This post may contain affiliate links, which means I may receive a commission for purchases made through the links. I will only recommend products that I have personally used! Learn more on my Disclosure page!

Short answer, yes, you do need boat insurance! Trust me, you do not want to lose your boat and end up paying an arm and leg for lawsuits when the unexpected happens. Picture this: It’s a flawless Saturday afternoon. You’re gliding across the lake, sun warming your face, your favorite playlist humming through the speakers. Out of nowhere, some hotshot in a speedboat veers recklessly across your path. Crunch. Your heart drops as you spin around to see your prized vessel—and theirs—sporting matching dents the size of bowling balls. Now you’re staring down repair bills that could buy a used car, and worse, the other boater’s threatening to sue because their “baby” was a limited-edition model. Sounds like a nightmare? It happens more often than you’d think—and not just to “other people.”So, do you need boat insurance?

Let’s skip the corporate jargon and talk straight. The answer isn’t a quick yes or no. It’s more like, “Let’s grab a coffee and unpack this.” Because whether you’re piloting a kayak or a yacht, the risks—and the what-ifs—are real.

Do You Actually Need Boat Insurance? The Direct Answer

It is a definite yes, you need it. Most states treat boat insurance like sunscreen—technically optional, but you’ll regret skipping it when things get fiery. Only a handful of states force you to get coverage, and even then, the rules are all over the map. Let’s break it down:

- Arkansas: If your boat’s motor growls louder than a Harley (over 50 horsepower), you’ll need liability insurance. Think of it like car insurance for the water—it covers the other guy’s damages if you’re at fault.

- Utah: Got a boat longer than a school bus (65+ feet)? Congrats, you’re in the “mandatory insurance” club. Utah’s not messing around with its floating giants.

- Florida & California: These sunny playgrounds don’t legally require coverage for Joe’s fishing boat or Sally’s weekend cruiser. But—and this is a big but—their crowded waters and hurricane seasons make insurance as practical as a life jacket.

Do You Need Boat Insurance in Florida? Let’s Break It Down

The takeaway? Just because your state says “nah” doesn’t mean your wallet agrees.

Why “Optional” Feels a Lot Like “Essential”

Let’s get real. You insure your phone. Your dog. Maybe even that vintage guitar collection. So why gamble on a boat that costs more than all three combined? Here’s the cold, hard truth:

- Accidents don’t care about state laws: That college kid doing donuts near the dock? They’re not checking your insurance status before sideswiping you.

- Liability lawsuits are expensive: Even a minor injury on your boat—say, a guest slipping on a wet deck—can lead to medical bills higher than your boat’s value.

- Mother Nature’s a wildcard: Storms, hurricanes, rogue waves. Your boat’s a sitting duck without coverage when the sky turns apocalyptic.

Imagine this: You’re hosting friends for a sunset cruise. Someone leans too far for a selfie, tumbles overboard, and breaks a rib. Without liability coverage, you’re not just playing nurse—you’re footing their ER bill and their chiropractor’s “emotional distress” fee.

What Situations Make Boat Insurance Essential?

Not every boat owner faces the same risks. Your need for insurance depends heavily on how, where, and what you boat.

