This post may contain affiliate links, which means I may receive a commission for purchases made through the links. I will only recommend products that I have personally used! Learn more on my Disclosure page!

Introduction

Boat insurance is your financial lifeline when maritime mishaps strike, encompassing everything from liability for injuries you cause to comprehensive protection against theft, fire, and natural disasters. Understanding the building blocks—liability, physical damage, medical payments, and uninsured boater coverage—empowers you to tailor a policy to your vessel’s size, value, and intended use. Policy types (agreed value versus actual cash value) dictate how much you receive after a total loss, while add‑ons like personal property, emergency assistance, and wreck removal fill crucial gaps. This is why every boat owner must understand Boat Insurance Coverage and Policies.

Premiums hinge on factors such as boat type, usage, location, and owner experience, but savvy choices—like adding safety features or opting for higher deductibles—can trim costs. Mastering the claims process and conducting regular policy reviews ensures your coverage stays aligned with evolving risks and regulations. Selecting a reputable, financially strong insurer with specialized marine expertise seals the deal, giving you peace of mind to savor every voyage.

Understanding the Foundations of Boat Insurance

Boat insurance serves as a specialized risk‑management tool that protects both vessel and owner against a spectrum of perils unique to the water. Liability coverage shields you if your boat injures someone else or damages another person’s property, paying medical bills, legal fees, and settlements up to your policy limit . Physical damage coverage—often called hull insurance—picks up repair or replacement costs if your boat suffers a covered peril, such as collision, fire, or vandalism.

Medical payments coverage steps in to cover medical bills for you and your passengers, regardless of fault, often up to predefined sublimits like $5,000 per person. Uninsured/underinsured boater coverage protects you when another boater at fault lacks adequate insurance, mirroring auto‑insurance protections on water.

These four pillars form the core of a standard boat insurance policy, but the precise definitions, limits, and exclusions vary widely among carriers. For instance, liability coverage may exclude water‑skiing injuries unless explicitly endorsed, while physical damage coverage might impose separate deductibles for named storms. Understanding these nuances requires careful examination of policy language and consultation with an experienced marine agent.

Policies also specify navigation limits—geographic boundaries within which coverage applies—so crossing from inland lakes into coastal waters without proper endorsement can void your claims. By mastering the foundational coverages, boat owners can avoid unpleasant surprises and ensure comprehensive protection for both the vessel and passengers.

| Coverage Type | What It Covers | Typical Limits | Pro Tip |

|---|---|---|---|

| Liability | Bodily injury & property damage you cause to others | $100K–$500K per occurrence | Increase limits if you charter or carry passengers |

| Physical Damage (Hull) | Repair/replacement after collision, fire, theft, etc. | Agreed‑Value or ACV | Choose Agreed‑Value for custom or vintage boats |

| Medical Payments | Medical bills for you & passengers, regardless of fault | $1K–$10K per person | Ensure limits cover typical ER costs |

| Uninsured/Underinsured | Damages when another boater at fault lacks coverage | Matches your liability limit | Vital in busy marinas or rental operations |

