This post may contain affiliate links, which means I may receive a commission for purchases made through the links. I will only recommend products that I have personally used! Learn more on my Disclosure page!

Your dinghy sits there, modest and unassuming. Yet it’s your gateway to freedom, your tender to adventure, your compact escape from shore. So why do so many owners leave these vessels completely unprotected?

What Exactly Is Dinghy Insurance?

Dinghy insurance protects small boats under 20 feet, including inflatables, rigid inflatable boats (RIBs), sailing dinghies, and small motorboats. It’s specialized coverage designed for vessels that larger boat policies overlook or undervalue.

Think your homeowner’s policy has you covered? Think again. Most home insurance limits boat coverage to $1,500. Your new Mercury outboard alone costs triple that amount.

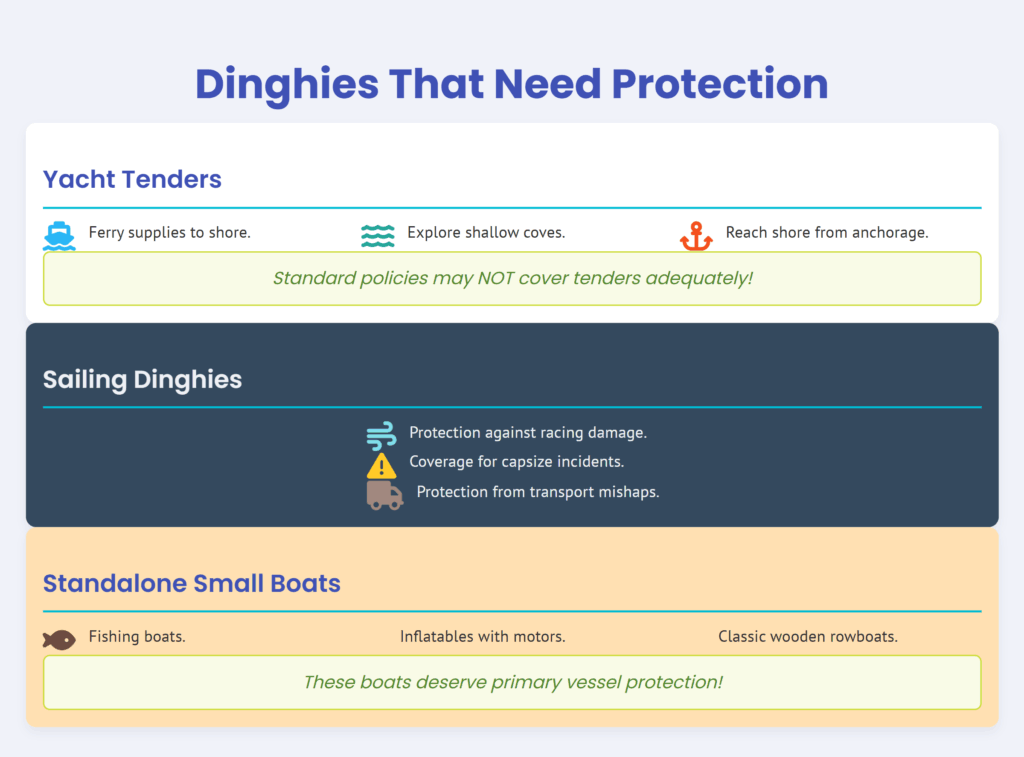

The Three Types of Dinghies That Need Protection

Yacht Tenders

You use it to ferry supplies, reach shore from anchorage, and explore shallow coves your mothership can’t access. Tenders face unique risks: being crushed between vessels, theft from docks, and damage during crane lifts. Standard yacht policies rarely provide adequate tender coverage.

Sailing Dinghies

From Lasers to Optis, from 420s to Flying Scots, these nimble craft need protection against racing damage, capsize incidents, and transport mishaps. Competition sailing adds liability concerns that recreational policies don’t address.

Standalone Small Boats

Your 14-foot aluminum fishing boat, that inflatable with a 20-horse motor, or your classic wooden rowboat. Each serves as a primary vessel, not just an accessory. They deserve primary vessel protection.

Coverage Options That Actually Matter

Agreed Value vs. Actual Cash Value

Agreed value means you and your insurer set the boat’s worth upfront. Total loss? You get that exact amount. No depreciation arguments. No haggling over market values.

Actual cash value factors in depreciation. Your five-year-old RIB worth $8,000 new pays out $4,000 today. The premium savings rarely justify the coverage gap.