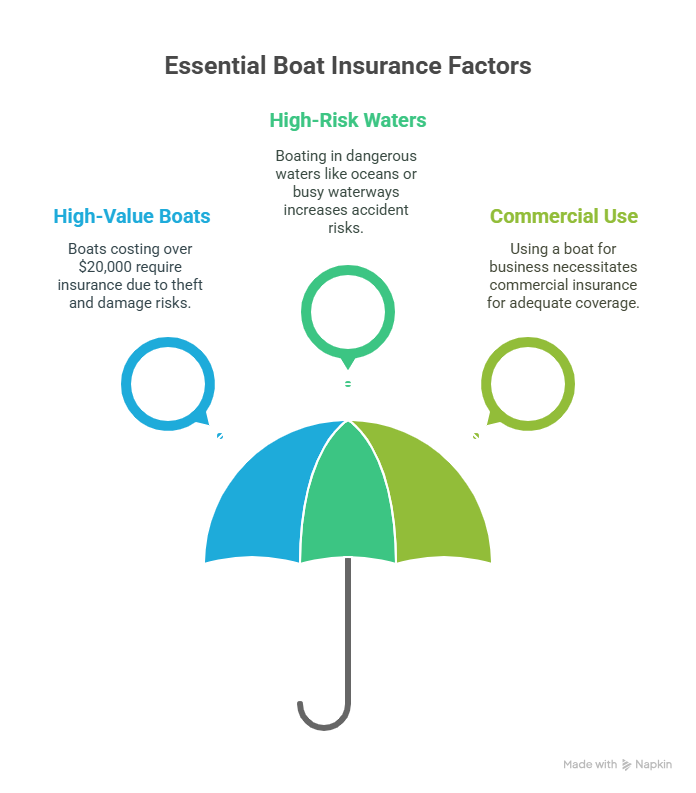

High-Value Boats That Need Protection

If your boat cost more than $20,000, insurance becomes much more important. Losing that kind of investment to theft, fire, or storm damage could seriously impact your finances. A $50,000 boat sitting uninsured is basically a huge gamble with money you probably can’t afford to lose.

Expensive boats also attract thieves. Boat theft claims increase every year, and recovery rates remain disappointingly low. Without insurance, a stolen boat represents a total financial loss.

Boats Used in High-Risk Waters

Some waters are simply more dangerous than others. The Great Lakes, with their sudden storms and heavy commercial traffic, present different risks than a quiet mountain lake. Ocean boating involves weather challenges that freshwater boaters never face.

Busy waterways like those around major cities see more accidents. More boats equals more collision opportunities. If you regularly boat in crowded areas, your accident risk increases substantially.

Commercial vs. Recreational Use Requirements

Using your boat for business changes everything. Charter operations, fishing guides, and boat rental businesses face much stricter insurance requirements. Commercial marine insurance costs more but provides protection that recreational policies don’t cover.

Even occasional commercial use can void a recreational policy. Renting your boat to friends or taking people fishing for money might require commercial coverage.

Do You Need Boat Insurance If You Own Your Boat Outright?

Paying cash for your boat gives you choices that financed buyers don’t have. You can legally operate without insurance in most states. But should you?

Consider what you’d do if your boat sank tomorrow. Could you afford to replace it without touching your retirement savings or emergency fund? If losing the boat would create financial hardship, insurance makes sense regardless of legal requirements.

Some boat owners self-insure by setting aside money equal to their boat’s value. This works if you have serious financial discipline and enough liquid assets to cover a total loss. Most people don’t fall into this category.

Asset protection matters too. If you cause an accident that injures someone seriously, you could face lawsuits that exceed your boat’s value. Liability claims can reach hundreds of thousands of dollars, especially if someone dies or suffers permanent disability.

Do You Need Boat Insurance for Different Types of Watercraft?

The type of boat you own significantly affects your insurance needs.

