This post may contain affiliate links, which means I may receive a commission for purchases made through the links. I will only recommend products that I have personally used! Learn more on my Disclosure page!

Ever stared at a rising sun glinting across the sea’s surface, feeling that unmistakable rush of freedom only a boat can bring? Owning a boat is both enchanting and electrifying—like capturing a slice of boundless horizon for yourself. Yet, a single hidden reef or an unexpected gust of wind can quickly remind us that adventure comes with risk. Accidents happen, storms brew, and unforeseen issues sometimes lurk beneath the calmest waters.

For new boaters, these realities highlight why boat insurance is so critical. While the idea of yet another insurance policy might feel like an unwelcome add-on to your hobby, it is in fact a cornerstone of responsible boat ownership. Much like a life vest can save you during a sudden capsize, boat insurance can rescue you from catastrophic expenses and legal nightmares if mishaps arise.

In this in-depth guide, you’ll discover how boat insurance works, what it covers, and why it’s a must-have for anyone taking to the waves. We’ll venture through essential policy terms, examine factors that affect premium costs, and explore strategies that can soften that monthly or yearly expense. By the end, you’ll understand how to tailor a policy that suits both your boating style and your bank account. Ready to dive in?

Understanding Boat Insurance Basics

What Is Boat Insurance?

On a fundamental level, boat insurance is a contractual agreement between you and an insurer, specifying that the insurer will shoulder certain financial burdens if your boat is damaged, stolen, or deemed responsible for injuring someone else or damaging their property. You, in turn, pay regular premiums to keep the coverage active.

But boat insurance isn’t merely a cut-and-paste copy of auto insurance. It’s specialized to address the realities of maritime life, ranging from groundings near rocky shores to docking mishaps in busy marinas. Different kinds of boat insurance policies cater to specific vessel types—such as jet skis, sailboats, and large powerboats—and can be customized based on features like your engine size, navigation range, and storage setup.

Why Boat Insurance Is Essential for New Boaters

Sailing for the first time can feel like stepping into another world. There’s an undeniable thrill, but it’s also a realm brimming with unique challenges. For instance, if you’re unaccustomed to swiftly changing weather conditions or how to navigate narrow channels, mistakes can happen faster than you’d think.

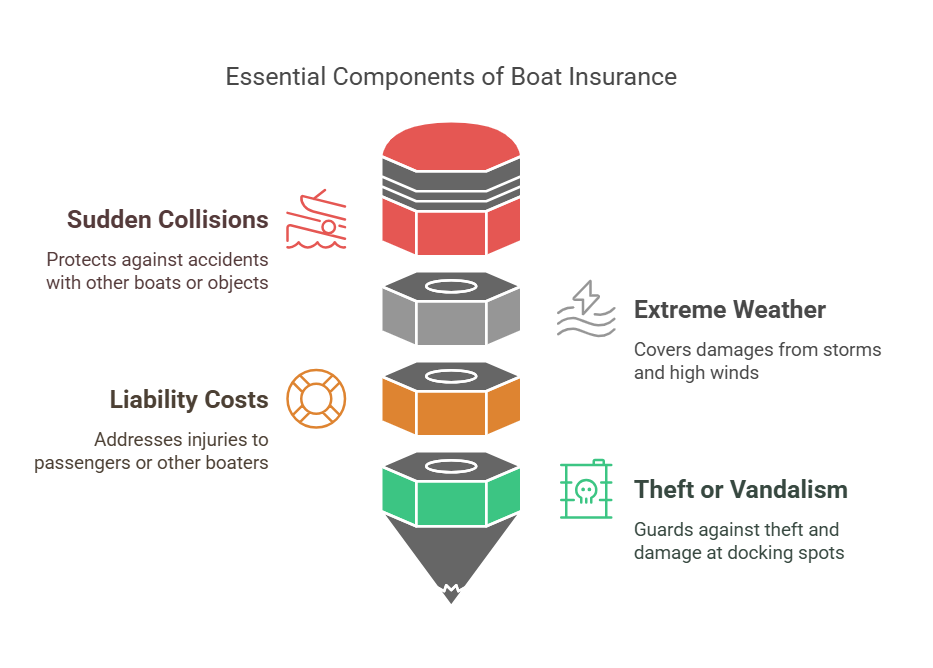

Boat insurance offers peace of mind by protecting you financially from:

- Sudden Collisions: Accidents with other boats or hitting submerged objects.

