This post may contain affiliate links, which means I may receive a commission for purchases made through the links. I will only recommend products that I have personally used! Learn more on my Disclosure page!

Ever stood on a dock, watching boats glide by, and wondered what happens if one of those babies crashes into something? Or maybe you’ve finally saved up for that pontoon you’ve been eyeing, but now you’re drowning in paperwork and wondering—Do You Have to Have Insurance on a Boat?

Let’s cut through the confusion. The short answer? It depends. Unlike car insurance, which pretty much every state demands you have, boat insurance requirements are a bit… well, all over the place. It’s not a simple yes or no situation, which is probably why you’re here reading this in the first place.

The Legal Side: When You Gotta Have It

First things first—some situations where you absolutely, positively need boat insurance, no two ways about it:

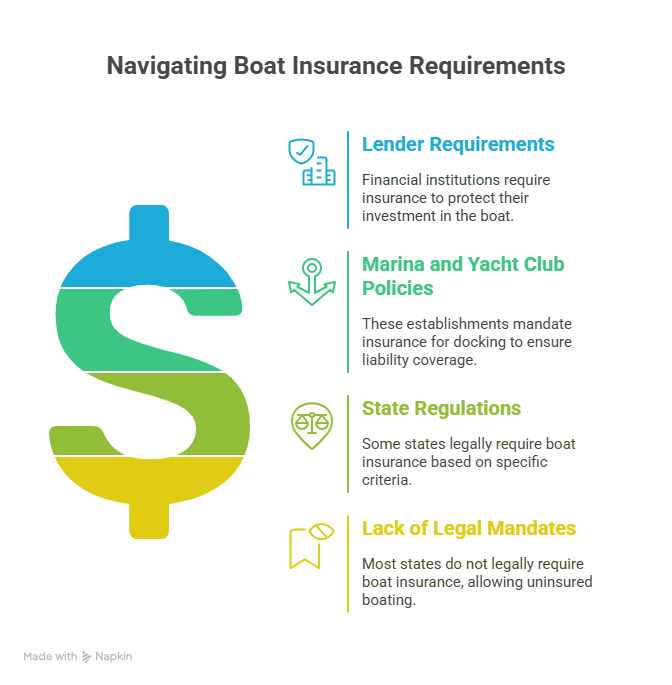

If you’ve got a loan on that beauty, your lender’s gonna insist on coverage. Makes sense, right? They’ve got money tied up in your vessel and wanna protect their investment. Same deal if you’re leasing. The company that actually owns the boat isn’t about to let you take their property out uninsured.

Then there’s marinas and yacht clubs. Try docking at most of these places without insurance—they’ll laugh you right back onto the water. Most require at least $300,000 in liability coverage before they’ll even consider letting you tie up. It’s their property, their rules.

Now for the government angle. A handful of states actually do mandate boat insurance—Arkansas, Hawaii, and Utah come to mind. Each has different requirements though. Arkansas wants liability coverage on boats with engines over 50 horsepower, while Utah focuses on boats worth over $2,000. Hawaii’s rules apply to specific harbors.

But here’s where it gets interesting—most states don’t legally require anything. Zip. Zero. Nada. You could technically take your uninsured bass boat out on a Michigan lake tomorrow, and no one’s gonna write you a ticket specifically for being uninsured.

Does that mean you should skip coverage? Well, that’s where things get complicated.

The Reality Check: When You Should Have It Anyway

So here’s the deal—just ’cause something ain’t legally required doesn’t make it smart to skip. Kinda like… ya know how nobody’s forcing you to wear a helmet on your bike in most states? But your skull’s probably thanking you when you wipe out and don’t end up eating through a straw for six months. Same kinda thing.

