This post may contain affiliate links, which means I may receive a commission for purchases made through the links. I will only recommend products that I have personally used! Learn more on my Disclosure page!

Do boats have to have insurance? Only Arkansas and Utah legally require boat insurance for all motorized vessels, but operating without coverage exposes you to unlimited financial liability that bankrupts 1,400 boat owners annually, according to U.S. Coast Guard data. The remaining 48 states don’t mandate insurance, yet 73% of boaters carry policies because one accident without protection destroys decades of financial stability.

Sarah Mitchell learned this lesson on Lake Michigan last September. No insurance required in Illinois. Her 22-foot Chaparral struck a submerged log, sending five passengers to Northwestern Memorial Hospital. Medical bills: $847,000. Legal settlements: $1.3 million. Her retirement savings, home equity, and daughter’s college fund: Gone.

You’re discovering exactly which states require coverage, what happens during accidents without insurance, specific liability scenarios that destroy uninsured boaters financially, and affordable protection starting at $50 monthly that prevents bankruptcy from a split-second mistake.

State-by-State Boat Insurance Requirements

The legal landscape shocks most boaters. Arkansas and Utah stand alone requiring insurance, yet specific situations trigger mandatory coverage in 31 other states.

Your state probably doesn’t require boat insurance. Your mortgage lender does. Your marina does. Your sanity should. Here’s the complete breakdown of legal requirements versus practical reality.

States With Mandatory Requirements

Arkansas demands liability coverage for all motorized watercraft. Minimum limits: $50,000 per person, $100,000 per accident, $25,000 property damage. Penalties for non-compliance include $100-$500 fines, registration suspension, and criminal charges for repeat violations.

Utah enforces similar requirements. Every motorized vessel needs liability protection. Jet skis included. Sailboats with auxiliary motors included. Electric trolling motors? Still counts. The state runs insurance verification checks at launch ramps during holiday weekends.

| State | Coverage Required | Minimum Limits | Penalty for Non-Compliance | Enforcement Method |

|---|---|---|---|---|

| Arkansas | All motorized vessels | $50K/$100K/$25K | $100-$500 fine + registration suspension | Random checks + accident verification |

| Utah | All motorized vessels | $25K/$50K/$15K | $75-$300 fine | Launch ramp inspections |

| All Other States | None (with exceptions) | N/A | N/A | Post-accident liability |