- Extreme Weather: High winds, storms, or even hurricanes in certain regions.

- Liability Costs: Injuries to passengers or other boaters.

- Theft or Vandalism: Not all docking spots have tight security.

Many marinas also insist on proof of insurance before they allow you to keep a vessel in their facilities. Certain states might have legal requirements that mirror or surpass what marinas expect. Ultimately, having solid coverage isn’t just a line on your expense sheet—it’s a cornerstone of safe, responsible boating.

Types of Boat Coverage

Boat coverage is as diverse as the waters you choose to navigate. Insurers frequently bundle various coverage options into packages, or let you pick à la carte. Below is a snapshot of frequently encountered coverage types:

| Coverage Type | Scope of Protection |

| Hull Coverage | Physical damage to the boat’s structure (hull) and attached equipment. |

| Liability Coverage | Costs related to bodily injury or property damage you cause to others. |

| Medical Payments | Funds medical expenses for you and your passengers after an accident, regardless of fault. |

| Uninsured/Underinsured | Protects you if another boater who is at fault has insufficient or no insurance. |

| Towing & Assistance | Covers rescue services, towing costs, and certain breakdown-related expenses. |

| Personal Property Coverage | Offers reimbursement for personal items onboard, such as electronics or fishing gear. |

| Fishing Equipment | Adds special coverage limits for rods, reels, and specialized tackle if lost or damaged under covered events. |

These coverage areas are foundational. Some people opt for extras like mechanical breakdown endorsements or special coverage for pricey onboard tech. The important thing is to align your coverage with your specific needs and usage patterns.

Key Insurance Terms Every Boater Must Know

Hull Insurance

As the backbone of most boat insurance policies, Hull Insurance focuses on protecting the physical parts of your watercraft. This can include the engine, the hull itself, and any permanently attached fixtures like navigational gear. If a sudden collision with a floating log cracks your hull, this coverage can handle repair or replacement costs.

- Heads-Up: Always check if your hull insurance covers accidents while your boat is on a trailer, as some policies only apply when the boat is afloat or stored in a marina.

Protection and Indemnity (P&I)

In maritime-speak, Protection and Indemnity (P&I) is what many landlubbers would compare to liability insurance. It covers legal obligations if your boat damages someone else’s property or causes injuries to other parties. Additionally, P&I often comes into play if your boat leaks fuel or pollutants into the water, leading to environmental liability.

- Why It Matters: Lawsuits in the boating world can spiral upward quickly, especially if there are injuries or environmental damages involved. P&I coverage serves as a financial shield.