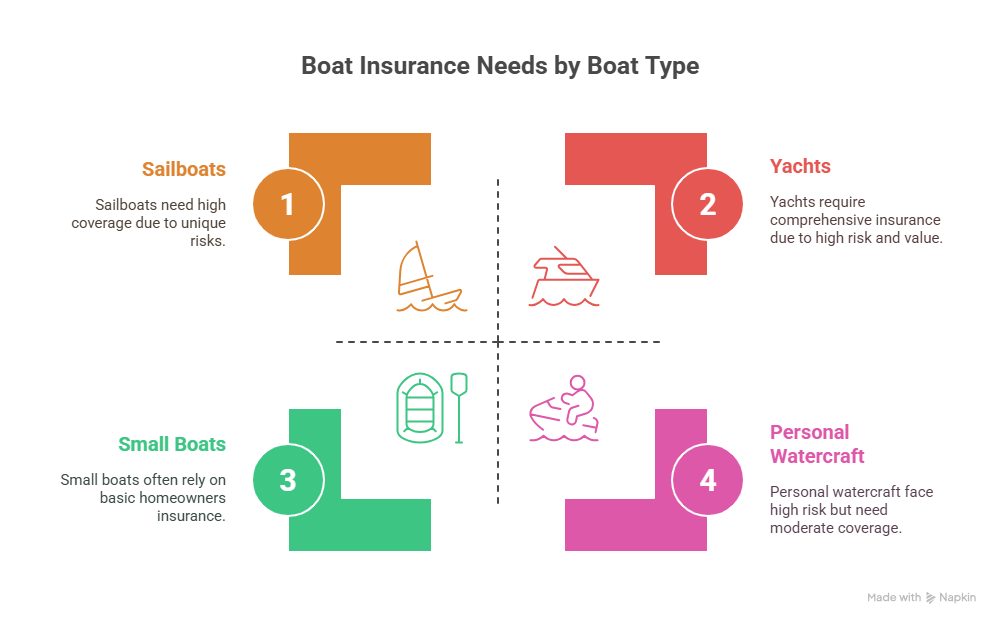

Small Boats and Kayaks

Kayaks, canoes, and small sailboats under 26 feet often fall under homeowners insurance policies. Check your policy carefully though. Coverage typically includes theft and some liability protection, but limits are usually low.

Small fishing boats and pontoon boats present interesting cases. They’re valuable enough to hurt financially if lost, but not expensive enough to require financing. Many owners skip insurance and regret it later.

Sailboats

Sailboats face unique risks that powerboat owners don’t consider. Running aground happens more frequently with sailboats due to their deeper drafts. Mast and rigging damage from storms can cost tens of thousands to repair.

Sailboat racing increases risks substantially. Racing exclusions in standard policies mean you might need special coverage for competitive sailing.

Yachts and Luxury Vessels

Expensive boats demand comprehensive insurance coverage. Yacht policies differ significantly from standard boat insurance. They typically include worldwide coverage, higher liability limits, and protection for expensive electronics and equipment.

Yacht insurance also covers crew wages, charter operations, and salvage costs that basic boat policies exclude.

Personal Watercraft

Jet skis and similar watercraft have higher accident rates than traditional boats. Their speed and maneuverability create unique risks. Many insurance companies charge higher premiums for PWCs because of increased claim frequency.

PWC theft rates are also higher than traditional boats. They’re easier to steal and transport, making comprehensive coverage particularly important.

When Do You Legally Need Boat Insurance?

Legal requirements vary dramatically by location and boat type.

State Requirements

Most states regulate boat insurance differently than auto insurance. While nearly every state requires car insurance, boat insurance mandates are much less common.

States with specific requirements typically focus on larger boats or commercial operations. The thresholds vary, with some states requiring coverage for boats over a certain horsepower and others focusing on vessel length or value.

Even in states without requirements, liability for accidents remains. You’re still responsible for damages you cause, with or without insurance.

Federal and International Waters

The Coast Guard doesn’t require recreational boat insurance, but they do require safety equipment and proper documentation. However, if you cause an accident in federal waters, you face the same liability issues as in state waters.

International cruising presents different challenges. Many countries require proof of insurance before allowing foreign boats in their waters. Without proper coverage, you might find yourself denied entry to foreign ports.

Do You Need Boat Insurance If You’re Financing Your Boat?

Lenders universally require insurance on financed boats. This requirement continues until you pay off the loan completely. The lender will be listed as an additional insured party, and they’ll receive notification if you cancel coverage.

Minimum coverage typically includes comprehensive and collision protection equal to the loan amount. Liability requirements vary by lender but usually start at $100,000 per occurrence.

Gap insurance becomes important for new boats that depreciate quickly. If your boat is totaled early in the loan term, you might owe more than the insurance payout covers. Gap coverage pays this difference.

What Risks Determine If You Need Boat Insurance?

Understanding your specific risks helps determine if insurance makes financial sense.