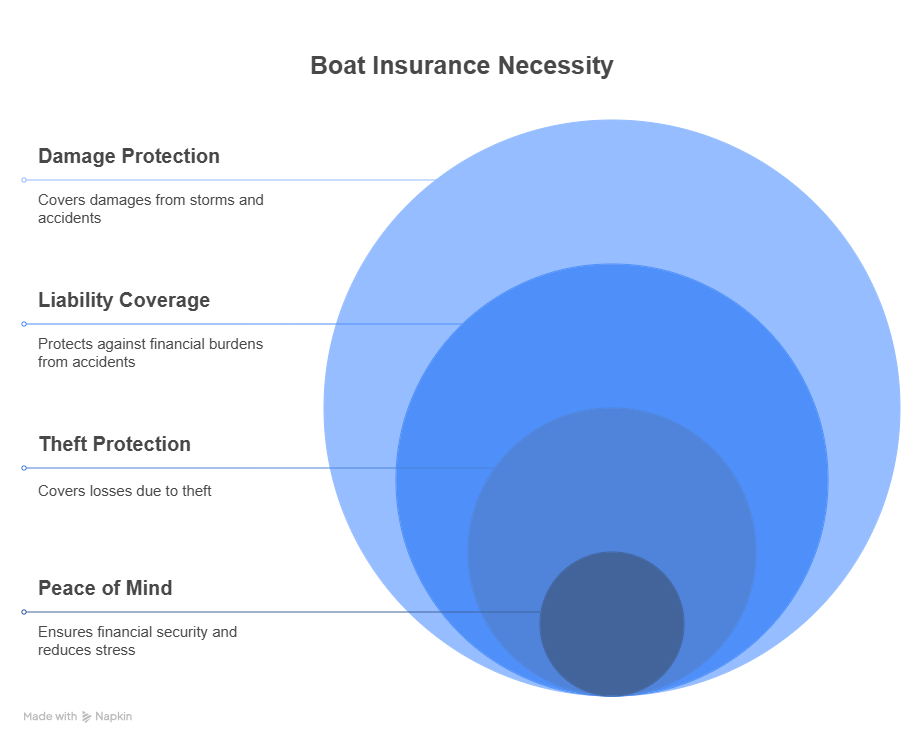

Consider this: boats aren’t cheap. Even a modest fishing boat can set you back $20,000 or more. That’s a significant chunk of change to leave unprotected. And water… well, water’s not exactly forgiving. Storms kick up, submerged objects lurk beneath the surface, and let’s be honest—some folks on the water have absolutely no clue what they’re doing.

Then there’s liability. Imagine this scenario: You’re having a great day on the lake, music playing, sun shining. You get distracted for just a second, and boom—you’ve crashed into another boat. Now you’re looking at their repair bills, possible medical expenses, and maybe even legal fees if they decide to sue. Without liability coverage, that’s all coming straight from your pocket.

And we haven’t even talked about theft yet. Boats are pretty easy targets—they’re often stored in accessible places, they’re valuable, and they’re literally designed to be moved. Insurance helps you sleep at night knowing you’re not completely out of luck if someone decides your boat looks better in their possession than yours.

What Boat Insurance Actually Covers

So what’s boat insurance really do for ya? It ain’t just some one-size-fits-all thing—more like a whole grab bag of different protections all bundled together:

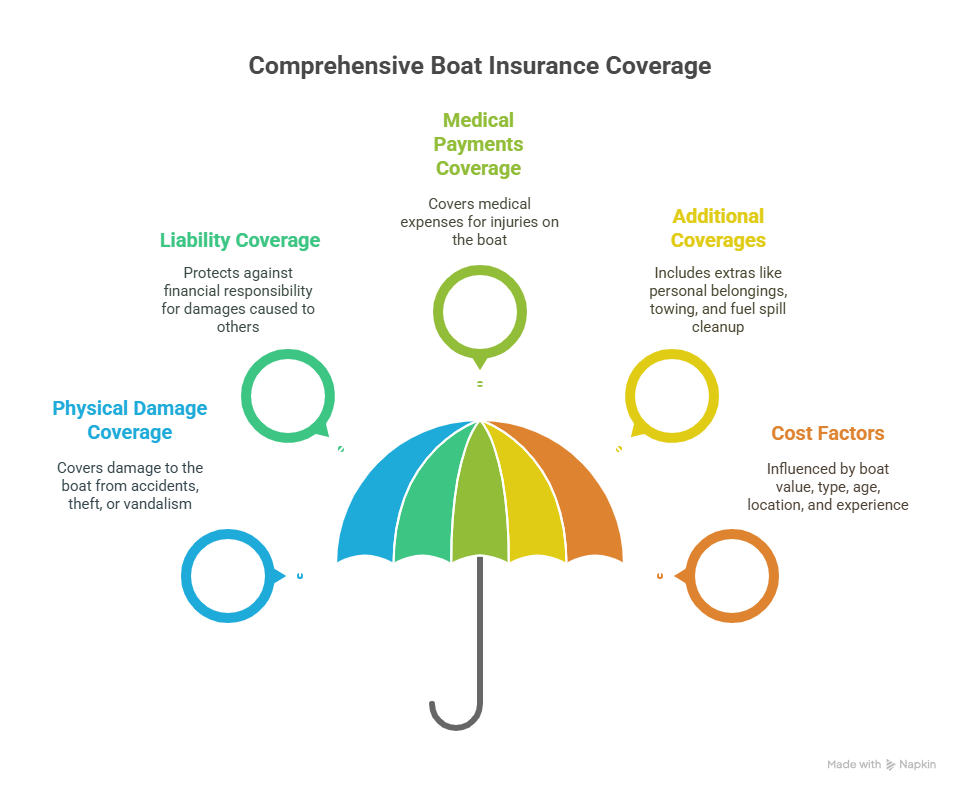

When your boat gets smashed up or totaled? That’s where physical damage coverage kicks in. It covers everything from hitting a dock to fires, nasty storms, theft, and even drunk teenagers deciding to tag your hull with spray paint. Basically anything bad that happens to the actual boat itself, this is the part that’s got your back.

Liability coverage? That’s the part that deals with damage you cause to other folks or their stuff. Say you’re at fault in some accident—this keeps you from having to hawk a kidney on the black market just to cover all the bills.

