This post may contain affiliate links, which means I may receive a commission for purchases made through the links. I will only recommend products that I have personally used! Learn more on my Disclosure page!

Cheap boat insurance for older boats exists despite myths about antique watercraft being uninsurable. Insurers assess risk differently for vessels over 15 years old. Condition trumps age every time. Picture your 1985 Chris-Craft gliding across Lake Michigan at sunset. What happens if a sudden squall damages her hull? Without protection, repair bills sink dreams faster than a cannonball. This guide reveals specialist providers, coverage tweaks, and hidden discounts for vintage vessels. You’ll discover why Florida’s salt air impacts premiums more than Oregon’s freshwater, how a $500 safety upgrade slashes rates by 20%, and where to find policies under $300 annually.

Why Older Boats Face Higher Premiums: And How to Fight Back

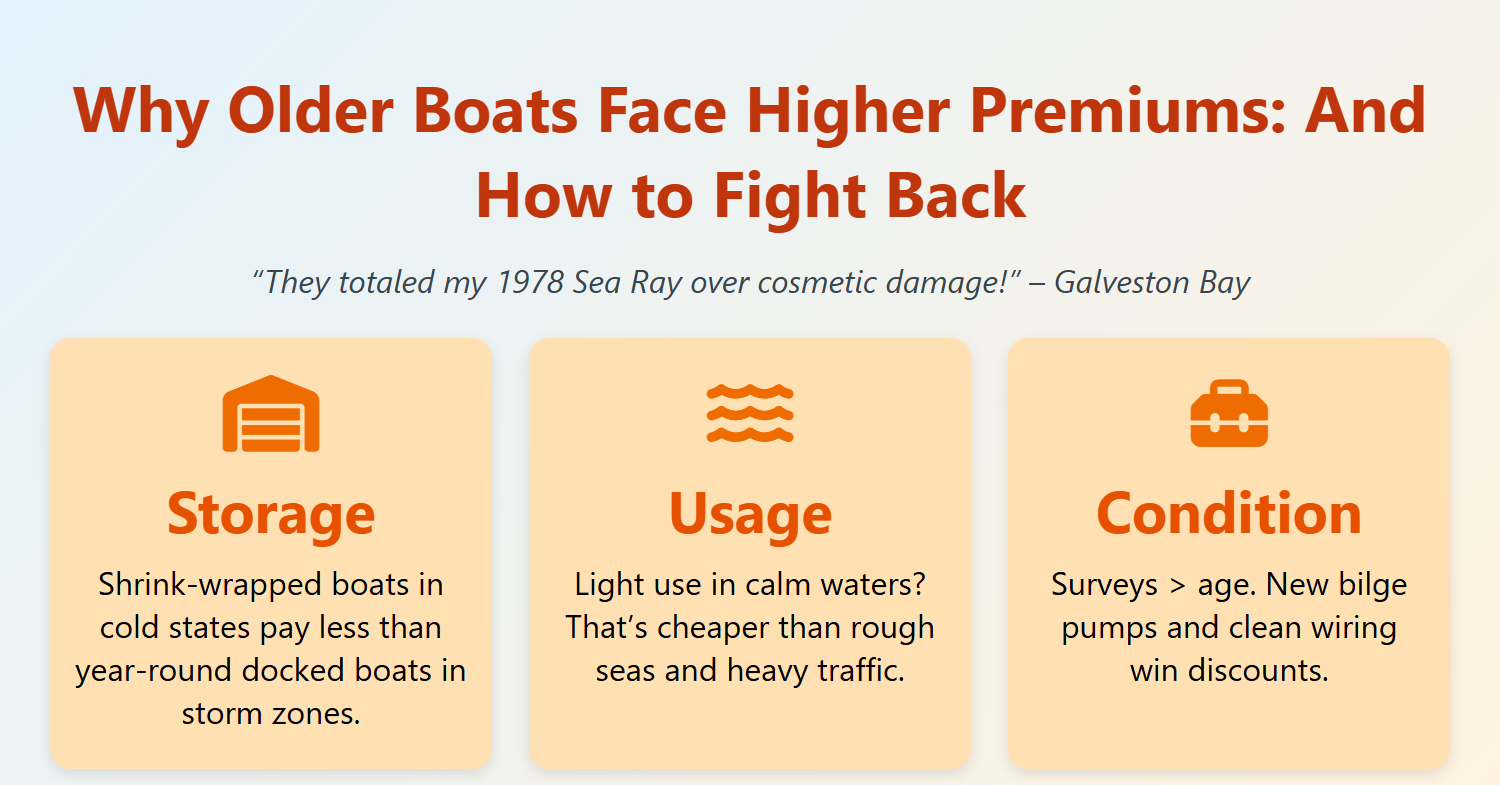

“They totaled my 1978 Sea Ray over cosmetic damage!” laments a boat owner from Galveston Bay. Marine insurers see pre-1990 boats as high-risk: brittle wiring, corroded fuel lines, outdated navigation systems. Yet a Baltimore sailor proved insurers wrong: his meticulously restored 1960s Bertram commands premiums 40% below average. Three factors dominate quotes:

- Storage: A shrink-wrapped boat in Minnesota winters poses less risk than one docked year-round in hurricane-prone Miami.

- Usage: Fifty annual hours on tranquil Vermont lakes beats 200 hours in choppy San Francisco Bay.

- Condition: Survey reports trump manufacturing dates. Fresh bilge pumps and fire extinguishers scream responsibility.

The Hull Truth About Inspections

Insurance surveys aren’t bureaucratic hoops. They’re negotiation tools. When “Salty Dog Salvage” in Seattle upgraded their 1989 trawler’s electrical system ($1,200), the surveyor’s report triggered a 35% premium drop. Always request:

- Moisture readings for fiberglass hulls

- Engine compression tests

- Original equipment documentation

| Upgrade | Avg. Cost | Premium Reduction |

