This post may contain affiliate links, which means I may receive a commission for purchases made through the links. I will only recommend products that I have personally used! Learn more on my Disclosure page!

Boat insurance claims face denial rates approaching 30% for claims over $50,000, according to marine insurance industry data, with technical violations and documentation failures leading to catastrophic financial losses for unprepared boat owners. The marine insurance industry paid out $2.1 billion in claims during 2023 while denying approximately $900 million in submitted claims based on policy exclusions and technical violations.

The pattern is consistent across every major marine insurer. Owners pay premiums faithfully for years, suffer a loss, file a claim, and discover their coverage contained exclusions they never understood. The financial devastation that follows destroys savings, retirement plans, and futures.

You’re about to discover the specific exclusions causing most denials, documentation that prevents rejection, real alternatives when claims get denied, and protective strategies that ensure coverage when you need it most.

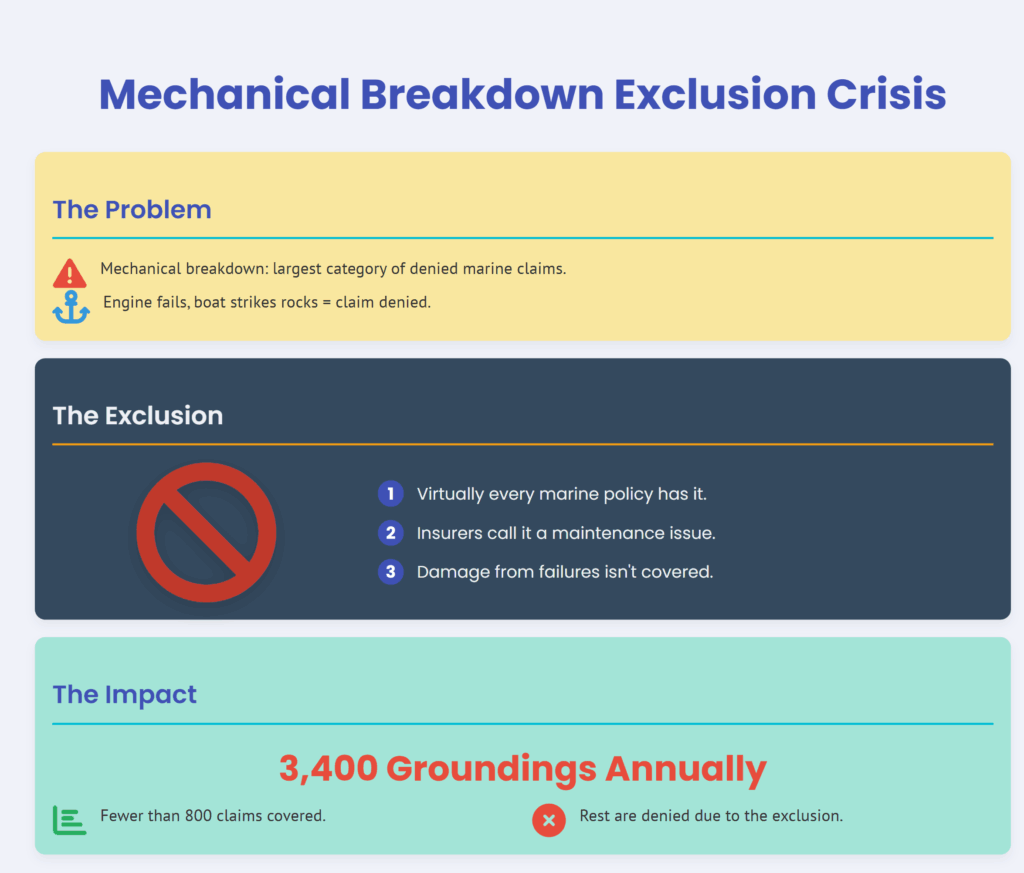

The Mechanical Breakdown Exclusion Crisis

Mechanical breakdown represents the single largest category of denied marine insurance claims. Your engine fails, your boat strikes rocks, total loss occurs. Insurance response? Mechanical breakdown caused the grounding. Claim denied.

This exclusion appears in virtually every marine policy. Insurers argue mechanical failures represent maintenance issues, not insurable events. The resulting damage—grounding, sinking, collision—becomes irrelevant once mechanical breakdown initiates the chain of events.

The numbers tell a devastating story. Engine failures cause approximately 3,400 groundings annually. Insurance covers fewer than 800 of these claims. The rest face denial under mechanical breakdown exclusions.

