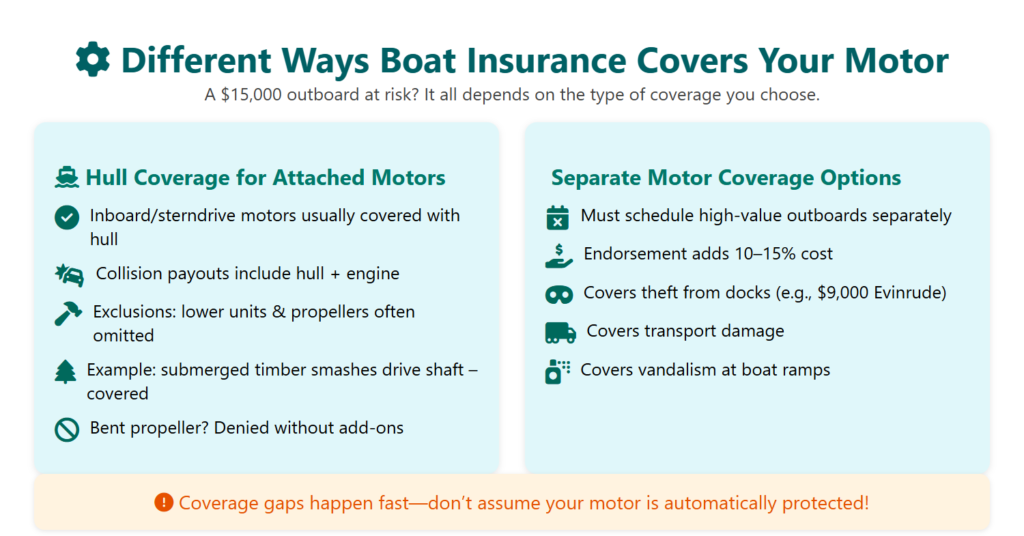

Different Ways Boat Insurance Covers Your Motor

Your motor’s protection lives or dies by policy type. A $15,000 outboard stolen off your dock faces different rules than a hurricane-flooded inboard. These coverage paths determine whether you’re fully protected or dangerously exposed.

Hull Coverage for Attached Motors

Inboard and sterndrive motors typically ride under hull protection. Total your boat in a collision? Insurance replaces both hull and motor. But loopholes exist: some policies exclude lower units or propellers. Imagine hitting submerged timber on the Hudson; hull coverage handles the shattered drive shaft but might deny a bent propeller without specific add-ons.

Separate Motor Coverage Options

Portable outboards demand their own policies. Forget to schedule that new $9,000 Evinrude? Theft claims vanish. Adding this endorsement costs 10-15% more but covers nightmare scenarios:

- Midnight theft from your Avalon dock

- Impact damage during highway transport

- Vandalized fuel lines at a Jersey Shore ramp

Agreed Value vs. Actual Cash Value

| Valuation Method | Payout Reality | Best Fit |

|---|---|---|

| Agreed Value | Full pre-set amount | New motors, rare models |

| Actual Cash Value | Current value minus wear | Older, low-cost motors |

That 2020 Mercury worth $8,000 new? ACV pays $4,500 after three seasons of saltwater use.

Motor Coverage Breakdown

| Coverage Type | Protection Scope | Cost | Ideal For |

|---|---|---|---|

| Hull Coverage | Attached motors | Base premium | Inboard cruisers |

| Separate Policy | Specific outboard coverage | +10-15% | Bass boats |

| Comprehensive | Theft, storms, vandalism | Varies by deductible | All vessels |