|---|---|---|

| Automatic Bilge Pump | $220 | 12% |

| GPS Tracking | $175 | 18% |

| Marine CO Detectors | $90 | 8% |

The Best Places to Find Cheap Boat Insurance for Older Boats

The internet’s flooded with quote generators. But you’re not just after a number, you’re chasing trust, terms, and flexibility.

1. Niche Marine Insurance Brokers

Small, independent brokers often beat the big names. Why? They know the underwriters who don’t mind older hulls and vintage builds.

Ask local marine supply stores or marinas for recommendations. Brokers in boating towns often have direct contacts at insurers who never advertise.

2. Regional and Local Insurers

State-based insurers like PEMCO (Pacific Northwest) or Farm Bureau (Midwest) sometimes underwrite older vessels when national chains won’t touch them.

Their edge? Understanding local boating conditions. That familiarity breeds flexibility.

3. Classic Boat Programs

Love wooden boats or rare fiberglass classics? Look into programs like Hagerty Marine. Though known for collector cars, they offer agreed-value policies on vessels with a story.

4. Membership-Based Discounts

| Membership | Discount Potential | Perks Offered |

|---|---|---|

| BoatUS | 10%-25% off premiums | Towing, repair discounts |

| USAA | Varies by plan | Excellent for military families |

| American Sailing Association | Up to 15% | Ideal for sailboats |

Memberships often unlock access to insurers you’d never reach as an individual.

Comparison: Budget Boat Insurers for Older Vessels

| Insurer | Specializes in Older Boats | Sample Annual Premium | Coverage Notes |

|---|---|---|---|

| Progressive | Sometimes | $220 – $480 | Great online quotes |

| Hagerty Marine | Yes (classics only) | $200 – $450 | Agreed-value policies |

| Markel | Yes | $180 – $390 | Allows older hulls, broad use |

| BoatUS/GEICO | Yes | $200 – $500 | Discount for members |

| State Farm | No | $250 – $600 | Not ideal for boats >20 years |

Use the above only as a launch point. Premiums vary wildly based on region, boat type, storage, and your boating history.

