This post may contain affiliate links, which means I may receive a commission for purchases made through the links. I will only recommend products that I have personally used! Learn more on my Disclosure page!

Imagine this: You’ve just purchased a pre-owned 18-foot fishing boat from a neighbor. It’s sturdy, well-maintained, and perfect for weekend trips. But as you finalize the paperwork, the insurance company drops a bombshell: “We need a marine survey before coverage can begin.” Suddenly, you’re scrambling to find a surveyor, schedule an inspection, and wait days (or weeks) for results. What if there was a way to skip this step?

The truth is, while surveys are standard for many policies, there are scenarios where you can secure boat insurance without one. Let’s dive into the exceptions, risks, and smart strategies for boat owners who want to bypass the survey hassle—without leaving themselves vulnerable.

Why Do Insurers Demand Surveys? (And When Might They Bend the Rules?)

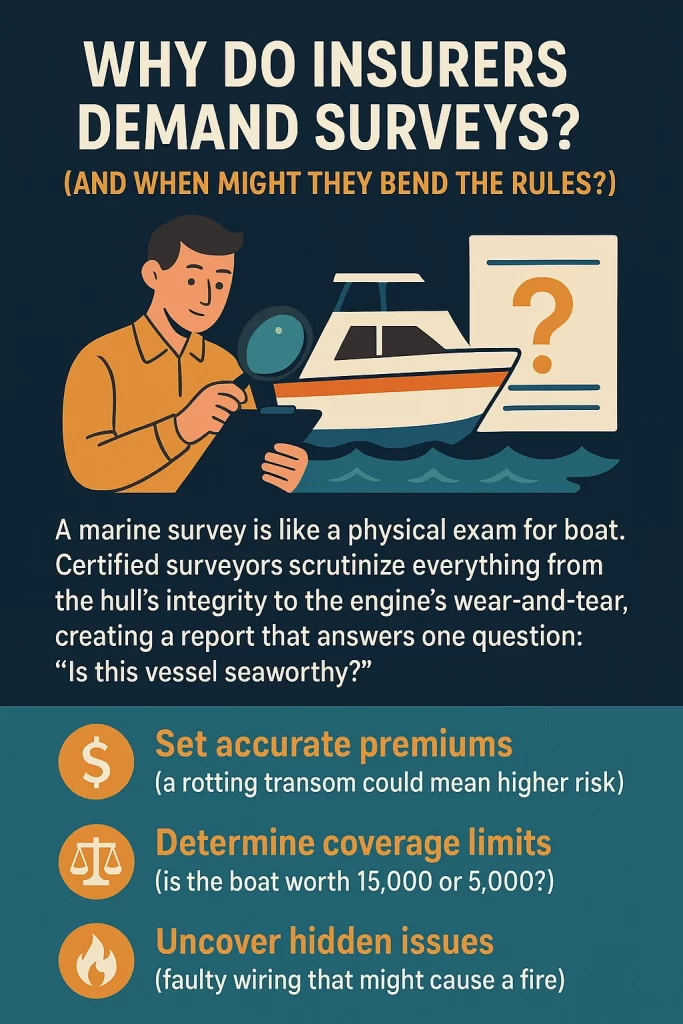

A marine survey is like a physical exam for your boat. Certified surveyors scrutinize everything from the hull’s integrity to the engine’s wear-and-tear, creating a report that answers one question: “Is this vessel seaworthy?” Insurers rely on these findings to:

- Set accurate premiums (a rotting transom could mean higher risk)

- Determine coverage limits (is the boat worth 15,000 or 5,000?)

- Uncover hidden issues (faulty wiring that might cause a fire)

But surveys aren’t cheap—they cost 300–300–800 on average—and they take time. Here’s when insurers might waive the requirement:

5 Scenarios Where You Might Skip the Survey

- Brand-New Boats

Fresh off the showroom floor? Most insurers accept the manufacturer’s warranty as proof of condition.- Example: A 2024 Boston Whaler with dealer maintenance records.

- Caveat: Once the warranty expires (usually 1–5 years), a survey becomes mandatory.

- Recently Surveyed Vessels

If your boat had a survey within the past 12–24 months (and no major changes occurred), insurers may accept the existing report.- Pro Tip: Provide the full survey, not just the summary. Highlight repairs made since the inspection.

- Low-Value Boats

Insurers often skip surveys for boats under 10,000–10,000–15,000 in value. Why? The potential payout is low, so the risk is manageable.- Common Examples: Small jon boats, older aluminum fishing boats, basic kayaks with motors.

- Low-Risk Usage

Boats used infrequently in calm, inland waters (think: small lakes) may qualify for “survey-free” policies.- Ideal Profile: A 16-foot pontoon used 10 times a year on a no-wake lake.