Policy Types—Agreed Value vs. Actual Cash Value

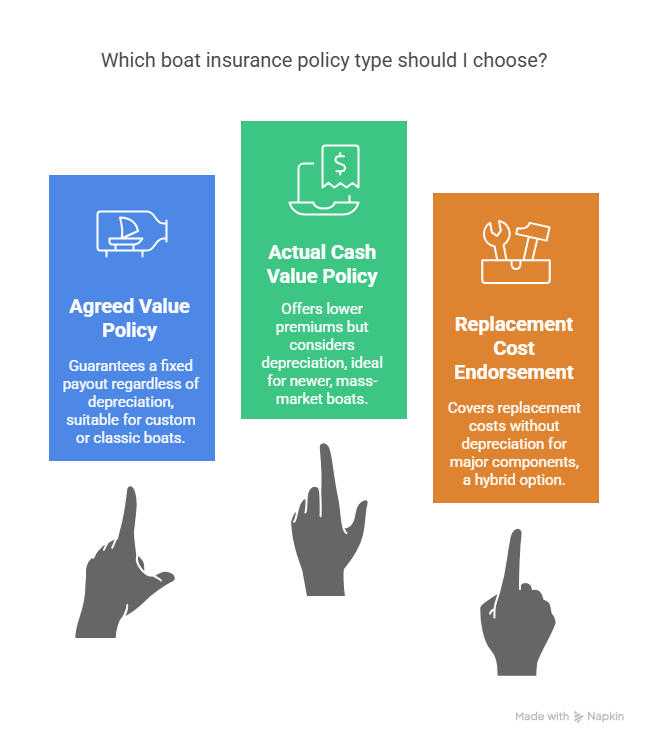

Boat insurance claims hinge dramatically on the policy type you choose: agreed value or actual cash value (ACV). An agreed‑value policy locks in the boat’s value at policy inception, guaranteeing you receive that amount in the event of a total loss, regardless of depreciation.

This option is particularly advantageous for custom builds, classic wooden boats, or heavily accessorized vessels, where market values can fluctuate unpredictably. While premiums for agreed‑value policies tend to be higher, the certainty at claim time often justifies the cost for owners unwilling to gamble on depreciated payouts.

In contrast, ACV policies calculate the boat’s worth at the time of loss, factoring in age‑related depreciation. If your 10‑year‑old cruiser suffers a total loss, the insurer will reference market guides and comparable sales to determine a payout that may be substantially lower than your original investment. ACV premiums are generally lower, making this a budget‑friendly choice for newer, mass‑market boats where depreciation curves are more predictable.

However, owners must assess whether potential savings on premiums outweigh the risk of an unexpectedly low settlement. Many marine insurers also offer a hybrid “replacement cost” endorsement, which covers the full cost to replace major components without depreciation but may still depreciate accessories.

Comprehensive vs. Collision—Covering All Angles

Comprehensive and collision coverages address two distinct categories of physical damage. Comprehensive coverage protects against non‑collision perils outside your control, such as theft, vandalism, fire, hail, or lightning strikes—ensuring that natural disasters or malicious acts don’t leave you footing a six‑figure repair bill.

For instance, if a fallen tree crushes your docked sailboat during a storm, comprehensive coverage pays for hull repairs and rigging replacement, minus your deductible.

Collision coverage, by contrast, responds when your vessel physically strikes another object—be it a submerged log, a pier piling, or another boat. Damages from a high‑speed docking mishap or an uncharted rock snagging your hull fall squarely under collision claims. Notably, collision coverage may also extend to injury expenses for pets on board, a niche benefit often overlooked by pet‑loving boaters.

Together, these coverages form a robust shield: comprehensive guards against unpredictable environmental and criminal events, while collision secures you during the dynamic act of boating itself.

Given the complex hydrodynamics and unseen hazards under the waterline, carrying both is highly recommended, especially for high‑value vessels.

🚩 Key Takeaway:

Never rely on just one form of physical‑damage coverage.

- Comprehensive protects against theft, fire, storms and vandalism.

- Collision kicks in when you hit another boat, dock or submerged object.

Together they form your safety net on the water.