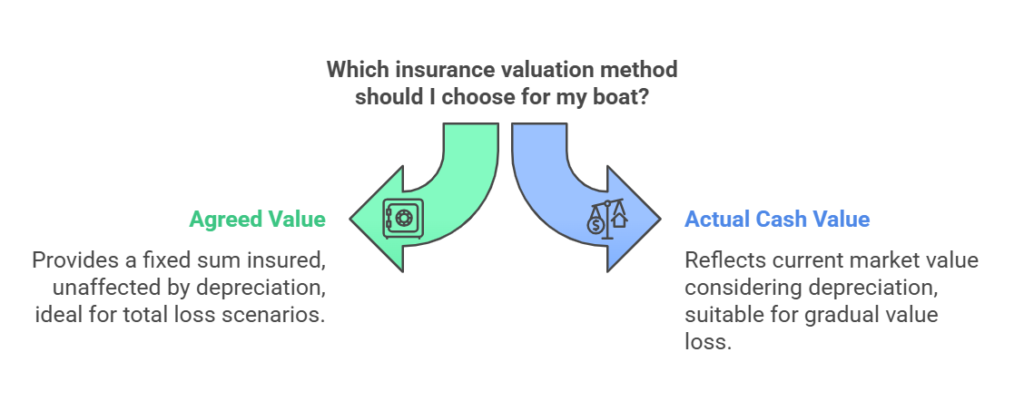

Agreed Value vs. Actual Cash Value

One of the most crucial nuances in boat insurance is determining how the insurer calculates your boat’s worth. Two key methods exist:

- Agreed Value: You and the insurer lock in a specific value for your vessel at the start of the policy. In a total loss scenario (like sinking or complete destruction), you’re paid this agreed-upon sum, without depreciation playing a role.

- Actual Cash Value (ACV): Over time, your boat’s value depreciates. If you suffer a major loss, the insurer compensates you based on the boat’s current market value rather than the original purchase price.

Choosing between these two typically boils down to your budget and whether the boat is brand new, older, or holds special historical or custom value.

Total Loss Coverage

Total loss refers to a situation where repairing your boat after a major accident or disaster isn’t feasible, often due to excessive damage or exorbitant repair costs. Total Loss Coverage ensures you receive a payout that aligns with your policy’s value structure (Agreed Value or ACV), helping you replace your watercraft without going broke.

Personal Property Coverage

Boat trips can resemble mini-adventures, complete with personal gadgets, fishing supplies, and even expensive marine electronics. Personal Property Coverage helps pay to replace these items if they’re lost or damaged due to covered incidents. However, note that each policy might set its own specific limits. For instance:

- Electronics (GPS, sonar, radios) could be capped at a certain amount.

- Personal Items (clothing, binoculars) might require a separate rider if their value is high.

Liability Protection

Operating a boat often involves fluid and unpredictable conditions. You might dodge a careless boater on a busy Sunday afternoon or accidentally back into someone’s boat while docking. Liability Protection covers these real-world missteps, handling legal fees, medical costs, and repair bills if you’re held responsible for the damages.

Medical Payments Coverage

If a passenger slips on deck and sustains an injury during a sudden turn, Medical Payments Coverage steps in. It can cover hospital stays, doctor visits, and other necessary medical treatments, regardless of who caused the accident. This coverage can be a financial lifesaver if an unexpected mishap sends someone to the emergency room.