Hidden Requirements Nobody Mentions

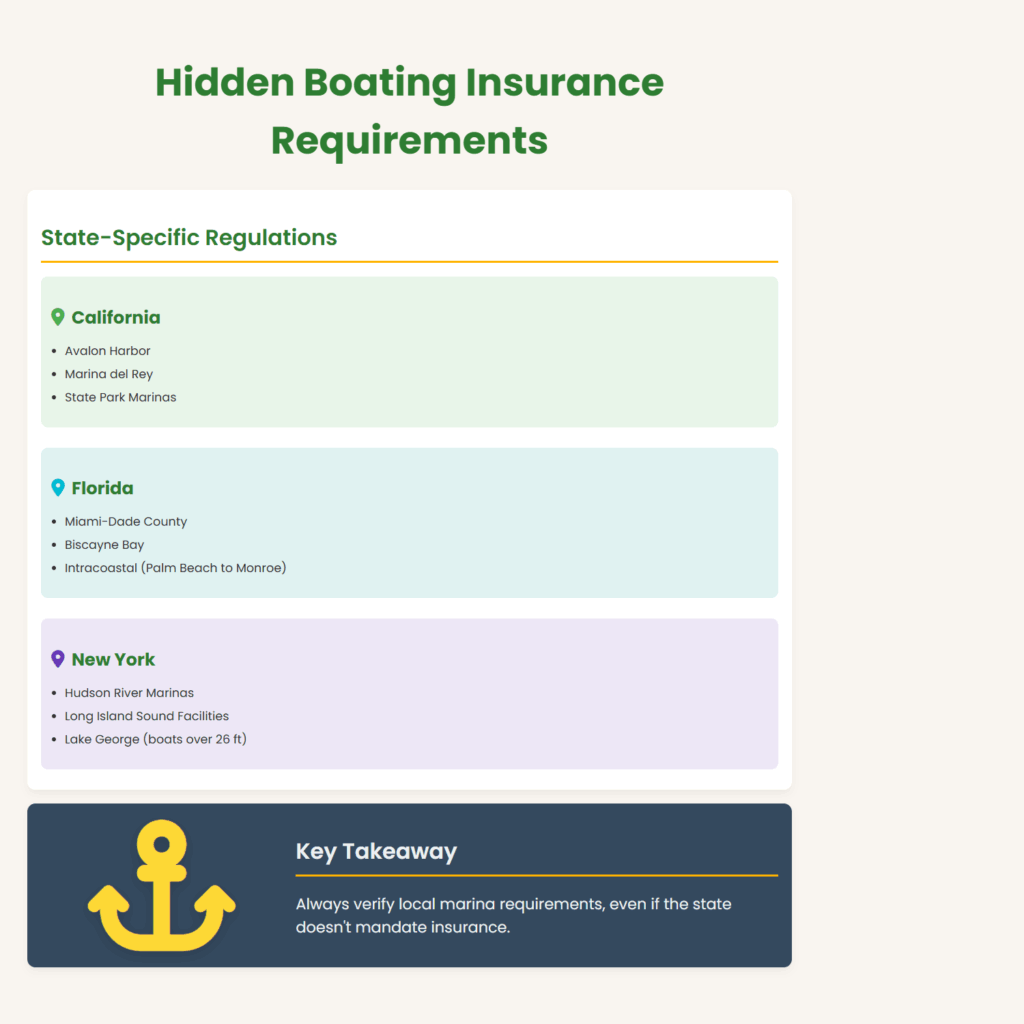

California doesn’t require insurance. Unless you boat in Avalon Harbor. Or berth at Marina del Rey. Or enter any state park marina. These facilities demand proof of coverage.

Florida has no state mandate. Miami-Dade County does. Specific waterways require insurance. Biscayne Bay? Coverage required. The Intracoastal from Palm Beach to Monroe County? Insurance mandatory at most marinas.

New York State says no insurance needed. New York City says otherwise. Hudson River marinas require $1 million liability minimum. Long Island Sound facilities demand coverage proof. Lake George mandates insurance for boats over 26 feet.

Federal Waters Change Everything

Three miles offshore, state laws stop mattering. Federal admiralty law applies. Insurance isn’t required, but liability becomes unlimited.

You damage a commercial vessel in federal waters without insurance? Personal bankruptcy provides no protection. Maritime liens attach to everything you own. Forever. Until paid.

That shrimp boat you accidentally hit outside Mobile Bay? They’re claiming $2.8 million in lost income. Your house, cars, retirement accounts, future wages – all subject to seizure.