Collision and Property Damage

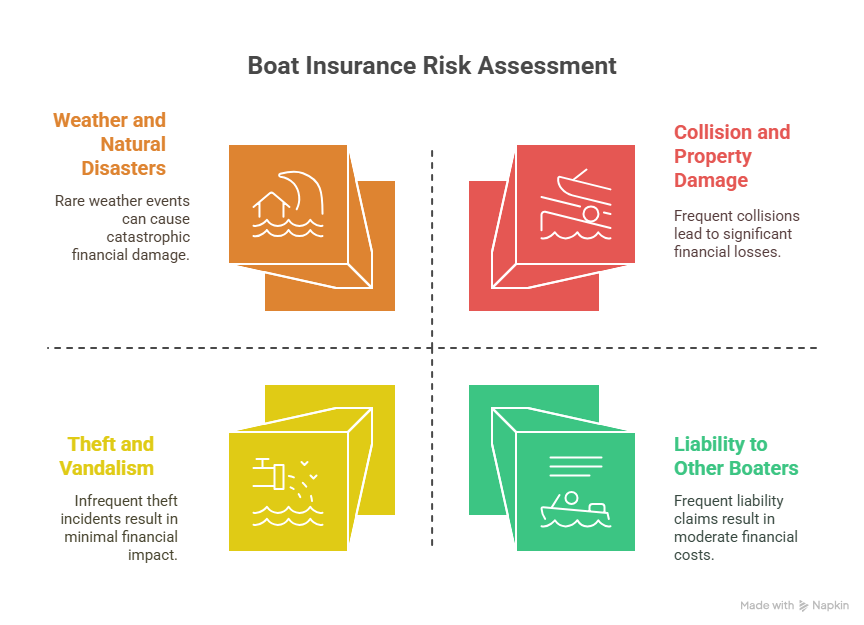

Boat accidents happen more frequently than most people realize. Unlike cars, boats don’t have lanes or traffic signals. Navigation rules exist, but enforcement is limited compared to road traffic.

Property damage from collisions can be expensive. Hitting another boat, dock, or underwater obstacle can cause damage that exceeds your boat’s value. Propeller damage to other boats is particularly costly.

Theft and Vandalism

Boat theft continues rising nationwide. Thieves target boats for their engines, electronics, and resale value. Recovery rates remain low because stolen boats are often taken apart quickly for parts.

Vandalism at marinas or storage facilities affects many boat owners annually. Damage can range from minor scratches to complete destruction.

Weather and Natural Disasters

Storms pose serious threats to boats whether they’re on the water or in storage. Hail damage, wind damage, and flooding can total a boat quickly. Hurricane damage along coastal areas destroys thousands of boats annually.

Even boats in indoor storage face risks from roof collapses, flooding, and fire.

Liability to Other Boaters

Injuring someone while boating creates potentially massive financial liability. Medical bills from boating accidents often reach six figures. Permanent disabilities or deaths can result in million-dollar judgments.

Water sports like skiing and wakeboarding increase liability risks. Towing someone creates additional responsibility for their safety.

Do You Need Boat Insurance Based on Where You Boat?

Location significantly affects your insurance needs and costs.

Freshwater vs. Saltwater

Saltwater boating typically costs more to insure due to higher theft rates, more severe weather, and increased accident frequency. Coastal areas see more boat traffic and more expensive boats, driving up claim costs.

Saltwater also causes more equipment corrosion and maintenance issues, though this doesn’t directly affect insurance decisions.

High-Traffic Waterways

Popular boating areas have more accidents simply because they have more boats. Lakes near major cities, popular vacation destinations, and waterways with heavy commercial traffic all present increased risks.

Busy areas also have more enforcement, which can help prevent some accidents but doesn’t eliminate the risks.

Remote Waters

Boating in isolated areas creates different risks. Emergency response takes longer, making accidents potentially more serious. However, you’re less likely to collide with other boats or cause property damage to expensive facilities.

How Much Boat Insurance Do You Actually Need?

Coverage amounts should reflect your specific situation and risk tolerance.