Essential Add‑On Coverages

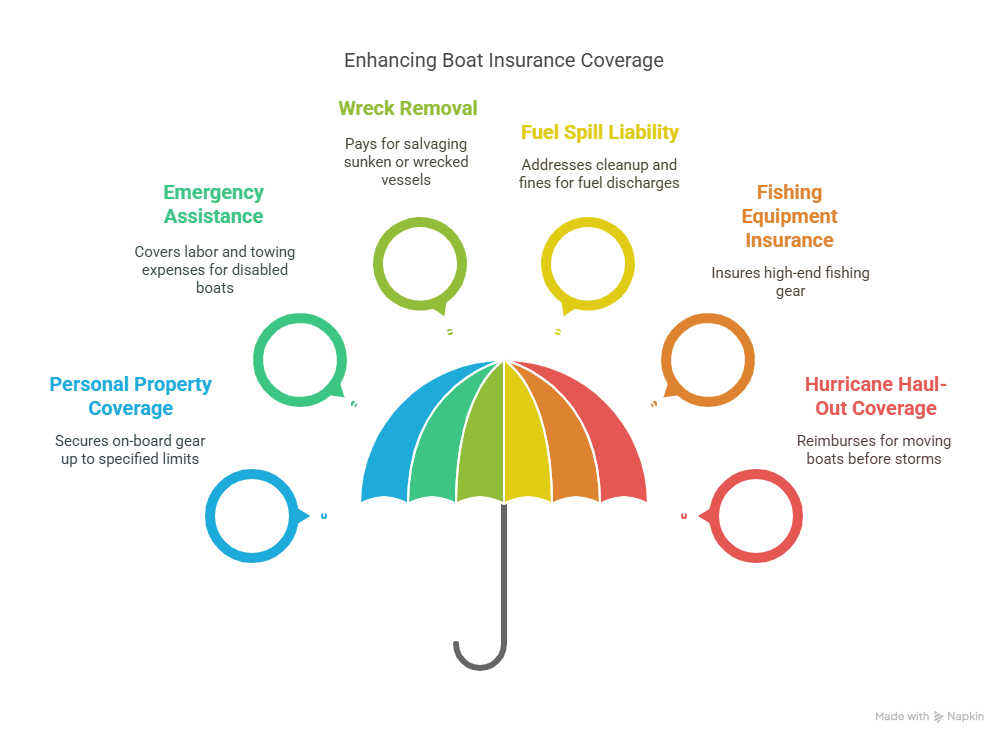

Standard policies lay the groundwork, but optional endorsements tailor protection to your lifestyle and risk profile. Personal property coverage secures on‑board gear—fishing rods, electronics, safety equipment—often up to limits between $500 and $5,000 per item category. Emergency assistance or on‑water towing covers labor and tow expenses if your boat becomes disabled far from shore, a service that can cost hundreds per incident if paid out of pocket.

Wreck removal pays to salvage a sunken or wrecked vessel, a process that can reach tens of thousands of dollars in deep or environmentally sensitive waters. Fuel spill liability addresses cleanup and environmental fines if your boat accidentally discharges fuel, imperative in regulated coastal zones.

Additional niche options include fishing equipment insurance for high‑end rods and reels, and hurricane haul‑out coverage that reimburses for professionally moving or hauling your boat ahead of named storms.

Selecting the right add-ons bundle depends on your vessel’s typical use—freshwater fishing versus blue‑water cruising—and local regulatory requirements. Together, these extras plug coverage gaps and deliver peace of mind in specialized scenarios.

Premium Drivers and Cost‑Saving Strategies

Boat insurance premiums reflect a blend of vessel characteristics, owner profile, and operating environment. Insurers weigh boat type and value heavily—luxury yachts and performance powerboats attract higher rates than modest pontoons—while engine size and vessel age also influence risk assessments.

Usage patterns matter too: boats kept in saltwater or used commercially face stiffer underwriting than freshwater recreational craft. Location is critical; marinas in hurricane-prone regions or high-theft areas drive up premiums, as do long navigation ranges into open seas.

“I trimmed my annual premium by 12% simply by completing a certified boating safety course—worth every minute on the water!”

– A savvy boat owner’s real experience

Owner experience and safety training can earn discounts. Completing a certified boating safety course or maintaining a claim-free history signals lower risk, trimming premiums by up to 15% in some programs. Installing GPS trackers, bilge alarms, and fire suppression systems can unlock further credits, as carriers recognize the reduced likelihood of total loss.

Deductible selection provides another lever: opting for a 5% hull deductible rather than 1% can slash premiums significantly, though at the expense of higher out‑of‑pocket costs in a claim.