| Liability Only | Zero motor protection | Lowest | Derelict hulls |

What Motor Damages Are Typically Covered

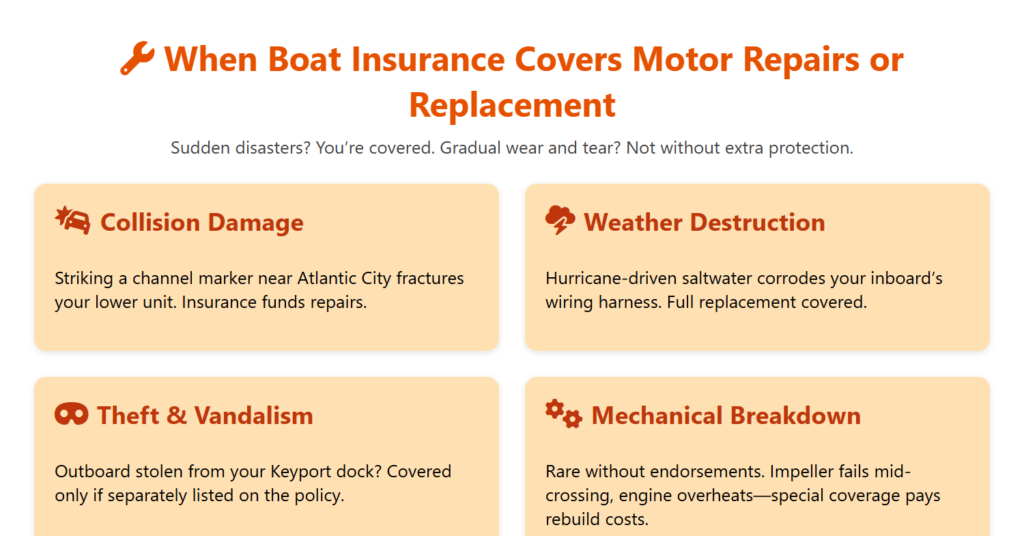

When Boat Insurance Covers Motor Repairs or Replacement

Does boat insurance cover the motor when a nor’easter floods your engine block? Yes—if you carry comprehensive coverage. Protection activates for sudden disasters, not slow breakdowns. Real claims we’ve seen paid:

Collision Damage

Striking a channel marker near Atlantic City fractures your lower unit. Insurance funds repairs.

Weather Destruction

Hurricane-driven saltwater corrodes your inboard’s wiring harness. Full replacement covered.

Theft & Vandalism

Outboard stolen from your Keyport dock? Covered only if separately listed on the policy.

Mechanical Breakdown

Rare without endorsements. Example: Your impeller fails mid-crossing, overheating the engine. Special coverage pays for rebuilds.

Snap timestamped photos post-incident. Adjusters demand proof damage wasn’t pre-existing.

Common Motor Coverage Exclusions

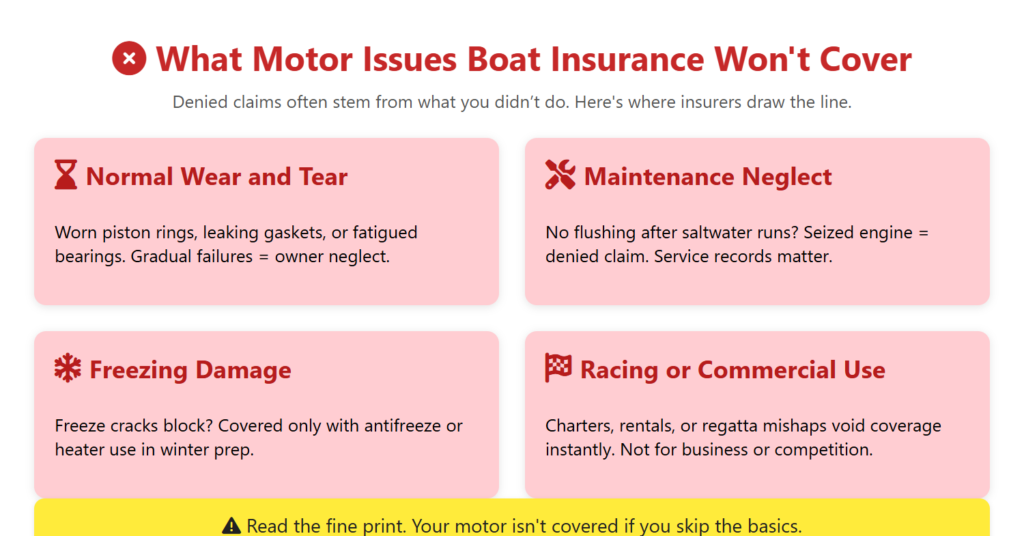

What Motor Issues Boat Insurance Won’t Cover

These claim-killers cost boaters thousands yearly. That corroded crankshaft from skipped maintenance? Denied. Frozen block after botched winterization? Your problem. The fine print bites hardest here:

Normal Wear and Tear

Worn piston rings, leaking gaskets, or fatigued bearings. Gradual failures signal “owner neglect” to insurers.

