This post may contain affiliate links, which means I may receive a commission for purchases made through the links. I will only recommend products that I have personally used! Learn more on my Disclosure page!

For many folks, the idea of owning a boat is downright magical—imagine cruising across a peaceful lake at sunset, sharing laughter with close friends, and storing away new memories in the warmth of your heart. Yet, if you’re getting up in years, you might wonder: can you be too old to get boat insurance? The short answer is that most insurance providers won’t turn you away purely based on age. However, it’s wise to know how insurers actually size things up and what subtle rules or extra steps might come into play.

In the current market, insurance companies use some pretty detailed methods to decide who gets covered and at what price. Older boaters can draw added attention because of potential health or mobility issues—things like balance, reaction times, or chronic conditions. Still, the idea that you’ll be stamped “too old” and sent away is more rumor than reality. That said, your age can have an impact on certain parts of the policy, such as:

- Premium Costs: Will you have to pay a bit more because of higher perceived risk?

- Coverage Terms: Could there be extra conditions or limits due to your age or health situation?

- Eligibility Requirements: Is proof of good health or additional documentation requested?

In this comprehensive guide, we’ll shine a light on every corner of the topic—from basic industry norms and typical maximum age boundaries to specialized policies that cater specifically to older boaters. Let’s unravel the nuances of boat insurance for those in their golden years so you’ll feel steady at the helm, regardless of your birth date.

Understanding Age Factors in Boat Insurance

Age is more than just a number in the eyes of an underwriter. Insurance providers analyze countless details to decide whether to extend coverage. Although many older boaters maintain impeccable safety records, the industry relies on broad statistical trends linking advanced age to enhanced risk. This can include everything from health factors and diminished mobility to potential reflex slowdowns.

Nevertheless, the weighting of age in the final decision is rarely absolute. An 80-year-old who has decades of incident-free boating can present a better risk profile than a 45-year-old with multiple violations. Thus, boat insurance for older individuals operates on a balance of risk elements—age, health, and maritime experience all feed into the equation.

How Age Impacts Boat Insurance Eligibility

Insurance companies focus on two core areas when deciding eligibility for older boaters: health and operational competence. Health factors can carry particular significance. Conditions like arthritis, impaired vision, or slower reaction times may lead some underwriters to see an increased likelihood of accidents. Still, many insurers realize that age-related limitations can be proactively managed through adaptations—such as installing extra safety rails or using non-slip flooring.

On the flip side, demonstrated expertise can tip the scales in your favor. If you’ve successfully operated boats for decades without major incidents, that accumulated experience weighs heavily against any age-related concerns. While not every insurer requests a medical evaluation, some do if you’re above a certain age threshold—like 70 or 75. Ultimately, your personal health profile and record as a boater determine if any extra documentation will be necessary.

Therefore, can you be too old to get boat insurance? Usually not. What truly matters is the narrative you can provide: Are you a careful operator with the health and knowledge required to handle a vessel safely? Convincingly demonstrate these points, and the question of age becomes far less daunting.