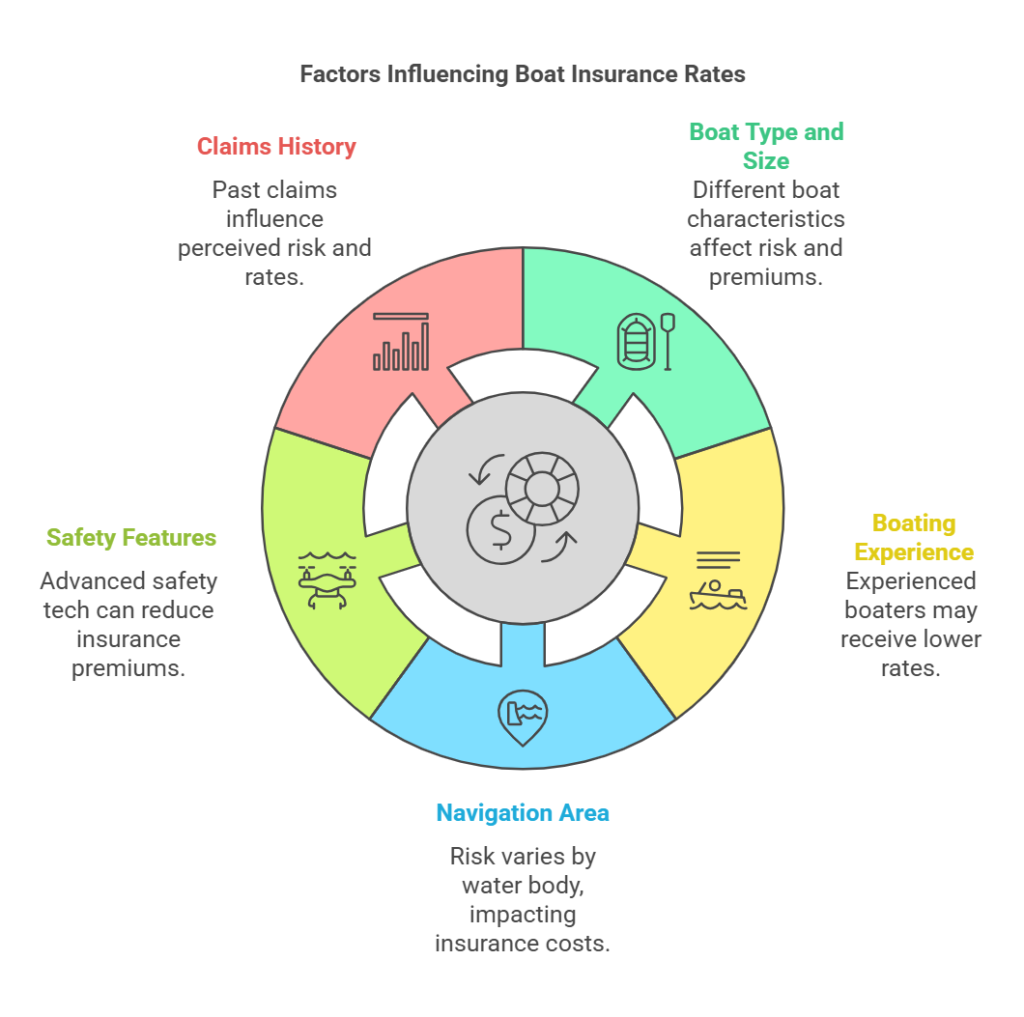

Factors Affecting Boat Insurance Rates

Insurance rates aren’t pulled from thin air; they reflect numerous risk factors and historical data. Understanding these criteria can empower you to reduce premiums where possible.

Boat Type and Size

Boats come in all shapes, speeds, and sizes. Insurers naturally assess how your boat’s characteristics influence the likelihood of accidents:

- High-Performance Speedboats: Their capability for rapid velocity raises the probability of severe collisions. Expect higher premiums.

- Sailboats: Generally slower and deemed less risky by insurers, resulting in somewhat friendlier rates.

Boating Experience

If you’re a seasoned boater who’s taken multiple safety courses and clocked countless hours on the water, you’ll usually get better rates. New boaters, or those with a shaky driving record on land, might face elevated premiums until they establish a track record of responsible behavior.

Navigation Area

Where you plan to navigate significantly affects how insurers view your risk profile:

- Hurricane-Prone Regions: Storm threats can spike premiums.

- Calmer Lakes and Rivers: These bodies of water often pose fewer hazards, leading to lower potential rates.

Safety Features

Installing cutting-edge safety technology can earn you discounts. Features such as:

- Automatic Fire Suppression Systems

- GPS Tracking and Anti-Theft Alarms

- Marine Radios and EPIRBs (Emergency Position Indicating Radio Beacons)

emphasize proactive risk management, which insurers tend to reward.

Claims History

A track record riddled with past claims suggests higher risk. Consequently, insurers will likely quote higher premiums. If you have minimal or no claims, you appear more trustworthy, and your rates typically stay manageable.

Choosing the Right Boat Insurance Policy

Assessing Your Insurance Needs

Boats vary wildly: some are modest pontoons gently cruising a local lake, while others are behemoth yachts battling offshore swells. Ask yourself:

- Usage Frequency: Do you sail daily, seasonally, or just a few times a year?

- Primary Activities: Do you fish casually, indulge in water sports, or host parties onboard?