Liability Limits That Protect Your Assets

A child falls overboard during a harbor tour. A wake swamps a kayaker. Your anchor drags into another boat. Liability coverage saves you from financial ruin. Most policies start at $100,000. Smart owners carry $300,000 minimum.

Personal Property Coverage

Your dinghy carries expensive gear:

- GPS units and chartplotters

- Safety equipment and flares

- Fishing tackle and diving gear

- Outboard motor accessories

- Custom covers and biminis

Basic policies exclude personal property. Enhanced coverage adds protection for items stored aboard or used with your dinghy.

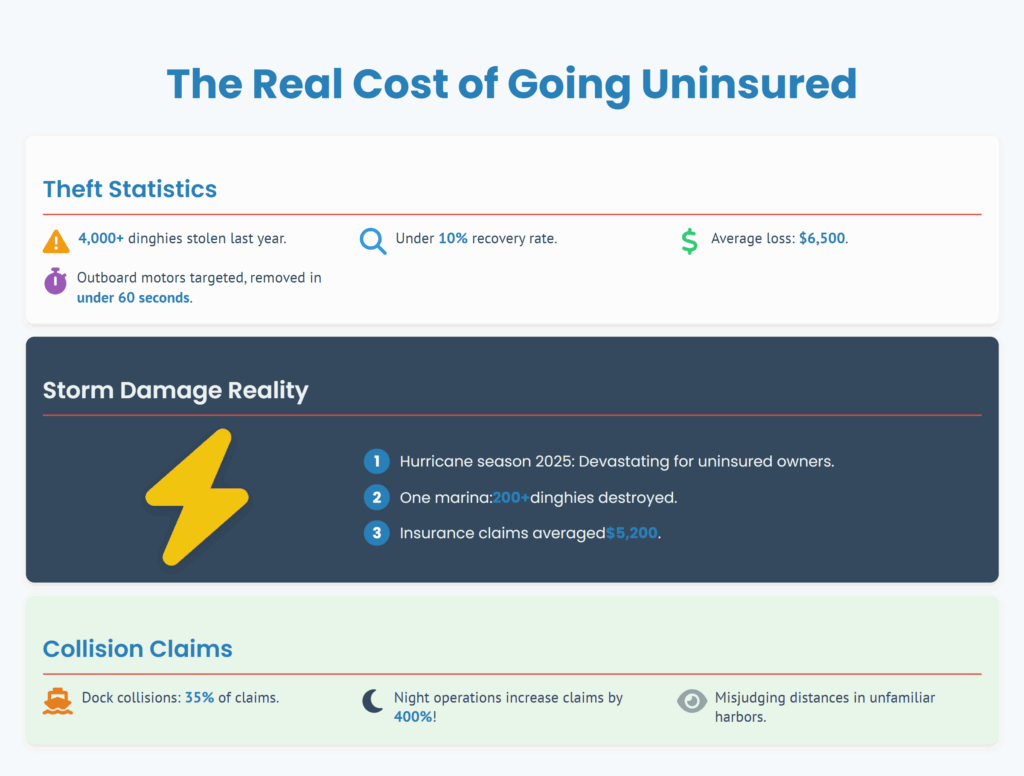

The Real Cost of Going Uninsured

Theft Statistics That’ll Make You Think Twice

Last year, over 4,000 dinghies disappeared from marinas, beaches, and yacht clubs. Average loss? $6,500. Recovery rate? Under 10%. Thieves target outboard motors specifically, removing them in under 60 seconds.

Storm Damage Reality

Hurricane season 2025 already proved devastating for uninsured dinghy owners. One Florida marina reported 200+ dinghies destroyed in a single storm. Insurance claims averaged $5,200. Uninsured owners? They’re still saving for replacements.

Collision Claims You Won’t See Coming

Dock collisions account for 35% of dinghy claims. Night operations increase claim frequency by 400%. Even experienced sailors misjudge distances in unfamiliar harbors.

Premium Factors You Control

Location, Location, Location

Store your dinghy in Maine? Expect lower premiums than Miami. Inland lakes cost less than coastal areas. Private storage beats public ramps. Your ZIP code drives pricing more than any other factor.

Security Measures That Slash Premiums

- Engine locks reduce premiums 10-15%

- GPS trackers cut costs another 10%

- Covered storage drops rates 20%

- Certified operator training saves 5-10%

- Alarm systems provide additional discounts

Your Claims History Follows You

Three claims in five years? Premiums double. Zero claims? Discounts accumulate annually. Choose your battles wisely. Small claims hurt more than they help.