Common Age Restrictions for Boat Insurance

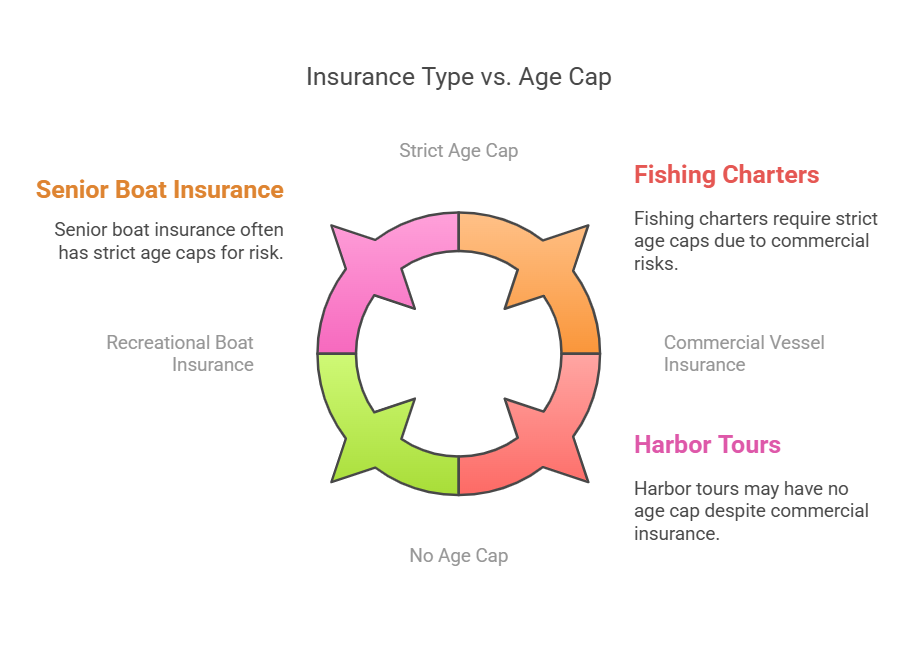

Although outright age bans are uncommon, some insurance providers impose maximum age boat coverage policies. For example, one company might choose 75 as an upper limit, while another sees no need for such a rule. These restrictions generally come into play when an insurer perceives a greater risk—be it from health or liability concerns.

When such age caps exist, they often vary based on whether the policy is commercial or recreational. Commercial vessel insurance may feature tighter constraints due to elevated liability. Conversely, a senior recreational boater might enjoy more flexibility if they can prove safe vessel operation and a consistent track record.

Below is a sample table illustrating how age might factor differently in two policy types:

| Policy Type | Typical Age Guidelines | Main Concerns |

| Recreational Boat Policy | No strict cap or ~75+ | Lower usage & liability |

| Commercial Boat Policy | ~65-70 | Higher liability risks |

The key to navigating these restrictions is early, proactive research. In some situations, companies are willing to make exceptions or grant coverage under special conditions. If one insurer denies you, don’t be discouraged—others may welcome your application, particularly if you’ve proven to be a conscientious boater.

Maximum Age Limits for Boat Insurance Coverage

Even though rigid upper-age cutoffs are rare, it’s prudent to learn how age limits boat insurance providers might structure their policies. Factors like the intended usage of the boat, its size, and the region where you plan to sail can influence these age limits. Below, we’ll unpack the two main categories of boat insurance—recreational and commercial—then explore geographical variations.

Standard Age Caps by Insurance Type

- Recreational Boat Insurance

Most senior boat insurance shoppers fall under this category. With recreational boating, insurers typically apply fewer restrictions because the overall risk is often lower than that of commercial operations. Some companies have no set maximum age limit at all, emphasizing your individual health status and safety record instead. Others may place a cap around 75 or 80, particularly if they factor age strongly into their risk models. However, these limits are by no means universal. Many older adults remain fully insurable well into their 80s, provided they demonstrate consistent upkeep of their vessels and a clean driving history. - Commercial Vessel Insurance

If you operate your boat for business—maybe offering fishing charters or harbor tours—the dynamic changes. Commercial insurance generally carries higher liability coverage, which leads some providers to enforce stricter age thresholds, such as capping coverage at 70 or 75. Insurers often worry that the physical demands of running a commercial operation might exceed what they consider safe for older owners or operators. Additionally, regulators sometimes impose their own guidelines for vessels used to transport passengers, influencing how insurers approach age.

Below is another table showcasing potential age caps for different policy types and their rationale:

| Policy Category | Potential Age Cap | Rationale |

| Recreational Use | None or ~75-80 | Lower liability; usage often seasonal or moderate |

| Commercial Use | ~65-75 | Higher liability; continuous operation, passenger safety |

Regional Variations in Age Restrictions

Geographical location plays a critical role in shaping how insurers treat older boaters. In the United States, states like Florida and California boast substantial populations of elderly boaters. As a result, boat insurance elderly policies may be more readily available and come with fewer restrictions. In these markets, competition fosters more inclusive underwriting because insurers don’t want to miss out on a large, potentially profitable demographic.

In contrast, insurance regulations in certain states or countries might directly or indirectly limit older boaters. European nations often impose rigorous maritime standards, which can impact coverage terms. That said, these standards can sometimes work in your favor. If you meet stringent licensing or safety requirements—like mandatory training programs or annual medical exams—insurers often see this as a reassurance of your competence, regardless of age.

Cross-Border Tip: If you plan to take your boat overseas or sail in international waters, confirm any cross-border policies. Some insurers are global or have reciprocal agreements, meaning you can carry your coverage across regions. Others might force you to procure local coverage when you enter new territories. In such scenarios, older boaters must pay particular attention to local age restrictions. Though it can be complicated, working with an experienced broker can illuminate a path through varied international rules, ensuring that a higher age doesn’t exclude you from the adventures you crave.

Options for Older Boaters Seeking Insurance

The notion that advanced age denies you from securing boat insurance is largely a misconception. While there might be additional hurdles, numerous paths remain open for senior boaters determined to protect their investments. From specialized programs geared toward older demographics to cost-saving measures that counterbalance higher rates, you aren’t short on older boater insurance options. Below, we detail how you can tap into these possibilities.