What Happens Without Insurance: Real Accident Scenarios

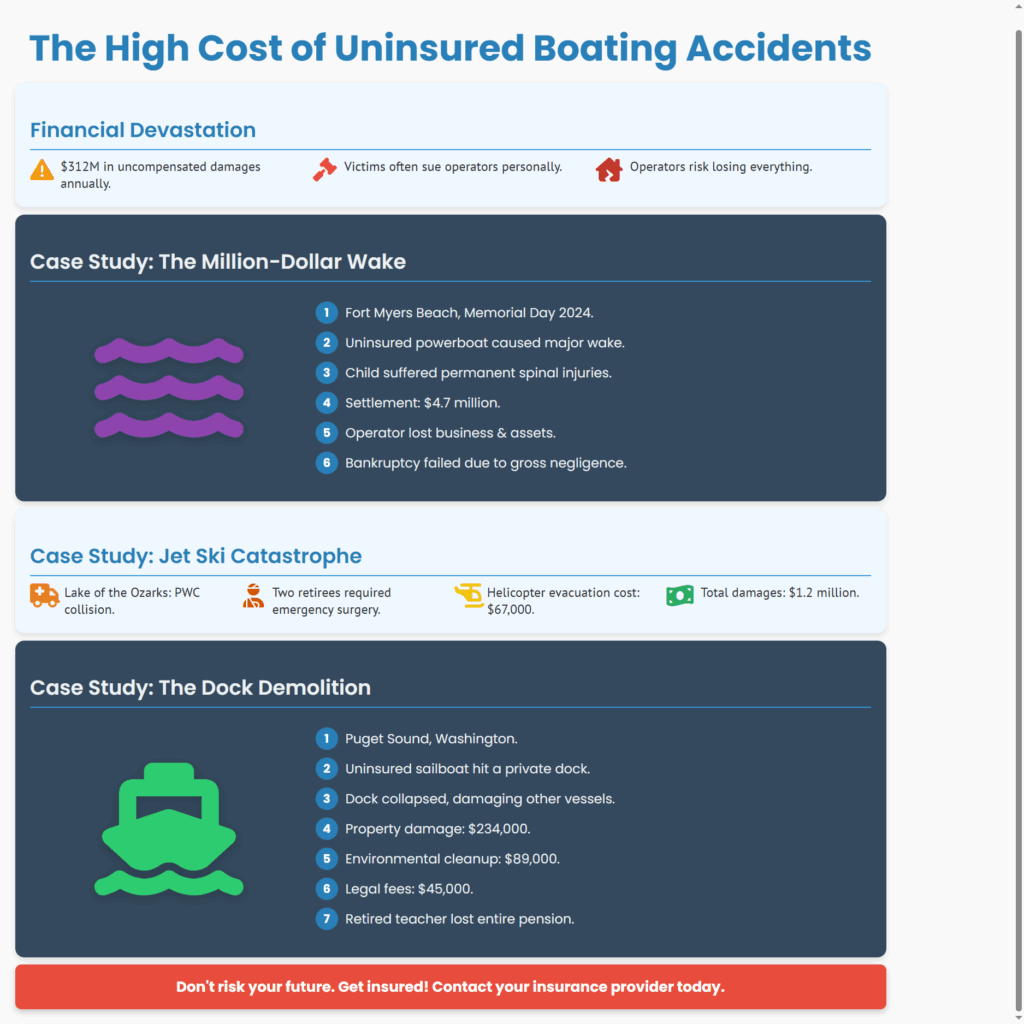

The statistics chill your blood. Uninsured boating accidents cause $312 million in uncompensated damages annually. Victims sue operators personally. Operators lose everything.

The Million-Dollar Wake

Fort Myers Beach, Florida. Memorial Day 2024. An uninsured 35-foot Fountain powerboat throws a massive wake. Three smaller boats capsize. A child suffers permanent spinal injuries.

Settlement amount: $4.7 million. The operator owned a successful plumbing business, two rental properties, and a $800,000 primary residence. He now works for hourly wages. Bankruptcy couldn’t discharge the judgment because courts ruled gross negligence.

The Jet Ski Catastrophe

Lake of the Ozarks, Missouri. An uninsured PWC operator collides with a pontoon boat. Two retirees require emergency surgery. Helicopter evacuation costs alone: $67,000.

Total damages awarded: $1.2 million. The 28-year-old operator had no assets. Courts garnished his wages for 20 years. His credit score: destroyed. His ability to buy a home: eliminated. His marriage: ended under financial stress.

The Dock Demolition

Puget Sound, Washington. Wind pushes an anchored, uninsured sailboat into a private dock during a storm. The dock collapses, damaging three other vessels.

Property damage: $234,000. Environmental cleanup from fuel spills: $89,000. Legal defense costs: $45,000. The sailboat owner, a retired teacher, lost her entire pension in the settlement.

The True Cost of Being Uninsured

Insurance costs money. Not having insurance costs everything.

Average boat insurance premium: $200-$600 annually. Average uninsured accident cost: $287,000. The math speaks volumes. One incident without coverage equals 478 years of insurance premiums.