By analyzing these drivers, boat owners can adopt targeted strategies—enhancing safety features, adjusting deductibles, or staging their boat in lower‑risk locations—to optimize insurance spend without compromising protection.

Mastering the Claims Process

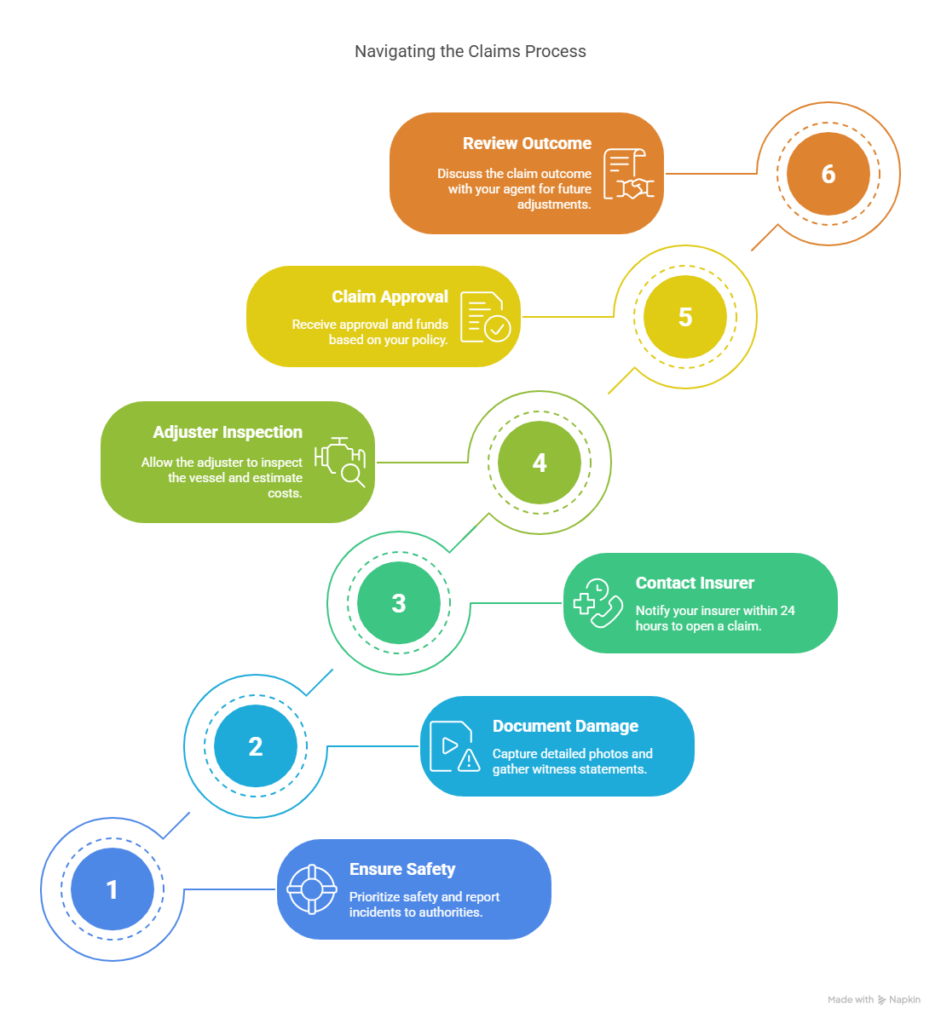

When mishaps occur, a smooth claims experience hinges on prompt action and thorough documentation. First, ensure everyone’s safety and, if necessary, call maritime authorities or the Coast Guard for rescue and incident reporting. Next, photograph all damage from multiple angles, capturing hull breaches, equipment loss, and surrounding conditions before any cleanup begins. Collect witness statements and maintain logs of emergency towing or repair expenses.

Contact your insurer immediately—ideally within 24 hours—to open a claim file and receive guidance on authorized repair yards or salvage operations. An adjuster will inspect the vessel, verify coverage, and estimate repair costs. Transparency and detailed records accelerate claim approval; undisclosed pre‑existing damage or unauthorized repairs can lead to partial denials. Once approved, you’ll receive funds per your policy’s valuation method—agreed value or ACV—minus applicable deductibles.