Specialized Insurance Programs

Senior-Focused Policies

A handful of providers have carved out a niche offering dedicated plans for older boat owners. Such policies often weigh experience more heavily than raw age, rewarding those who’ve accumulated decades of safe operation. They may also include perks like reduced premiums for passing advanced safety courses or for installing specific safety equipment.

Tailored Coverage Options

If you don’t use your boat intensively—say, you only set sail on summer weekends—an insurer might craft a coverage package that reflects this limited usage. Lower time on the water translates to reduced risk, which can shrink premium costs. Some plans also factor in navigational limits—only covering you in calmer inland lakes, for example, versus the open sea.

Locating these specialized offerings can be as simple as searching “senior boat insurance” online or contacting local boater associations. Often, these associations have leads on which insurers provide the best deals for older individuals who still love the thrill of open waters.

Requirements for Older Boaters

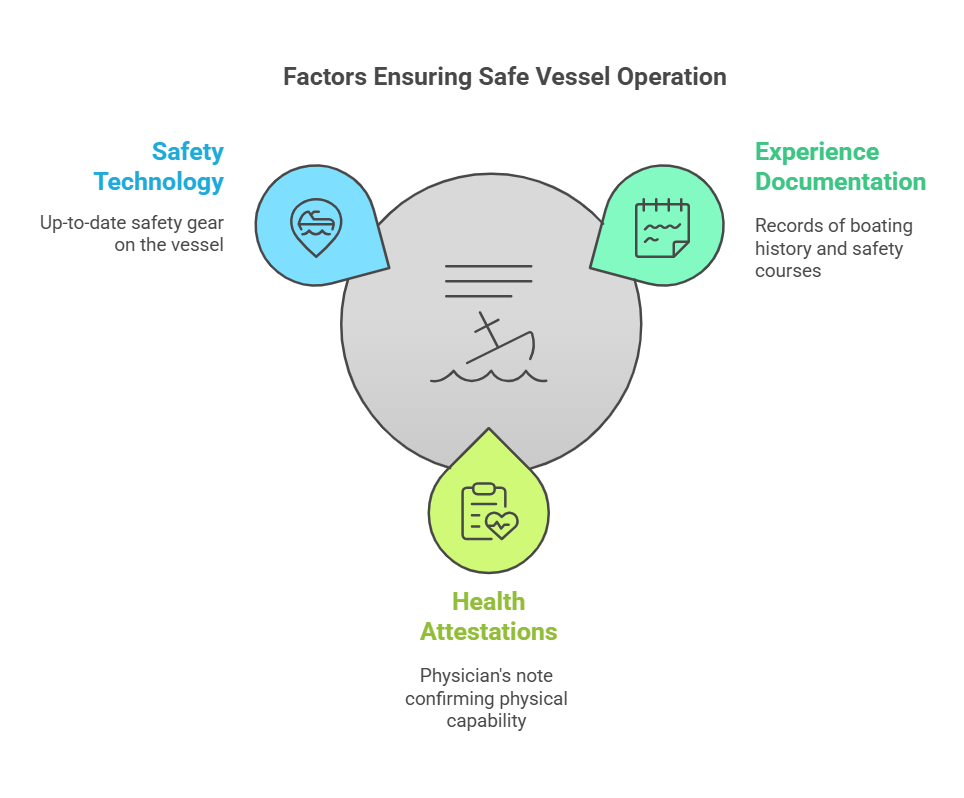

While specialized plans offer a friendly starting point, they generally have unique requirements to ensure mutual confidence. For instance, an insurer might ask for proof of your boating history, like a documented sailing log or a certificate from a recognized maritime training institute. Some may require a brief physician’s statement confirming you’re fit to operate the boat safely.

Another requirement could be a refresher safety course every couple of years, particularly for those in their 70s or 80s. These courses serve a dual purpose: you stay updated on essential protocols, and the insurer assures you’re proactive about maintaining your skills. In return, you often benefit from loyalty discounts or premium reductions tied to completed training.

Ultimately, meeting these additional requirements should be seen as a mutually beneficial safeguard, not a burdensome hoop to jump through. They help ensure that older boaters can continue enjoying their maritime hobbies confidently and that insurers can manage risk effectively.

Cost Implications for Senior Boaters

While age can factor into premium calculations, it doesn’t always lead to exorbitant costs. Many senior boaters pay only slightly more than their younger counterparts, particularly if they can demonstrate safe operating habits. The insurer’s primary concern is the likelihood of a claim, which is influenced by more than age alone. Accident history, boat condition, and the waters you traverse can overshadow any age-based risk assumptions.