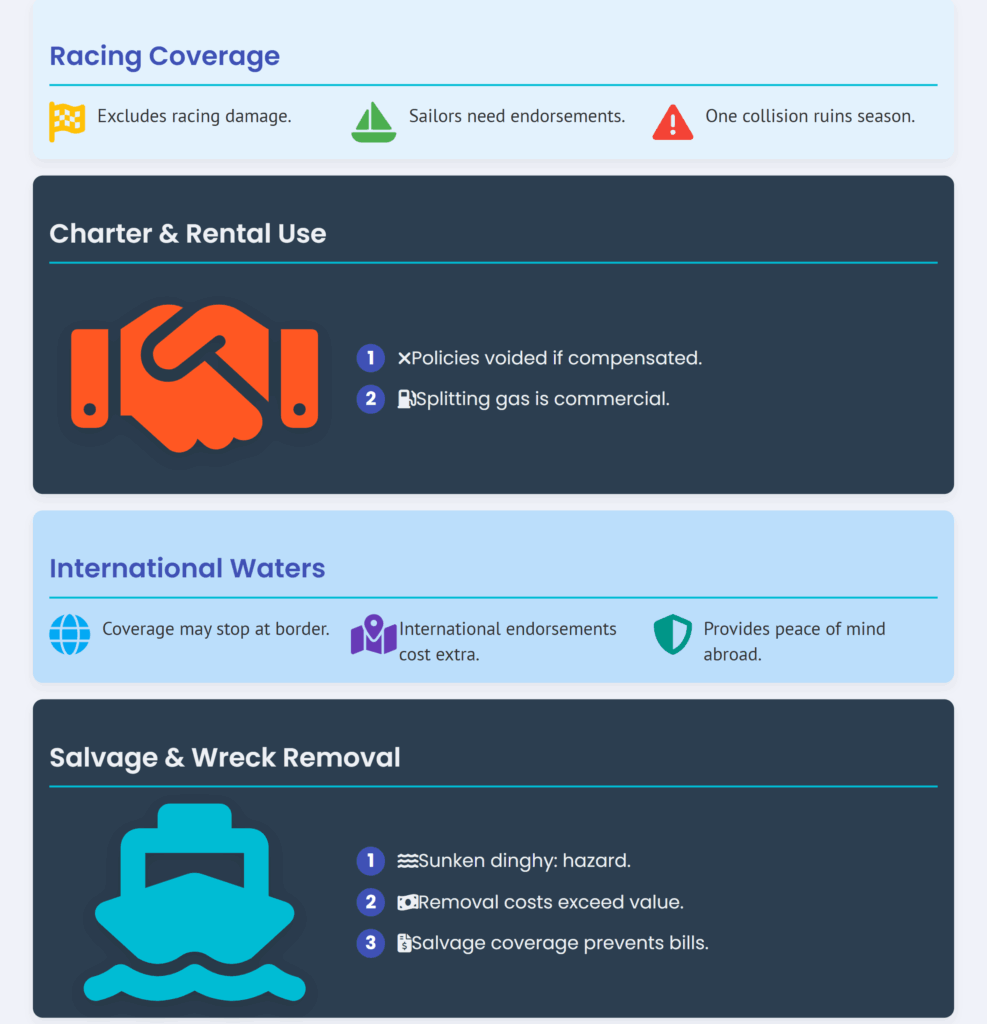

Specific Scenarios Your Policy Must Address

Racing Coverage

Standard policies exclude racing damage. Competitive sailors need specific endorsements. One protest collision ruins your entire season without proper coverage.

Charter and Rental Use

Letting friends borrow your dinghy? Standard policies void coverage during compensated use. Even splitting gas money technically constitutes commercial activity.

International Waters

Cruising to the Bahamas? Mexico? Your coverage might stop at the border. International endorsements cost extra but provide peace of mind abroad.

Salvage and Wreck Removal

Your sunken dinghy becomes an environmental hazard. Removal costs exceed vessel value quickly. Policies with salvage coverage prevent massive unexpected bills.