Financial Destruction Timeline

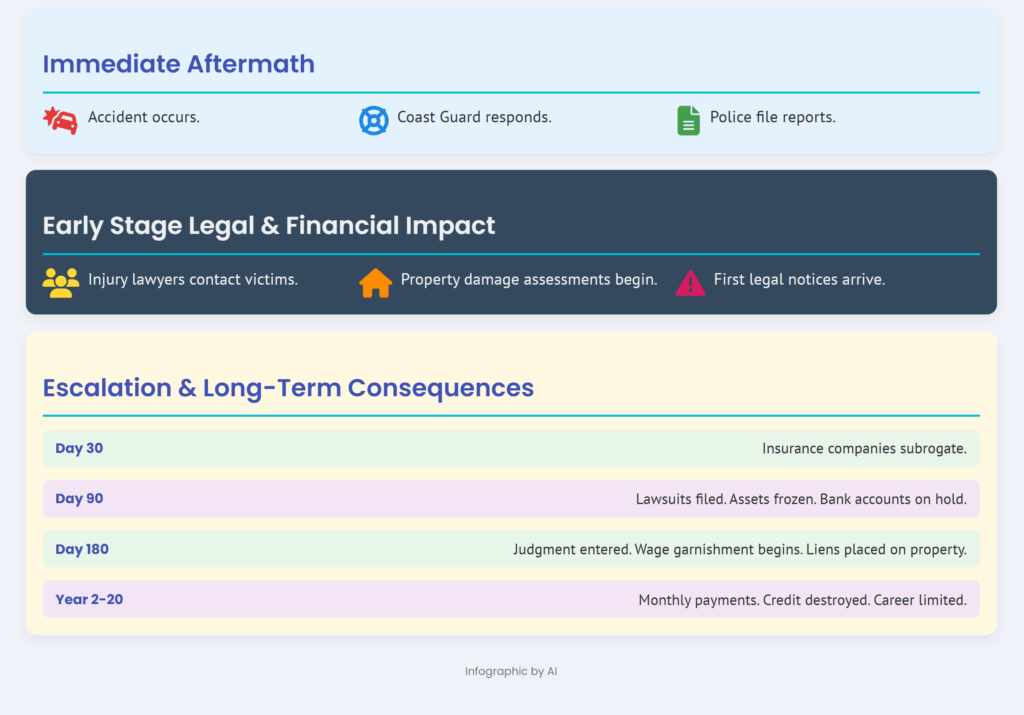

Day 1: Accident occurs. Coast Guard responds. Police file reports.

Day 7: Injury lawyers contact victims. Property damage assessments begin.

Day 30: First legal notices arrive. Insurance companies of damaged parties subrogate against you.

Day 90: Lawsuits filed. Assets frozen. Bank accounts placed on hold.

Day 180: Judgment entered. Wage garnishment begins. Liens placed on property.

Year 2-20: Monthly payments to victims. Credit destroyed. Career opportunities limited.

Hidden Costs Beyond Lawsuits

Legal defense without insurance averages $350 per hour. Maritime lawyers charge $500-$750 hourly. A simple property damage case costs $15,000-$30,000 to defend. Complex injury cases? $100,000+ in legal fees alone.

Your homeowner’s insurance won’t help. Auto insurance won’t cover it. Umbrella policies exclude uninsured watercraft. You stand alone against teams of attorneys.

| Accident Type | Average Settlement | Legal Defense Cost | Time to Resolve | Bankruptcy Protection |

|---|---|---|---|---|

| Property Damage Only | $45,000-$125,000 | $15,000-$30,000 | 6-12 months | Sometimes |

| Minor Injuries | $150,000-$500,000 | $30,000-$75,000 | 12-24 months | Rarely |

| Serious Injuries | $500,000-$5 million | $75,000-$250,000 | 24-48 months | Never |