Still, it’s useful to know the standard cost variables in play. Boat insurance elderly policies might include a modest surcharge if the underwriter deems health or reflex-related risks higher. However, insurers often offset these surcharges with discounts for experience or for outfitting your vessel with advanced safety features. Bundling your boat insurance with other policies—like homeowner’s or auto insurance—can further reduce your overall costs.

By staying open-minded, shopping around, and employing strategic measures—like periodic courses and strong documentation—older boaters often discover that ensuring robust coverage needn’t strain the bank account. It’s a matter of aligning your risk profile with an insurer that recognizes your wealth of experience, rather than fixating solely on your date of birth.

Overcoming Age-Related Insurance Challenges

Challenges do surface for older boaters, but being labeled “uninsurable” due to age alone is rare. More often, seniors must show evidence of preparedness and skill to satisfy underwriters wary of potential age-related hazards. Below, we detail tangible steps for overcoming these hurdles—from highlighting qualifications to adapting policies to your sailing habits.

Qualification Requirements

When doubts arise, insurers typically look for proof that you’re both physically and mentally equipped to operate a vessel safely. Having a robust set of qualifications in your back pocket can resolve those doubts swiftly.

- Documentation of Experience

Compile thorough records of your boating history. This could include logs of voyages, any previous insurance claims (or lack thereof), and evidence of completed safety or navigation courses. A proven record of cautious behavior often reassures underwriters, regardless of your age bracket. - Health and Fitness Attestations

If required, a brief exam or note from your physician can attest that you’re capable of handling physical tasks onboard. Though not all providers demand medical exams, voluntarily providing such evidence can be a proactive way to ease an insurer’s concerns. - Safety Technology

Show that you’re up-to-date with current safety gear—such as GPS trackers, life jackets, emergency beacons, and anti-slip decks. Maturity can breed caution, so demonstrating that your boat is well-equipped can work to your advantage.

Essentially, these qualifications serve to highlight your commitment to responsible boating. They also help define your unique profile—one that might weigh your wealth of experience more heavily than standard actuarial data about older individuals.

Policy Modifications and Alternatives

If a standard policy doesn’t suit your situation or if an underwriter hesitates to insure you at a high coverage level, consider adjusting your policy or exploring alternatives:

- Reduced Usage Coverage

If you boat solely on weekends or in fair-weather months, a limited usage plan could unlock lower premiums. The risk of a claim is less if the vessel isn’t constantly in action, thus insurers may be more flexible on age. - Co-Ownership or Co-Insured Arrangements

Some older boaters may partner with a younger family member. Sharing ownership or listing a younger operator on the policy can reduce the insurer’s perception of risk, as it indicates there’s someone else capable of handling the vessel if needed. - Liability-Only Policies

Older captains who maintain meticulously cared-for boats might accept less coverage on the hull or engine, focusing on liability. This approach lowers an insurer’s financial exposure, making it easier for them to cover an older applicant. - Boating Clubs and Group Policies

Certain associations offer group insurance plans. By joining a recognized boater club with a proven safety record, you could access more favorable underwriting terms, bridging any gap between your age and an insurer’s comfort zone.

Working with Insurance Brokers

If you encounter persistent objections or are overwhelmed by the intricacies of maximum age boat coverage, consider enlisting the help of a specialized insurance broker. Brokers differ from direct insurance agents in that they represent your interests rather than a single insurer. A broker’s role is to canvas the market for the best policy that meets your specific requirements.

Working with a broker carries distinct advantages for senior boaters:

- Experience: Brokers with a history of serving older clients typically know which insurers have the most lenient age-related policies or who might offer specialized programs.

- Negotiation: They can advocate on your behalf, highlighting your strong points (e.g., long track record, minimal claim history) to negotiate better premiums or coverage terms.

- Time Savings: Rather than contacting multiple insurers yourself, you can streamline the process through a broker who already has established relationships.

While brokers often charge fees, their expertise can be well worth it, especially if you’re navigating tricky age-based underwriting obstacles. By championing your cause, they help ensure you remain in control of the helm, regardless of the year on your birth certificate.

Tips for Securing Boat Insurance as an Older Boater

Information is power. Armed with the following tips, you can approach insurers with confidence, highlight your strengths, and lessen any concerns tied to age. Think of these strategies as best practices—steps that make you stand out in a sea of applicants and simplify the approval process.