- Geographical Scope: Inland waters or open ocean? Certain high-risk areas might require specialized coverage.

Your answers shape the coverage details you’ll need. A part-time lake boater might not require the same depth of coverage as someone circumnavigating coastal territories prone to sudden squalls.

Comparing Insurance Providers

Insurers differ in everything from policy language to the ease of filing claims. Don’t hesitate to collect multiple quotes. Compare:

- Premium Costs: The cheapest option isn’t always the best if coverage is lacking.

- Coverage Scope: Look at deductibles, policy caps, and any special endorsements offered.

- Customer Service: Aim for a provider known for quick, hassle-free claim settlements.

Reading the Fine Print

Legal clauses and exclusions can make the difference between a happy resolution and a rejected claim. Dig deeply into:

- Geographical Limitations: Some policies only cover specific regions.

- Excluded Perils: Wear and tear, mold infestations, or mechanical failures may be off-limits.

- Deductible Types: Are there separate deductibles for hurricane damage vs. collision?

Negotiating Your Policy

You might be able to haggle for better terms or rates. Insurers sometimes offer discounts for:

- Multiple Policies (boat + home + auto)

- Boating Safety Certificates

- Long-Standing Customers

- Security and Safety Equipment

A short, friendly conversation with an insurance agent can reveal opportunities for lower premiums.

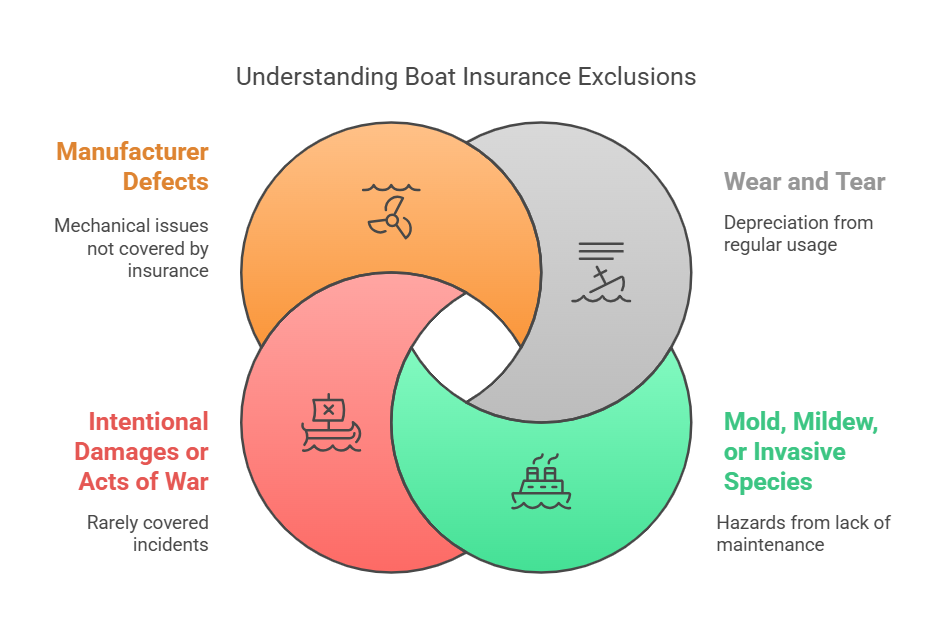

Common Boat Insurance Exclusions

What Typical Policies Don’t Cover

Standard boat insurance is robust but not all-encompassing. Typical exclusions often include:

- Wear and Tear: General aging or depreciation from regular usage.

- Mold, Mildew, or Invasive Species: Preventative maintenance is crucial to avoid these hazards.

- Intentional Damages or Acts of War: Rare but expressly excluded.

- Manufacturer Defects: Mechanical breakdown due to design flaws might require a warranty claim rather than insurance.