| Fatality | $1 million-$10 million | $150,000-$500,000 | 36-60 months | Never |

Why Marina Requirements Matter More Than State Laws

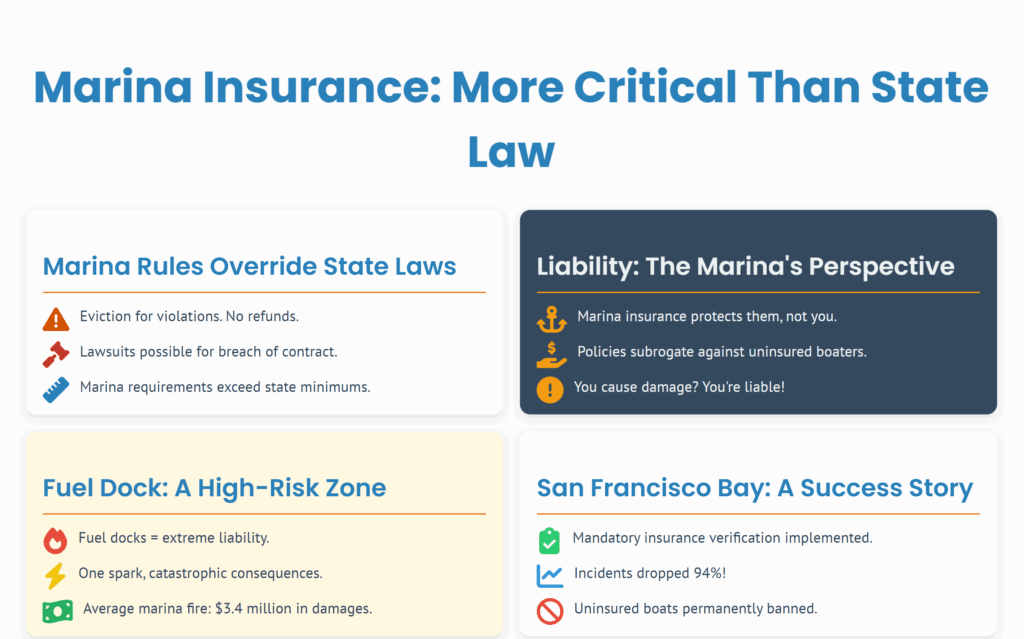

Your state doesn’t require insurance. Your marina does. Violate their requirements? Immediate eviction. No refunds. Potential lawsuits for breach of contract.

Marina requirements typically exceed state minimums. Coastal marinas demand $1-2 million liability. Great Lakes facilities require $500,000 minimum. Yacht clubs mandate specific coverage levels based on vessel value.

The Marina Liability Trap

Marinas carry insurance protecting themselves, not you. Their policies subrogate against uninsured boaters causing damage. You hit another boat in the marina? The marina’s insurance pays, then sues you for reimbursement.

San Francisco Bay Marina learned this enforcement works. After three uninsured boater incidents cost $1.8 million, they implemented mandatory insurance verification. Incidents dropped 94%. Uninsured boats? Banned permanently.

Fuel Dock Disasters

Fuel docks present extreme liability. One spark, one mistake, catastrophic consequences. The average marina fire causes $3.4 million in damage.

Lake Lanier, Georgia. An uninsured boater’s backfire ignited fuel vapors. Twelve boats destroyed. Marina structure severely damaged. Environmental cleanup required. Total damages: $7.2 million. The operator’s construction business, liquidated. His family’s future, devastated.

Loan and Mortgage Requirements Override Everything

Finance a boat? Insurance becomes mandatory regardless of state law. Lenders protect their collateral aggressively.

Banks require comprehensive coverage with maximum $1,000 deductibles. Credit unions demand agreed value policies. Marine lenders specify exact coverage requirements including:

- Hull coverage for full loan amount

- Liability minimums of $300,000

- Uninsured boater protection

- Salvage and wreck removal

- Environmental damage coverage

Miss one insurance payment? Lenders force-place coverage at 3x normal cost, adding it to your loan balance.

The Refinance Trap

Boat values depreciate. Loans don’t. Underwater financing creates insurance complications.

You owe $45,000. Boat’s worth $32,000. Lender requires insurance for loan amount. Standard policies cover actual value. Gap coverage costs extra. Many discover this during claims.

Your boat sinks. Insurance pays $32,000. You owe $45,000. The $13,000 difference? Due immediately. Default triggers entire loan balance acceleration.