Then there’s medical payments coverage. Handles injuries to you or whoever’s riding with ya, don’t matter who caused the mess. And lemme tell ya, those hospital bills? They stack up faster than empties at a fishing tournament, especially when they gotta send helicopters or you end up in the ER.

Some policies even toss in little extras—like coverage for personal belongings on your boat, towing if you break down on the water, or fuel spill cleanup (which, trust me, can cost ya thousands if you dump diesel in a protected marina).

So what’s all this protection gonna cost ya? Well, it’s all over the map depending on your boat’s value, what type it is, how old, where you’re using it, and how much experience you’ve got under your belt. But ballpark? Figure somewhere between 1-5% of what your boat’s worth each year. So if you’ve got a $20,000 boat, you’re probably looking at $200-$1,000 annually. Not exactly chump change, but won’t exactly break the bank either.

The Hidden Costs of Going Uninsured

Here’s something most folks don’t think about—the hidden costs when you skip insurance. Like, say your uninsured boat causes environmental damage. We’re talking fuel leaks, oil spills, that kinda thing. The EPA don’t mess around with that stuff. Cleanup costs? Astronomical. We’re talking tens of thousands, sometimes hundreds of thousands of dollars.

Or how ’bout this scenario—your boat breaks loose during a storm and smashes into a neighbor’s dock. Without insurance, you’re on the hook for all of it. And don’t think your homeowner’s policy’s gonna swoop in and save the day. Most have specific exclusions for this exact situation.

I knew this guy once—let’s call him Mike. Had a sweet little 22-footer he’d take out on Lake Michigan. No insurance, ’cause why bother, right? One weekend, strong winds kicked up while it was docked. Boat broke loose, drifted into a marina, and damaged three other vessels before they could secure it. Final bill? Just shy of $95,000. Mike had to sell his house to cover it. No joke.

Real Talk: When You Might Skip It

I’m not here to sell you insurance. There are legitimate situations where you might reasonably go without:

If you’ve got a small, inexpensive boat—like a canoe, kayak, or small sailboat worth under a couple thousand bucks—the insurance might cost more than it’s worth. These craft also tend to cause less damage if something goes wrong.

Some homeowners or renters insurance policies actually cover small boats already. Worth checking your policy before you buy separate coverage. Just be aware that these typically have pretty low coverage limits and might only cover the boat while it’s at your home.

If you’re an experienced boater with a solid emergency fund who only takes out a small, paid-off boat on calm waters… maybe you’re comfortable with the risk. That’s your call. Just be honest with yourself about whether you could handle a worst-case scenario financially.

The Fine Print: What Insurance Typically Won’t Cover

Course, no insurance covers everything. Most policies have exclusions you should know about. Like normal wear and tear—that’s on you, buddy. Insurance companies figure regular maintenance is your responsibility. Same goes for gradual deterioration, marine life damage (barnacles and such), and manufacturer defects.

And if you’re thinking of using your boat for commercial purposes—like fishing charters or water taxi services—your regular pleasure craft policy ain’t gonna cut it. You’ll need specialized commercial coverage for that.

Oh, and read the fine print about navigational limits. Most policies specify exactly where you’re covered. Take your boat outside those boundaries? You might as well have no insurance at all.

How to Actually Decide What’s Right for You

Here’s a quick gut-check to figure out if you should get boat insurance:

Ask yourself: “If my boat sank tomorrow, would I be financially devastated?” If yes, get insurance.

Consider: “If I accidentally hit someone else’s expensive boat, could I afford to pay for it?” If no, definitely get liability coverage at minimum.

Think about where you boat. Busy waterways with lots of expensive vessels around? Insurance starts looking pretty smart.

And be realistic about your experience level. Newbies make mistakes—it’s just part of learning. Insurance gives you room to gain experience without one error costing you everything.

Shopping Smart: Getting the Best Coverage for Your Buck

If you do decide to get coverage, don’t just go with the first quote you get. Shop around. Different insurers weigh risk factors differently. Some give discounts for safety courses, others for clean driving records (yep, your car driving history can affect your boat insurance).

Bundle policies when you can. Most companies offer decent discounts if you insure your home, car, and boat with them. And don’t be shy about asking for discounts—many companies offer ’em for everything from automatic fire extinguishers to being claim-free for several years.

Higher deductibles mean lower premiums, but make sure you can actually afford that deductible if something happens. No point saving $50 a year if you can’t cover a $1,000 deductible when disaster strikes.

Conclusion: Do You Have to Have Insurance on a Boat?

So do you legally have to have insurance on a boat? In most places, no. But is it a good idea anyway? For most boat owners, absolutely.

Boating’s supposed to be about relaxation and fun, not financial stress. There’s something pretty nice about being out on the water knowing that if something goes sideways, you’re not facing financial ruin. That peace of mind alone might be worth the premium.

Whatever you decide, just make it an informed choice. Talk to other boaters, get quotes from different insurers, and read the fine print. Your perfect day on the water is waiting—just make sure you’ve thought through what happens if that perfect day takes an unexpected turn.

And hey—if you do decide to go without insurance, maybe stay a little further away from my boat out there. Just saying.