Optional Add-Ons and Endorsements

To fill coverage gaps, many insurers offer extra endorsements. A few popular ones are:

- Hurricane Haul-Out Coverage: Covers the expense of removing your boat from harm’s way when an official hurricane watch or warning is issued.

- Mechanical Breakdown Coverage: Addresses certain engine or machinery failures beyond standard wear.

- Fishing Gear Protection: Augments the coverage amount for specialized angling equipment.

Claims Process Explained

Steps to File a Boat Insurance Claim

Picture this: you’re coasting at a gentle speed, but a submerged branch gouges your hull. Now you need to file a claim. Here’s how:

- Notify the Insurer Promptly: Call your provider as soon as possible.

- Document Everything: Capture photos, take notes about water conditions, gather witness information if available.

- Obtain Repair Quotes: Some companies require multiple quotes or send out an adjuster.

- Secure Police Reports (If Applicable): In cases involving theft, vandalism, or injuries, an official report may be necessary.

Documentation Requirements

Being organized can speed up claim processing. Keep:

- Incident or Accident Reports

- Receipts and Maintenance Logs

- Purchase Invoices (for expensive gear or electronics)

- Detailed Photos from various angles

Navigating the Claims Settlement

Once your claim is under review, the insurer may propose repair or replacement options. If it’s a total loss, you may receive a lump sum. Clarify any misunderstandings about deductibles or partial reimbursements to avoid last-minute surprises.

Cost-Saving Tips for Boat Insurance

Discounts and Reductions

Many insurers reward conscientious boaters with price breaks. Be on the lookout for:

- Safe Boater Courses: Certificates from accredited programs such as the U.S. Coast Guard Auxiliary or the American Boating Association often translate into immediate discounts.

- Policy Bundles: Insuring your boat, home, and car under one provider can significantly reduce your overall premium.

- No-Claims Bonus: If you’ve stayed claims-free for a certain duration, you might see your rate drop.

Risk Mitigation Strategies

Show insurers you’re a low-risk client by:

- Regular Maintenance: Keep up with engine inspections, hull cleaning, and mechanical tune-ups.

- Upgraded Security: Invest in robust locks, tracking systems, and anti-theft measures.

- Safety Drills: Practice emergency procedures for fire, collisions, or sudden flooding.

These proactive moves often yield both short-term savings and long-term peace of mind.

Bundling Insurance Policies

Here’s a quick breakdown of potential savings when bundling various insurance types together. Keep in mind, actual percentages vary by provider, so view these numbers as rough estimates:

| Bundle Type | Possible Discount Range |

| Boat + Home | 5% – 20% |

| Boat + Auto | 5% – 15% |

| Boat + Home + Auto (Triple Bundle) | 10% – 25% |

| Boat + Specialty Vehicles (e.g., Motorcycle) | 5% – 10% |

The more you combine, the greater the cumulative discount may become—so long as the coverage matches your real needs.