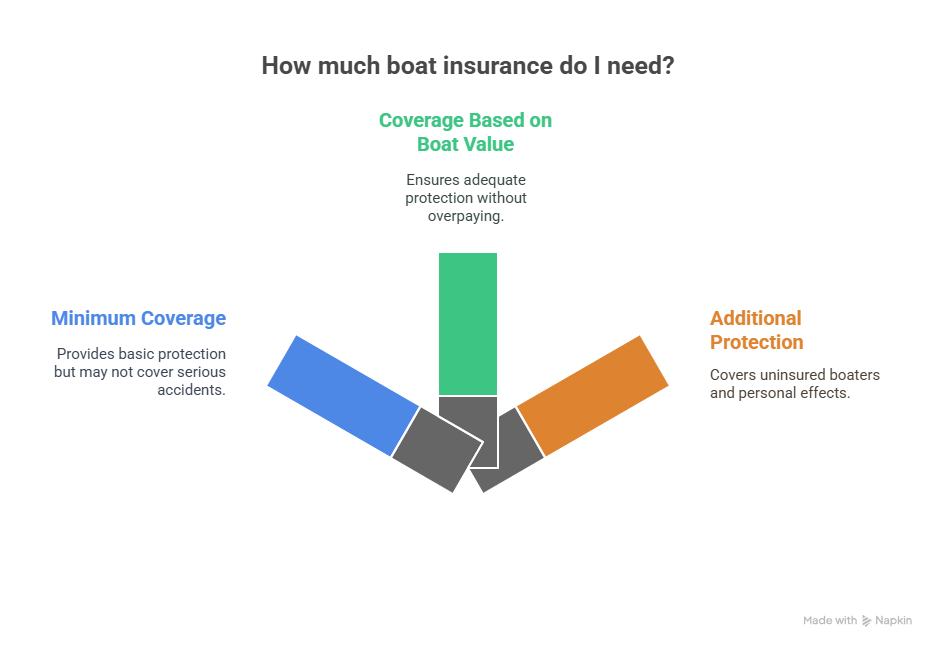

Minimum Coverage

If you decide you need insurance, liability coverage should start at $100,000 per occurrence. This covers basic injury and property damage claims but won’t protect you from serious accidents.

Many experts recommend $300,000 in liability coverage as a more realistic minimum. Serious boating accidents can easily exceed $100,000 in damages.

Coverage Based on Boat Value

Comprehensive and collision coverage should equal your boat’s current market value, not what you paid for it. Boats depreciate, and over-insuring wastes money while under-insuring leaves you exposed.

Consider replacement cost coverage for newer boats. This pays to replace your boat with a similar new model rather than paying depreciated actual cash value.

Additional Protection You Might Need

Uninsured boater coverage protects you when someone without insurance damages your boat or injures you. This coverage is becoming more important as insurance costs rise and some boat owners choose to go without coverage.

Personal effects coverage protects gear you keep on your boat. Fishing equipment, electronics, and safety gear can add up to thousands of dollars in value.

Do You Need Boat Insurance If You Rarely Use Your Boat?

Infrequent use doesn’t eliminate all risks. Boats in storage still face theft, vandalism, and weather damage. However, you might qualify for laid-up coverage that costs less than full-use policies.

Laid-up coverage typically excludes liability and collision coverage while maintaining comprehensive protection. This works well for boats stored for months at a time.

Seasonal boaters often switch between full coverage during boating season and laid-up coverage during winter storage. This strategy can save money while maintaining necessary protection.

Financial Consequences: Why You Might Need Boat Insurance

The financial impact of going without insurance can be severe and long-lasting.

Repair and Replacement Costs

Modern boats contain expensive electronics, engines, and equipment. A minor accident can result in repair bills that exceed $10,000. Major damage or total loss can cost $50,000 or more.

Parts for boats often cost more than similar automotive parts. Marine electronics and specialized equipment carry premium prices that add up quickly during repairs.

Liability Lawsuit Protection

Serious boating accidents can result in lawsuits that last for years and cost hundreds of thousands of dollars. Even if you win the lawsuit, legal defense costs can reach $50,000 or more.

A judgment against you doesn’t disappear if you can’t pay it. Wage garnishment, asset seizure, and bankruptcy might follow a large liability judgment.

Emergency Services

Coast Guard rescues are free, but commercial towing and salvage services are not. Towing a large boat can cost several hundred dollars. Salvage operations for sunken or grounded boats often cost thousands.