- Lay-Up Periods

If your boat is stored out of water (e.g., winterized), some insurers offer suspended coverage without a survey—just reactivate it before relaunching.

The Hidden Risks of Skipping a Survey

While dodging a survey saves time and money, it’s not always wise. Consider these pitfalls:

- Underinsurance: Without a survey, you might insure a 20,000boatfor20,000boatfor15,000, leaving you shortchanged if it’s totaled.

- Claim Denials: Missed damage (e.g., soft spots in the hull) could give insurers grounds to reject claims later.

- Safety Blind Spots: Surveys often catch life-threatening issues like gas leaks or compromised flotation foam.

Real-World Case: A Florida boater insured a 1998 Sea Ray without a survey. Six months later, the engine seized due to undocumented saltwater corrosion. The insurer denied the claim, citing “pre-existing condition.”

Survey-Free Insurance Options: A Side-by-Side Look

| Scenario | Pros | Cons |

|---|---|---|

| New Boat (Under Warranty) | Fast approval, no upfront costs | Limited to recent models |

| Low-Value Boat | Affordable, quick process | Risk of underinsurance |

| Lay-Up Storage | Lower premiums during off-season | Coverage gaps if boat is used |

| Recent Survey | Leverages past investment | Must meet insurer’s age requirements |

How to Convince Insurers to Waive the Survey

Even if your boat doesn’t fit the scenarios above, you can negotiate. Try these tactics:

- Provide Compelling Documentation

- Maintenance logs showing regular oil changes, hull cleanings, etc.

- Time-stamped photos of the engine, bilge, and electrical systems.

- Receipts for recent repairs or upgrades.

- Opt for Actual Cash Value (ACV) Policies

ACV coverage (which factors in depreciation) is less risky for insurers, so they might skip the survey. - Choose a Higher Deductible

Agreeing to pay $2,000 out-of-pocket per claim reduces the insurer’s risk, making them more flexible.

Alternatives to Traditional Insurance: Worth the Gamble?

If surveys are a dealbreaker, consider these options—but tread carefully:

Self-Insuring

- How It Works: Set aside $500/month into an emergency fund instead of paying premiums.

- Best For: Boats worth <$5,000 or owners with significant savings.

- Risk: A single accident could wipe out your fund.

Peer-to-Peer (P2P) Insurance Groups

- How It Works: Pool funds with other boaters to cover each other’s losses.

- Example: A local fishing club’s shared liability fund.

- Risk: No regulatory oversight; members might dispute claims.

FAQs: Can I get boat insurance without survey?

Q: Can I insure a 30-year-old sailboat without a survey?

A: It’s tough but possible. Focus on insurers specializing in classic boats. Submit detailed photos, maintenance records, and a boating resume showing your experience.

Q: What if I lied about the boat’s condition to skip the survey?

A: Big mistake. Insurers can deny claims (or cancel your policy) if they discover misrepresentation. Always disclose known issues.

Q: Do marinas require a survey for dockage?

A: Many do—especially for older boats. Even if your insurer waives the survey, the marina might not.

Q: Are survey waivers more common for certain boat types?

A: Yes. Insurers are more lenient with:

- Small powerboats under 20 feet

- Human-powered craft (canoes, rowboats)

- Boats with electric-only motors

Q: Can I get liability-only coverage without a survey?

A: Often, yes. Liability coverage (for damage you cause to others) doesn’t require a survey since your boat’s value isn’t insured.

Q: How do I prove my boat’s value without a survey?

A: Use a combination of:

- NADA Guides or BUC Value reports

- Purchase receipts

- Recent sale prices of comparable boats

Expert Tips for Survey-Free Success

- Build a “Boat Resume”

Document your experience (e.g., “20 years of boating, USCG safety course certified”) to reassure insurers. - Leverage Your Auto Insurer

Companies like State Farm or Allstate may waive boat surveys for existing customers with bundled policies. - Pre-Inspect Critical Systems

Hire a mechanic to check the engine and a marine electrician to inspect wiring. Submit their reports as proof of condition.

When a Survey Is Non-Negotiable

Despite the exceptions, some situations always demand a survey:

- Boats over 20 years old

- Vessels priced above $50,000

- Liveaboard sailboats or yachts

- After major incidents (groundings, collisions)

The Bottom Line: Is Skipping the Survey Smart?

For low-risk, low-value boats, survey-free insurance can be a win. But for anything else, remember: A survey isn’t just for insurers—it’s for you. That 500reportmightreveala500reportmightreveala5,000 repair need you never noticed.

If you do skip the survey:

- Double-check coverage limits

- Photograph every inch of the boat

- Keep meticulous maintenance records

In the end, the goal isn’t just to get insured—it’s to stay afloat financially when the unexpected strikes.