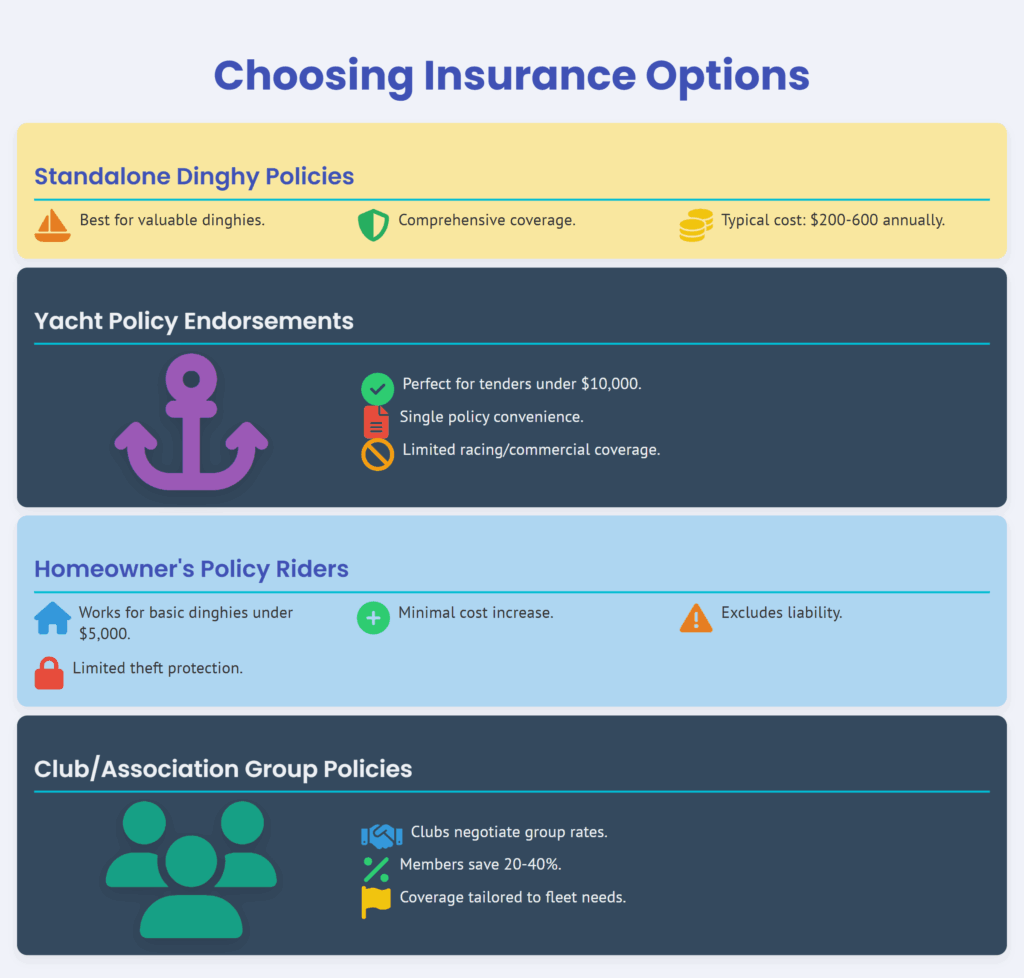

Choosing Between Insurance Options

Standalone Dinghy Policies

Best for valuable dinghies used independently. Comprehensive coverage tailored to small craft needs. Typical cost: $200-600 annually.

Yacht Policy Endorsements

Perfect for tenders under $10,000 value. Convenience of single policy management. Limited coverage for racing or commercial use.

Homeowner’s Policy Riders

Works for basic dinghies under $5,000. Minimal cost increase to existing policy. Excludes liability and offers limited theft protection.

Club or Association Group Policies

Sailing clubs negotiate group rates. Members save 20-40% through collective bargaining. Coverage tailored to specific fleet needs.

The Claims Process Simplified

Document everything immediately:

- Photograph damage from multiple angles

- Collect witness contact information

- File police reports for theft

- Save all repair estimates

- Track recovery and storage expenses

Response time matters. Report claims within 24 hours. Delays create coverage disputes. Insurance companies reward prompt reporting with faster settlements.

Red Flags in Policy Fine Print

Watch for these exclusions:

- Gradual deterioration (worn gelcoat doesn’t count)

- Freezing damage in northern climates

- Mysterious disappearance versus proven theft

- Wear and tear on outboard motors

- Damage during unauthorized use

Geographic restrictions hide everywhere. “Coastal waters” means different things to different insurers. Verify coverage areas explicitly.

Making Your Decision Today

Your dinghy represents freedom, adventure, and countless memories waiting to happen. Every trip without insurance gambles those possibilities against preventable financial loss.

Get quotes from three providers minimum. Compare coverage, not just premiums. Read actual policy documents, not marketing summaries. Ask about claims satisfaction rates and average settlement times.

September’s perfect for policy shopping. Insurers offer off-season discounts now through November. Rates increase 20-30% come spring when everyone remembers they need coverage.

Your dinghy deserves protection equal to its importance in your life. Whether it’s your solo escape pod or the family fun machine, proper insurance keeps adventures afloat. The water beckons. Your dinghy awaits. Protect them both with coverage that matches your passion for being on the water.