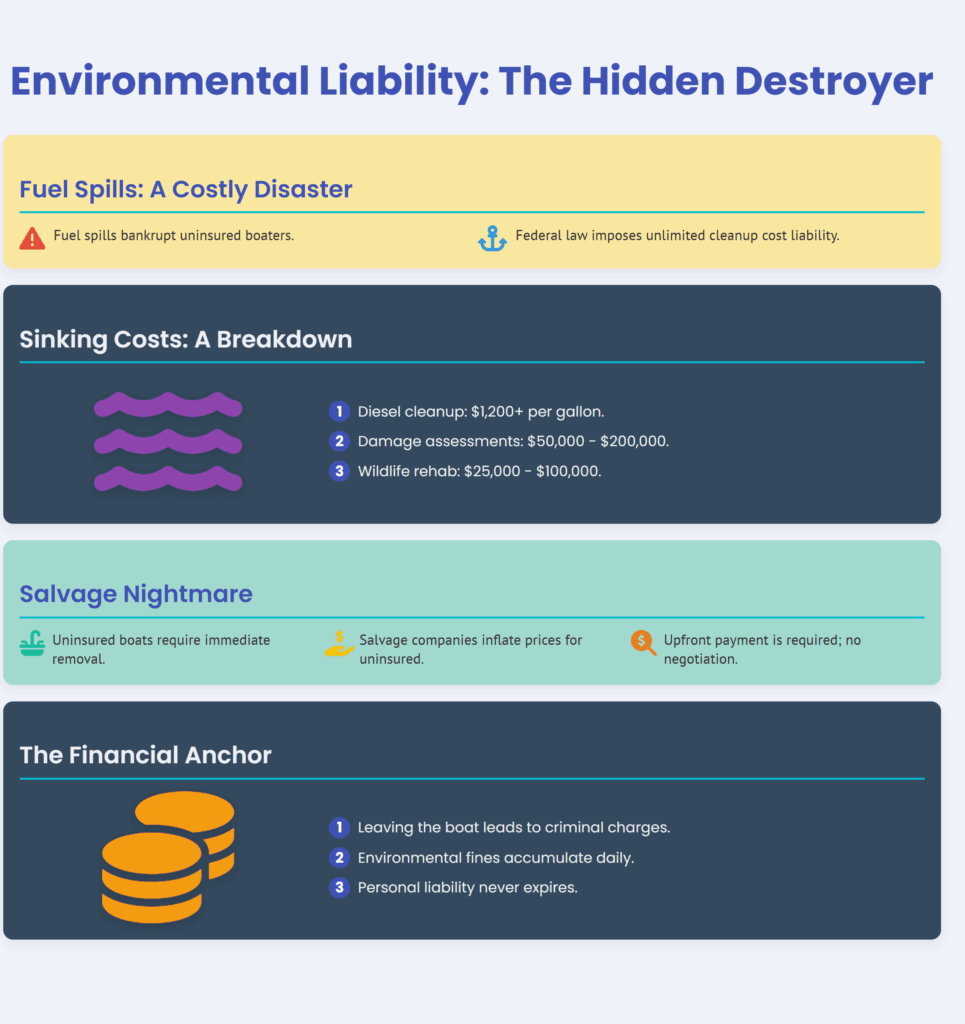

Environmental Liability: The Hidden Destroyer

Fuel spills bankrupt uninsured boaters faster than collisions. Federal law makes you liable for all cleanup costs. No limits. No exceptions.

Your boat sinks in Chesapeake Bay carrying 100 gallons of diesel. Cleanup costs: $1,200 per gallon minimum. Environmental damage assessments: $50,000-$200,000. Wildlife rehabilitation: $25,000-$100,000.

Total bill for a “simple” sinking: $287,000 average. Protected waterways, endangered species areas, or drinking water sources? Multiply by five.

The Salvage Nightmare

Your uninsured boat sinks. Law requires immediate removal. Salvage companies know you’re uninsured. Prices triple.

Standard salvage with insurance: $15,000-$30,000. Emergency salvage without insurance: $45,000-$150,000. Payment required upfront. No negotiation.

Leave the boat? Criminal charges. Environmental fines accumulate daily. Personal liability never expires. That sunken boat becomes a financial anchor dragging you under for decades.

Affordable Insurance Options for Every Boater

Basic liability insurance costs less than your monthly marina electricity bill. $50-$75 monthly protects against financial ruin.

Progressive offers liability-only coverage starting at $38 monthly for small boats. GEICO BoatUS provides basic protection from $42 monthly. Local marine insurers beat these rates 40% of the time.