These costs hit immediately when you need help, and you can’t delay payment while you figure out financing.

Signs You Definitely Need Boat Insurance

Certain situations make boat insurance essential rather than optional.

If your boat represents a significant portion of your net worth, insurance protects against devastating financial loss. Most financial advisors recommend insuring any asset worth more than 5% of your total assets.

Frequent boaters face higher risks simply due to increased exposure. If you’re on the water more than 20 days per year, your accident risk increases substantially.

Operating in crowded waters or participating in water sports increases both collision and liability risks. These activities make insurance much more important.

Business use of any kind requires commercial coverage. Even occasional charter work or fishing guide services create liability exposures that recreational policies don’t cover.

Making Your Decision: Do You Need Boat Insurance?

Deciding whether you need boat insurance requires honest assessment of your situation, risks, and financial capacity.

Start by determining if insurance is legally required for your boat and location. Factor in lender requirements if you’re financing the purchase. Consider marina requirements if you plan to dock regularly.

Evaluate your financial ability to absorb a total loss. If losing your boat would significantly impact your financial security, insurance makes sense regardless of legal requirements.

Assess your liability exposure based on how and where you boat. Higher-risk activities and locations justify insurance even for owners who could afford to replace their boats.

Consider your risk tolerance. Some people sleep better knowing they’re covered, while others prefer to self-insure and invest the premium money elsewhere.

The decision ultimately comes down to balancing the cost of coverage against the potential financial consequences of going without it. For most boat owners, insurance provides peace of mind that’s worth the annual premium cost. The question isn’t really whether you can afford boat insurance, but whether you can afford to be without it when something goes wrong.

Frequently Asked Questions About Boat Insurance

Q: How much experience do you need for boat insurance?

Insurance companies won’t grill you about your boating resume when offering basic coverage—they’re more concerned with your wallet than your sailing trophies. But here’s the twist: Your time on the water directly shapes what you pay. A rookie skipper and a salty sea dog might get the same policy, but their premiums? Night and day.

Think of it like car insurance for teenagers. New boaters often get slapped with a “newbie tax” for their first few years. Why? Stats don’t lie—inexperience leads to fender-benders (or in this case, hull-scrapes). But there’s hope: Take a safety course from groups like the Coast Guard Auxiliary, and some insurers will knock 10% off your rate. It’s like getting a gold star for adulting.

But here’s where it gets spicy. Want to insure a speedboat that goes 0-to-60 faster than your golf cart? Or a yacht longer than your house? Insurers suddenly turn into helicopter parents. They’ll demand proof you’ve handled similar beasts before. Some flat-out refuse to cover first-timers with overpowered toys. It’s like needing a pilot’s license to fly a fighter jet—no shortcuts.

Age plays games here too. Young boaters pay more (no shocker), but retirees picking up boating at 65? They’re not off the hook either. Insurers have spreadsheets showing late-starters have their own unique oopsie patterns—like misjudging docking speeds or forgetting tides exist.

The silver lining? Time heals all premiums. Stick to the rules, keep your record cleaner than a freshly swabbed deck, and those rates will drop faster than an anchor. Three years of no claims? You’re basically boating royalty to insurers.

Q: Do you need insurance on a boat trailer?

This question’s a sneaky little troublemaker, isn’t it? “Does my insurance cover the trailer?!” Cue the confused head-scratching. The truth? It’s all about the fine print and where your trailer’s parked. Let’s untangle this mess.

Your car insurance might have your back—but only when the trailer’s hitched to your ride. Think of it like a seatbelt that only works while you’re driving. Most auto policies throw in basic trailer coverage (for trailers lighter than your cousin’s lifted pickup, around 2,000 pounds). But the second you unhook that trailer at the marina or your driveway? Poof—coverage vanishes like sunscreen at a beach party.

Now, let’s talk fancy trailers. That sleek aluminum rig you dropped $5K on to haul your prized bass boat? Or the custom-built beast for your vintage wooden sailboat? Those aren’t “just trailers”—they’re investments. Insuring them separately isn’t paranoid; it’s smart. Thieves aren’t just after boats. Trailers are the low-hanging fruit of the waterfront—easy to swipe, easy to chop for parts, and way harder to track than a stolen vessel.