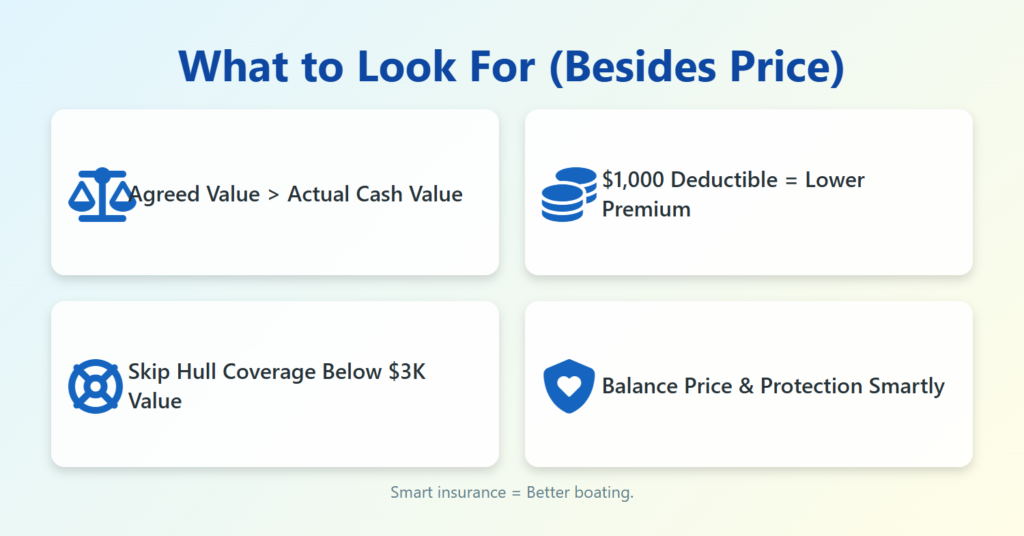

What to Look For (Besides Price)

Getting “cheap” insurance is easy. Getting smart cheap insurance? That takes strategy.

Actual Cash Value vs Agreed Value

Actual Cash Value (ACV) means depreciation hits you hard. That 1988 Bayliner? Might be worth less on paper than your kayak.

Agreed Value locks in a payout upfront. You and the insurer decide what your boat’s worth. That number doesn’t budge, unless you change it.

Deductible Sweet Spot

A $1,000 deductible often lowers your premium significantly. But go too high, and one rogue wave turns into an expensive regret.

Coverage You Can Live Without

Many older boats don’t need hull coverage, especially if their book value is under $3,000. Liability-only plans exist and often cost under $150/year.

The Price vs. Protection Tightrope

Cheapest isn’t always wisest. A Tampa retiree learned this brutally: his cut-rate policy excluded “gradual deterioration”, a $7,000 osmosis repair denial. Top providers balance cost and coverage:

| Provider | Avg. Annual Cost | Older Boat Specialization | Emergency Towing |

|---|---|---|---|

| Progressive | $340 | Agreed-value policies | Included |

| BoatUS | $390 | Classic boat discounts | $100 add-on |

| Foremost | $310 | Hull depreciation waivers | Included |

| Markel | $295 | No survey under 26’ | Included |

Slashing Premiums Like a Pro

Sacramento’s “Old Boat Brigade” shares secrets: bundling with home insurance cuts rates by 22%. Increasing deductibles to $1,500 saves another 15% if you keep $2,000 in an emergency fund. Safety courses (often free via Coast Guard Auxiliary) shave off 12%.

Location, Location, Location

Dock your craft inland? Demand discounts. A Montana lake house owner pays $210 less than his Florida cousin for identical 1980s sailboats. Winter layup months (November-March in Great Lakes regions) qualify for “storage credits.”

Conclusion: Cheap Boat Insurance for Older Boats

Affordable protection for vintage boats thrives at specialized insurers like Markel and Progressive. Prioritize agreed-value policies covering hull blisters and sinking risks: never settle for liability-only. Start today: photograph maintenance records, call three providers from this list, and request “classic boat” quotes. Your 1985 Catalina deserves protection as sturdy as her keel.

Frequently Asked Questions

Can I insure a 40-year-old boat for its appraised value?

Absolutely. “Agreed-value” policies lock in your boat’s worth pre-accident. Submit recent photos and restoration receipts. Progressive specializes in these.

Why did my insurer deny coverage based on age?

Most mass-market insurers automate underwriting. Companies like BoatUS manually review applications; their agents understand vintage marine craftsmanship.

Do wooden hulls cost more to insure?

Typically, yes, by 20-30%. Rot inspections every two years prove seaworthiness. Some insurers waive this for epoxy-sealed hulls.

Are storm damage deductibles higher for older boats?

Not necessarily. Hurricane-prone zones (e.g., Gulf Coast) have percentage deductibles (2-5% of hull value). Inland policies often offer fixed $1,000 deductibles.

Will modifications or restorations help reduce my premium?

Sometimes. Updated electrical systems, anti-theft devices, and new engines can lower risk in the insurer’s eyes. But don’t expect major savings unless the improvements are substantial.

What if my state doesn’t require boat insurance?

You still might need it. Many marinas, lenders, or event organizers demand proof of coverage. And liability lawsuits don’t care what state you live in.