Smart Coverage for Budget Boaters

Older boats don’t need comprehensive coverage. Liability-only insurance protects your assets while acknowledging your boat’s limited value.

Your 1995 Bayliner worth $8,000 doesn’t justify $200 monthly comprehensive coverage. But $55 monthly liability insurance prevents bankruptcy from accidents. The math becomes obvious.

Building Coverage Strategically

Start with state minimum liability. Add coverage annually as budget allows:

Year 1: Basic liability ($100,000/$300,000)

Year 2: Increase limits ($300,000/$500,000)

Year 3: Add uninsured boater protection

Year 4: Include personal property coverage

Year 5: Consider comprehensive if boat value justifies

This progression provides immediate protection while building comprehensive coverage affordably.

When Insurance Becomes Absolutely Mandatory

Certain situations demand insurance regardless of state requirements:

Boat Shows: Exhibitors require insurance proof. No exceptions.

Poker Runs: Event insurance mandatory. Personal coverage required.

Regattas: Racing exclusions mean special coverage needed.

Charter Operations: Commercial insurance required even for occasional paid trips.

International Waters: Mexico requires insurance. Canada demands proof. Bahamas won’t clear customs without coverage.

Cross state lines? Different rules apply. That Tennessee registration means nothing in Arkansas waters. Officers check insurance during safety inspections. Violations trigger immediate citations.

The Psychology of “It Won’t Happen to Me”

Every uninsured boater believes they’re careful enough. Statistics prove otherwise.

The average boater has one reportable accident every 8.7 years. Experienced operators actually have MORE accidents due to increased exposure and overconfidence. Twenty-year captains cause 31% of major accidents.

Your spotless record means nothing to the family you accidentally injure. Your decades of safe operation won’t resurrect the swimmer your propeller strikes. Your experience won’t repair the dock you demolish during unexpected weather.

Insurance isn’t about your skills. It’s about protecting others from your mistakes. Everyone makes them. Insurance ensures mistakes don’t destroy lives—yours and theirs.

Conclusion

Do boats have to have insurance? Legally, only in Arkansas and Utah, but practical requirements exist everywhere through marinas, lenders, and specific waterways. Operating without insurance risks unlimited personal liability averaging $287,000 per accident, with serious incidents reaching millions.

Contact three marine insurance agents this week. Compare liability-only quotes starting around $50 monthly. Verify your marina’s requirements. Check your loan documents for mandatory coverage levels.

Purchase at least state minimum liability coverage immediately. Increase limits annually as budget permits. Document your coverage properly. Display proof at your marina. Carry documentation aboard.

Your boat represents freedom and joy. Don’t let one accident without insurance transform that freedom into decades of financial bondage. Protect yourself, protect others, preserve your future. Today.

Frequently Asked Questions

What states require boat insurance by law?

Only Arkansas and Utah mandate insurance for all motorized boats. Arkansas requires $50,000/$100,000/$25,000 minimums while Utah mandates $25,000/$50,000/$15,000. However, specific counties, cities, marinas, and waterways in 31 other states require insurance despite no state mandate.

What happens if I get in an accident without boat insurance?

You become personally liable for all damages, medical costs, and legal fees. Victims can sue you directly, garnish wages, place liens on property, and seize assets. Average settlements reach $287,000, with serious injury cases exceeding $1 million. Bankruptcy rarely discharges maritime injury judgments.

Can I get liability-only boat insurance?

Yes, liability-only coverage costs $35-$75 monthly for most recreational boats. This protects your assets from lawsuits without expensive comprehensive coverage. It’s ideal for older boats where hull value doesn’t justify full coverage costs.

Does my homeowner’s insurance cover my boat?

Homeowner’s policies provide minimal boat coverage, typically $1,000-$1,500 maximum, and exclude liability for accidents. They cover small boats under 26 feet with less than 25 horsepower while in storage only. On-water accidents, larger boats, and liability claims require separate marine insurance.

Do marinas really require insurance?

Yes, most marinas mandate liability insurance ranging from $300,000 to $2 million. They verify coverage during slip agreements and can evict uninsured boats immediately. Marina requirements often exceed state minimums and include specific provisions for fuel spills and dock damage.