After resolution, review the claim outcome with your agent to address any coverage gaps exposed during the process. Prompt, organized claims handling not only restores your vessel but also informs smarter policy adjustments for future seasons.

Choosing the Right Insurance Provider

Selecting an insurer isn’t solely about price; financial stability, marine expertise, and customer service quality are equally vital. Review carrier financial strength ratings from agencies like A.M. Best or Standard & Poor’s to ensure they can honor large claims decades from now. Seek companies specializing in marine insurance—these underwriters understand vessel construction, navigation risks, and maritime law nuances better than generalist insurers.

Examine customer reviews and J.D. Power satisfaction surveys to gauge responsiveness during quoting and claims. A provider offering 24/7 marine helplines, digital claim filing, and partnerships with national repair networks delivers superior support when you’re stranded offshore. Policy flexibility—such as adjustable navigation limits and modular endorsements—allows your coverage to evolve as your boating habits change.

Finally, leverage independent agents to compare multiple carriers, balancing premium, coverage breadth, and service quality to find the optimal match for your boating lifestyle.

Legal Requirements and Regulatory Compliance

Boat insurance regulations vary widely across jurisdictions. While no federal mandate exists in the U.S., many lenders require hull and liability coverage as a financing condition. Marinas often demand proof of insurance, including specified liability minimums, before granting docking privileges. Some states—like Louisiana and Florida—impose specific insurance requirements for vessels above certain lengths or horsepower ratings.

Furthermore, international voyages trigger compliance with foreign maritime laws and the International Convention on Civil Liability for Oil Pollution Damage (CLC) if carrying fuel beyond personal use. Noncompliance can result in hefty fines, impoundment, or denial of entry to foreign ports. Staying abreast of local statutes, marina rules, and financing contracts ensures uninterrupted enjoyment of your vessel and avoids legal entanglements.

The Importance of Regular Policy Reviews

📋 Annual Boat‑Policy Review Checklist

- ✔ Verify vessel value and adjust Agreed‑Value if upgraded

- ✔ Confirm navigation limits cover any new cruising areas

- ✔ Add or remove endorsements (e.g., fuel spill, emergency towing)

- ✔ Update personal‑property limits for new electronics or gear

- ✔ Reassess liability limits if you’ve added passengers or chartered

- ✔ Check for new safety‑feature discounts (GPS, alarms, fire suppression)

As your vessel ages, acquires new equipment, or shifts usage patterns, your insurance needs morph accordingly. Annual policy reviews help identify underinsured areas—such as added electronics or upgraded sails—and adjust coverage limits before gaps emerge. Conversely, dropping unused endorsements (e.g., commercial liability if you cease charter operations) trims unnecessary costs. Life changes—moving to a coastal retirement community or switching from inland lakes to ocean cruising—alter risk profiles and warrant navigation‑limit updates.

Engage your agent yearly to audit your policy, compare market offerings, and secure any new discounts for safety upgrades or loss‑free seasons. Proactive reviews keep your protection aligned with real‑world circumstances, ensuring that no storm—literal or financial—catches you off guard.

Conclusion—Boat Insurance Coverage and Policies

Boat insurance transcends mere legal formality: it is the anchor that steadies your financial security when unpredictable waves of liability, accidents, or natural disasters threaten your maritime investment. By dissecting core coverages—liability, physical damage, medical payments, and uninsured boater protections—alongside policy types, add‑ons, premium drivers, and claims strategies, you gain mastery over your risk landscape.