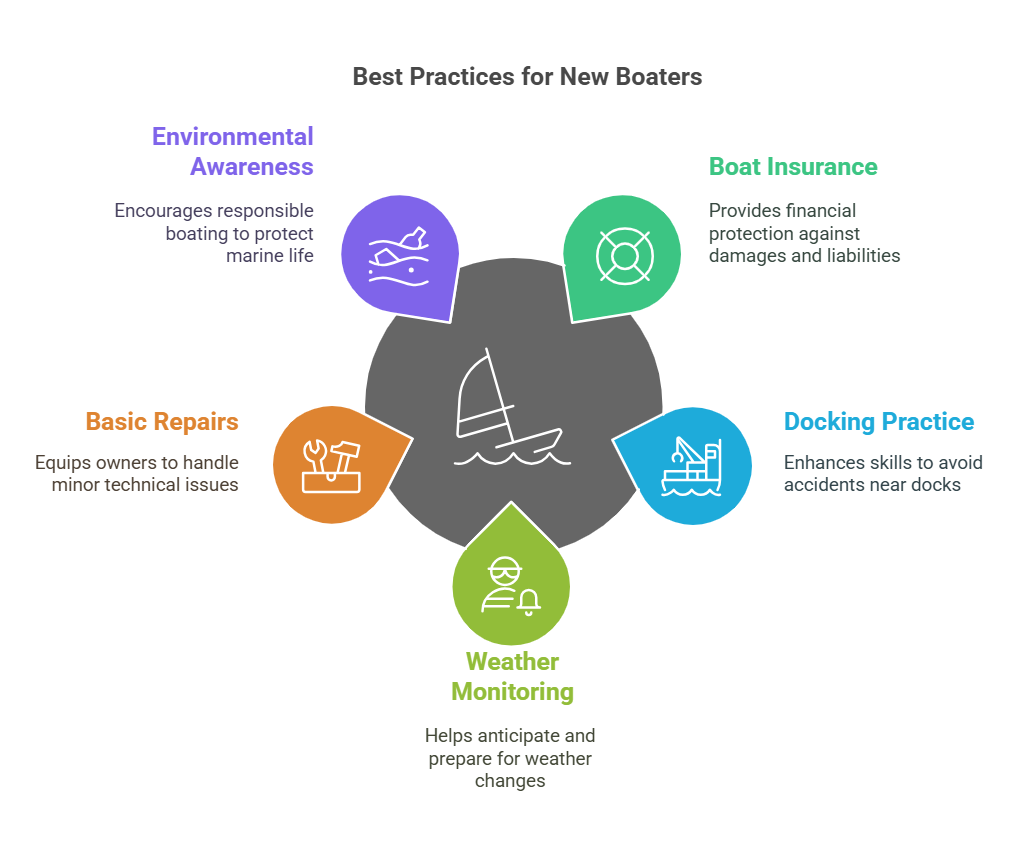

Extra Tips for New Boaters

While boat insurance sits at the heart of financial protection, first-time boat owners should consider other best practices to ensure smooth sailing.

- Practice Docking: Most accidents happen close to docks or in marinas. Having solid docking skills saves time, embarrassment, and money.

- Monitor the Forecast: Weather can shift in an instant. Check reports before each outing and learn to interpret cloud changes and wind shifts on the water.

- Learn Basic Repairs: A small patch kit or set of essential tools can prevent a minor leak from turning into a huge problem.

- Stay Environmentally Conscious: Fuel spills, improper waste disposal, and anchoring in protected reefs can lead to hefty fines. Respecting the environment also keeps your reputation clean in the boating community.

Conclusion

For many, owning a boat is like owning a passport to adventure. You can skim over rolling waves, explore hidden coves, and watch coastal sunsets that flicker with orange brilliance. However, each of these privileges comes with an element of unpredictability—one ill-judged turn or violent storm can spawn serious troubles and towering expenses. That’s where a robust boat insurance policy swoops in, functioning like a supportive safety net when the unthinkable occurs.

Whether you’re brand new to the water or picking up boating again after years away, the right insurance approach is vital. Look beyond just the price tag and focus on what a policy truly covers. Delve into the difference between Agreed Value and Actual Cash Value. Understand how liability coverage can shield you from lawsuits and how add-ons like towing assistance can spare you from panicked phone calls when your engine sputters unexpectedly.

Amid the swirl of coverage clauses, deductibles, and possible endorsements, don’t forget the simpler measures you can take to lower costs. Installing advanced security equipment, filing fewer (or no) claims, and bundling policies can trim your premiums. Meanwhile, practical skills—like respectful docking techniques, thorough maintenance, and careful trip planning—can greatly reduce your risk profile.

In the final analysis, boat insurance isn’t just one more expense. It is a strategic investment in safeguarding everything you cherish about boating—your financial stability, your treasured vessel, and your peace of mind while out on the open water. By mastering these key elements, you’ll be set to embark on countless voyages with confidence. May your anchor hold fast, your sails stay steady, and your insurance policy remain your loyal deckhand whenever the waters get rough.