Documentation Preparation

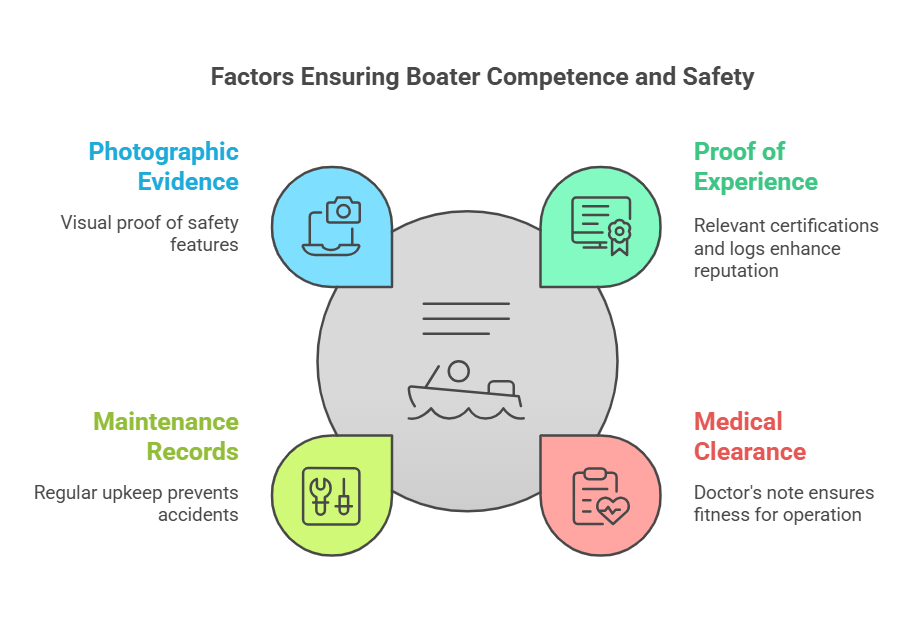

1. Gather Proof of Experience

Any relevant certifications—like completion of Coast Guard-approved safety courses—can solidify your reputation as a competent boater. If you maintain a log of your outings, detailing destinations, weather conditions, and any lessons learned, that’s even better.

2. Medical Clearance

While not universally mandatory, a doctor’s note certifying you’re fit to operate a watercraft can eliminate insurer doubts. Mention that you’re capable of climbing stairs or balancing on a rocking deck if needed.

3. Boat Maintenance Records

Insurers appreciate thorough upkeep. Show receipts for regular maintenance checks, upgrades (like new navigation equipment), or structural improvements. A well-maintained boat is less likely to cause or suffer accidents.

4. Photographic Evidence

Consider taking updated photos of your vessel, highlighting safety features like lifelines, non-slip surfaces, or emergency gear. Visual confirmations can reinforce statements about your commitment to safe boating.

Insurance Application Strategies

1. Apply in the Off-Season

Peak boating seasons—often spring and summer—can overload insurers with requests, making it harder to customize your policy. By applying off-peak, you’ll get more attentive service.

2. Be Honest and Thorough

Full disclosure about health conditions or mobility limitations prevents future disputes. If an insurer feels you withheld details, it could lead to claim rejections or policy cancellations.

3. Emphasize Safety

Use the application to emphasize active measures you take to prevent accidents—like mandatory life jacket usage or practicing safety drills. If you are part of a local maritime safety club, mention it.

4. Compare Multiple Providers

Never settle on the first quote. Different insurers weigh age factors differently. Gathering at least three to four quotes can reveal who offers the most favorable terms for your profile.

Conclusion: Can you be too old to get boat insurance?

Returning to that core question—can you be too old to get boat insurance? In most instances, the answer is an emphatic no. While it’s true that some insurers impose age-related restrictions or may require additional documentation, age itself seldom forms an absolute barrier to coverage. Many companies welcome seasoned boaters, especially those who can demonstrate impeccable experience and a proactive approach to safety.

Key Takeaways:

As you navigate the market, focus on highlighting your strengths. Provide proof of your boating experience, maintain a well-kept vessel, and consider specialized programs or brokers who cater to older demographics. If you encounter an insurer unwilling to budge, remember that alternatives likely exist—insurers who understand that mature boaters can bring wisdom and caution to the water.

Action Steps:

Begin by gathering essential documents, from your boating logs to any medical clearances you’ve obtained. Then, research various providers, including those that specifically note they work with senior clients. Finally, be open to policy modifications or specialized coverage plans. By doing so, you’ll position yourself to sail smoothly into your later years, reassured that your boat and your passion remain fully protected.