Maintenance Neglect

Never flushed saltwater from cooling passages? Seized engines get $0. Service records are your armor.

Freezing Damage

A single freeze cracks your block. Covered only if you used antifreeze or block heaters.

Racing/Commercial Use

Rented your boat for charters? Crashed in a regatta? Policy voided instantly.

Saltwater corrosion eats aluminum hulls near Cape May.

Racing voids coverage faster than a blown piston.

Document everything or pay everything.

Factors Affecting Motor Coverage Costs

How Motor Value Impacts Your Boat Insurance Premiums

Your premium isn’t random, it’s calculated from risks insurers see in your motor. A 300HP Mercury Verado screams “expensive claim,” while a 25HP trolling motor barely registers. These boat motor insurance cost factors directly sway your bill:

- Age & Value: A new $20,000 outboard adds $400+/year vs. $75 for a 1990s model

- Horsepower: Motors >250HP incur 20-30% surcharges (high-speed accident risk)

- Security Features: GPS trackers (e.g., Garmin EchoMap) slash premiums by 15%

- Usage: Saltwater fishing 50+ days/year? Expect 40% higher costs than occasional lake use

Storage matters brutally:

- High-risk: Dockside in Atlantic City (theft/storms)

- Low-risk: Garage-stored in Princeton with wheel locks

Choosing the Right Motor Coverage

How to Ensure Your Boat Motor Is Properly Insured

Match coverage to your motor’s real-world threats. A weekend angler with a 40HP Suzuki needs different protection than a liveaboard cruiser. Ask these questions:

Motor Replacement Cost

Can you afford a $15,000 repower? If not, choose agreed value coverage (avg. $500/year premium).

Deductible Tradeoffs

- $250 deductible: Adds $150+/year

- $1,000 deductible: Cuts premiums 25%

Usage Frequency

- Light use (20 days/year): Liability + physical damage ($250-$600/year)

- Heavy use: Comprehensive + mechanical breakdown endorsement ($800-$1,500)

Storage Location Tiers

| Risk Level | Storage Example | Premium Impact |

|---|---|---|

| Platinum | Climate-controlled garage | -25% |

| Gold | Gated marina (Sandy Hook) | Baseline |

| Bronze | Open dock (Jersey City) | +40% |

Expert range: NJ premiums span $150–$2,500/year. $500k liability + $10,000 motor coverage averages $725.

Filing Motor Insurance Claims

Steps to Take When Your Boat Motor Needs Insurance Coverage

Your engine just seized mid-channel. Don’t panic—document. Miss one step, and insurers deny claims for “insufficient evidence.” Here’s your battle plan:

- Immediate Documentation

Snap timestamped photos: whole motor, damage close-ups, accident context (e.g., submerged log). Video the failure if safe. - Contact Your Insurer

Call within 24 hours. Delays = suspicion. Have policy #, photos, and mechanic contacts ready. - Marine Surveyor Collaboration

Let their expert assess the damage. Don’t authorize repairs first—voids coverage. - Repair vs. Replacement Call

Under 60% repair cost? Insurers fix. Over? They’ll total it. Negotiate if quoted repair costs exceed the motor value.

“But the adjuster lowballed me!” Demand second opinions from certified marine mechanics.

Conclusion: Does Boat Insurance Cover the Motor

Does boat insurance cover the motor? Absolutely—for sudden disasters like theft, storms, or collisions. But protection isn’t automatic. Hull coverage safeguards inboards; outboards need scheduled policies. Remember: wear-and-tear, freeze damage, and neglect are always excluded.

Key Takeaways:

- Verify agreed value coverage for new motors

- Saltwater use demands corrosion endorsements

- Storage location slashes or spikes premiums

- Document everything before filing claims

Don’t gamble with your engine—the heart of your boat. Review your policy’s motor section today. Missing coverage? Get a quote from a NJ marine specialist. Peace of mind on Barnegat Bay is three pages away.

Final Thought: Insurance replaces motors. It can’t replace memories made aboard. Cover both wisely.