Real Numbers From Marine Insurers

Marine insurance companies report consistent denial patterns:

| Denial Reason | Percentage of Denials | Average Claim Amount | Typical Scenario |

|---|---|---|---|

| Mechanical Breakdown | 34% | $67,000 | Engine failure leads to grounding |

| Maintenance/Wear | 28% | $43,000 | Gradual deterioration causes failure |

| Navigation Limits | 19% | $125,000 | Damage outside covered area |

| Operator Error | 11% | $89,000 | Inexperienced operator causes damage |

| Late Reporting | 8% | $56,000 | Claim filed beyond time limit |

These aren’t estimates. Marine insurers report these figures to state insurance commissioners annually. The data remains remarkably consistent year over year.

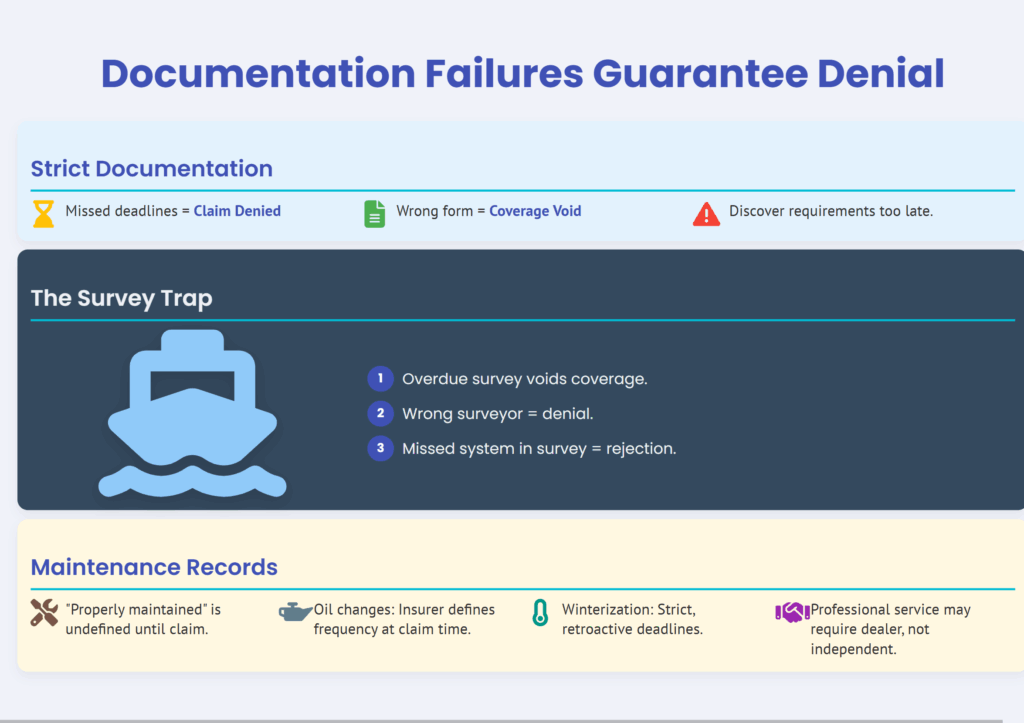

Documentation Failures That Guarantee Denial

Insurance companies require specific documentation within strict timeframes. Miss a deadline by 24 hours? Claim denied. Submit the wrong form? Coverage voided.

The typical boat owner discovers documentation requirements during the claim process. Too late. Insurance companies enforce these requirements ruthlessly, knowing most policyholders can’t comply retroactively.

The Survey Trap

Policies requiring annual surveys create massive denial opportunities. Survey overdue by one day? Coverage potentially void. Wrong surveyor certification? Claim denied. Survey missed one system? Grounds for rejection.

Insurance companies know approximately 40% of boats operate with overdue surveys. They collect premiums anyway. When claims arrive, they cite survey requirements for denial.

Maintenance Record Requirements

“Properly maintained” appears in every policy. Define “properly.” You can’t. Insurance companies define it during claims. Retroactively. Against you.

Oil changes every 100 hours? Some insurers say 50. Winterization by October 15? They wanted October 1. Professional service? They require dealer service, not independent mechanics.

Named Storm Deductibles: The Hidden Coverage Killer

Standard deductible: $1,000. Named storm deductible: 10% of hull value. Most discover this during hurricanes.

Your $300,000 boat suffers $100,000 hurricane damage. Your deductible isn’t $1,000. It’s $30,000. The special deductible applies whenever a named storm exists within 100 miles, regardless of actual weather at your location.

Florida boats face this reality constantly. Hurricane forms near Cuba. Miami experiences light rain. Named storm deductible applies. Damage from normal weather during the storm’s existence triggers the massive deductible.

Territory Violations Nobody Understands

“Coastal cruising” means different things to different insurers. Some define it as 25 miles offshore. Others say 75. Some exclude specific areas without clear notification.