Choosing a seasoned marine insurer, complying with legal mandates, and conducting regular policy audits fortify your shield. Ultimately, well‑structured boat insurance transforms every voyage from a leap of faith into a calculated adventure, allowing you to chart courses with confidence, knowing that calm seas or storms ahead, your investment and loved ones remain safeguarded

FAQs: Boat Insurance Coverage and Policies

1. What does boat insurance typically cover?

Most policies stitch together liability coverage—which pays if you injure someone else or damage their dock or boat—with physical damage (hull) coverage, handling repairs when your own vessel meets a storm, a rock, or vandalism. They usually include medical payments for you and your passengers no matter who’s at fault, and uninsured/underinsured boater protection that steps in when the other captain sails off without insurance.

2. Do I legally need boat insurance?

Only a couple of states mandate boat insurance for larger motorboats, typically requiring at least $50,000 of liability coverage before you shove off. But even where the law is silent, your lender (if you financed the boat) or your marina slip agreement often insists on proof of coverage, making insurance effectively as essential as life jackets on deck.

3. What types of boat insurance policies exist?

You’ll see two headline choices: an agreed‑value policy, where you and the insurer agree up front on your boat’s worth (ideal for custom or classic vessels), or an actual cash value (ACV) policy, which factors in age and wear so you get market value at the time of loss. Some carriers also offer liability‑only plans if you just need to cover damage to others, plus hybrid “replacement cost” endorsements that erase depreciation on major parts while still applying it to accessories.

4. How do Agreed Value and Actual Cash Value differ?

With agreed value, you set your price at policy start—so if a total loss occurs, you collect that exact sum, no surprises—even if the market tanked overnight. An ACV policy, by contrast, peeks at comparable sales and depreciation tables when you file a claim, so your check might be smaller than your original outlay, even though your premiums were lower all along .

5. What will boat insurance cost me?

Expect to shell out roughly 1–5% of your boat’s insured value per year—so a $50,000 cruiser might cost between $500 and $2,500 annually, depending on horsepower, usage, and where you berth it. Liability‑only plans start closer to $200–$300 a year, while comprehensive coverage on high‑end yachts can climb into the thousands once you pile on add‑ons.

6. Which factors drive my premium up or down?

Insurers eyeball your boat’s type, size, and horsepower—luxury yachts and speedboats carry heftier rates than humble pontoons. They also weigh your navigation area (inland lakes versus hurricane‑prone coasts), your boating experience and safety training, plus any onboard alarms, GPS trackers, or fire‑suppression gear you’ve installed.

7. What optional coverages should I consider?

Beyond the basics, savvy boaters tack on personal property coverage for rods, electronics, and cushions, emergency assistance/towing for on‑water breakdowns, and wreck removal to pay for salvage if you sink in deep or sensitive waters. Fuel‑spill liability can pick up environmental fines, while hurricane haul‑out endorsements cover proactive storm relocations.

8. How do I file a boat insurance claim?

First, secure safety—call the Coast Guard if needed—and snap photos of damage from every angle before tidying anything up. Then alert your insurer (within 24 hours if possible) via their app or hotline, supply your images, witness statements, and repair bills, and work with the adjuster to settle on a payout under your agreed‑value or ACV terms.

9. Are my boat trailer and dinghy covered?

Most policies let you add your trailer (and even that inflatable tender) for a small extra premium—so damage or theft on the highway is protected under your boat plan, though injuries during towing fall back on your auto policy.

10. How can I lower my boat insurance premiums?

Take a state‑approved boating safety course, bundle your boat and auto policies with one insurer, raise your deductibles, and install theft‑deterrent or safety gear like GPS trackers and bilge alarms—each move can shave 5–15% off your rate.

11. What key questions should I ask my agent?

Probe exclusions (“Which waters void my coverage?”), limits (“What’s the deductible for named storms?”), and endorsements (“How much for wreck removal or emergency towing?”). Ask about multi‑policy and safety discounts, and clarify how personal effects and trailers are handled to avoid surprises later.

12. How do I shop for boat insurance quotes?

Arm yourself with your hull ID, boat make/model/year, engine specs, and intended usage, then tap specialized marine insurers or comparison tools for instant estimates. Finally, run the numbers past an independent agent to ensure navigation limits and add‑ons truly match your cruising plans.