GPS technology makes territory violations easy to prove. Insurance investigators pull vessel tracking data. That fishing trip 30 miles offshore last summer? Your policy covered 25 miles. Claim denied for territory violation, even if the loss occurred within covered areas.

International Water Complications

Cross into Bahamian waters without written permission? Coverage void. Enter Mexican waters temporarily? Policy cancelled retroactively. Canadian waters seem safe? Not without specific endorsement.

The three-mile limit creates confusion. State waters end. Federal waters begin. Insurance coverage might end too. Most policies require specific federal water endorsements for coverage beyond state boundaries.

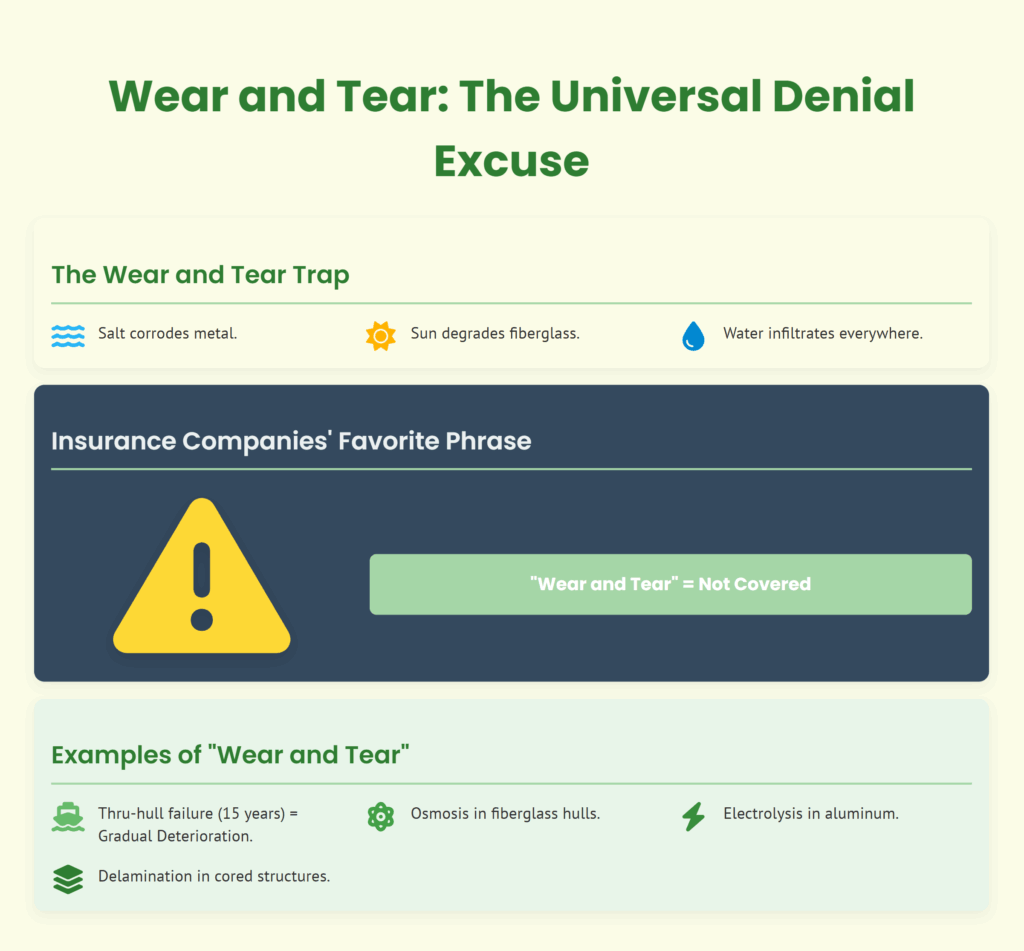

Wear and Tear: The Universal Denial Excuse

Everything on boats wears out. Salt corrodes metal. Sun degrades fiberglass. Water infiltrates everywhere. Insurance companies call it all “wear and tear.” Not covered.

Your thru-hull fitting fails after 15 years. Boat sinks. Insurance says “gradual deterioration.” Claim denied. The sudden failure doesn’t matter. The gradual weakening preceding it justifies denial.

Osmosis in fiberglass hulls. Electrolysis in aluminum. Delamination in cored structures. All classified as wear and tear. All excluded from coverage. All discovered during claims.

Legal Aftermath of Denied Claims

Denied claims trigger cascading legal problems. You still owe the marina for salvage. Environmental cleanup becomes your responsibility. Damaged property owners sue directly.

Without insurance coverage, personal assets become targets. Home equity, retirement accounts, future wages—all subject to maritime liens and judgments. Bankruptcy provides limited protection. Maritime law allows creditors to pursue assets indefinitely.

The Salvage Obligation

Your boat sinks. Law requires removal. Insurance won’t pay. Salvage companies demand $50,000-$200,000 upfront. No payment? Criminal charges possible.

Environmental agencies issue daily fines. $500-$5,000 per day until removal. Fines accumulate during appeals. Interest compounds. A $50,000 salvage becomes $200,000 within months.

Arbitration Clauses Trap Policyholders

Most marine policies mandate binding arbitration. No lawsuits allowed. No jury trials. No public proceedings. Just closed-door arbitration favoring insurers.

Arbitrators often work repeatedly for insurance companies. Obvious bias exists. Policyholders can’t challenge arbitrator selection. Appeals rarely succeed. The system favors insurers by design.

Arbitration costs $15,000-$50,000. Insurance companies have lawyers on retainer. Policyholders pay hourly rates. The financial imbalance ensures most accept denied claims rather than fight.

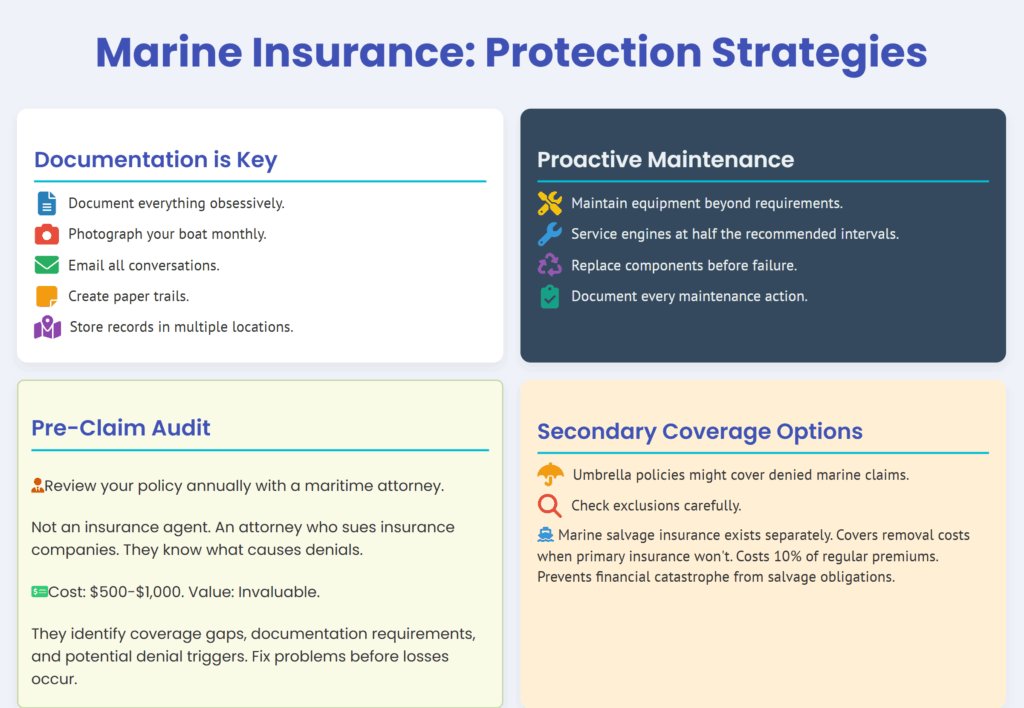

What Actually Works: Protection Strategies

Document everything obsessively. Photograph your boat monthly. Email all conversations. Create paper trails. Store records in multiple locations.

Maintain equipment beyond requirements. Service engines at half the recommended intervals. Replace components before failure. Document every maintenance action.

The Pre-Claim Audit

Review your policy annually with a maritime attorney. Not an insurance agent. An attorney who sues insurance companies. They know what causes denials.

Cost: $500-$1,000. Value: Invaluable. They identify coverage gaps, documentation requirements, and potential denial triggers. Fix problems before losses occur.

Secondary Coverage Options

Umbrella policies might cover denied marine claims. Check exclusions carefully. Some provide coverage when primary marine insurance denies claims.

Marine salvage insurance exists separately. Covers removal costs when primary insurance won’t. Costs 10% of regular premiums. Prevents financial catastrophe from salvage obligations.

Conclusion

Marine insurance claims face 30% denial rates due to mechanical breakdown exclusions, documentation failures, territory violations, and wear-and-tear classifications. Understanding these denial triggers before losses occur prevents financial devastation.

Review your policy exclusions immediately. Document all maintenance meticulously. Photograph vessel conditions monthly. Verify coverage territories precisely. Maintain equipment beyond minimum requirements.

Consider secondary coverage for salvage obligations. Conduct annual policy audits with maritime attorneys. Create comprehensive documentation systems. Your financial survival depends on preventing denial, not fighting it afterward.