Here’s a plot twist: Some boat insurance policies quietly include trailer coverage, but it’s often skimpy—like 10% of your boat’s value. If your trailer’s worth more than a used Jet Ski, that’s not gonna cut it. Dig into your policy like you’re searching for loose change in the couch. Missing coverage? Time to call your agent and ask, “What’s the deal with my trailer, Karen?”

Q: Does boat insurance cover you in all states?

Most boat insurance policies provide coverage throughout the United States and Canada. However, there are some important exceptions and limitations to understand.

Your policy’s navigation limits define where you’re covered. Basic policies might restrict coverage to inland waters or specific coastal areas. If you plan to boat in different regions, make sure your policy covers those areas.

Some policies exclude coverage in certain high-risk areas. Hurricane-prone coastal regions sometimes require special coverage or higher deductibles during storm season. The Bahamas and other international waters might need additional coverage.

Moving to a different state can affect your coverage and premiums. Insurance rates vary significantly by location due to different risks, regulations, and claim costs. You’ll need to update your policy when you relocate permanently.

Q: Can you get boat insurance with a bad driving record?

Your driving record definitely affects boat insurance rates and availability. Insurance companies figure that people who have car accidents are more likely to have boat accidents too.

DUI convictions hit particularly hard. A DUI, even if it happened in a car, will increase your boat insurance premiums substantially. Some companies won’t write policies for people with recent DUI convictions.

Multiple moving violations or at-fault accidents make you a higher-risk customer. You’ll pay more for coverage, and some insurers might decline to cover you entirely.

However, bad driving records don’t automatically disqualify you from boat insurance. Many companies specialize in higher-risk customers. You’ll pay more, but coverage is usually available.

Time helps heal bad records. Most insurance companies focus on the past three to five years when evaluating risk. Clean driving for several years can gradually reduce your boat insurance premiums.

Q: Do you need boat insurance for boats under 16 feet?

Smaller boats create an interesting insurance dilemma. They’re often valuable enough to hurt financially if lost, but not expensive enough to require financing that would mandate insurance.

Many homeowners insurance policies provide some coverage for small boats, typically under 26 feet and with engines under 50 horsepower. This coverage usually includes theft and some liability protection, but limits are often quite low.

The problem with relying on homeowners coverage is that it’s not designed for regular boat use. If you use your small boat frequently, you might exceed the policy’s intended coverage scope.

Small boat accidents can still result in serious liability claims. A 14-foot fishing boat can cause just as much injury as a larger vessel if handled improperly. Liability exposure doesn’t decrease just because your boat is smaller.

Consider separate boat insurance if your small boat is worth more than $10,000 or if you use it regularly in busy waters. The peace of mind often justifies the relatively low cost of coverage.

Q: What happens if you get caught boating without required insurance?

Penalties for boating without required insurance vary significantly by state and situation.

In states that mandate boat insurance, penalties typically include fines, possible boat impoundment, and license suspension. Arkansas, for example, can fine uninsured boaters and prevent them from registering their boats until they provide proof of insurance.

Even in states without insurance requirements, operating without coverage can have serious consequences if you cause an accident. You’re personally liable for all damages, injuries, and legal costs.

Coast Guard officers can ask for proof of insurance during safety inspections, though they can’t cite you for not having coverage in most situations. However, if you cause an accident during the inspection, the lack of insurance becomes a much bigger problem.

Marina operators often require proof of insurance before allowing you to dock. Getting caught without coverage might mean being asked to leave immediately.

The biggest risk isn’t the fine, it’s the financial exposure. One serious accident without insurance can result in decades of financial hardship.

Q: Does boat insurance cover fishing equipment and personal belongings?

Standard boat insurance policies typically include some coverage for personal property, but limits are usually quite low, often just $1,000 to $5,000 total.

Serious anglers carry thousands of dollars worth of rods, reels, tackle, and electronics. A single fish finder can cost $2,000 or more. High-end fishing setups easily exceed basic policy limits.

You can usually purchase additional personal property coverage for an extra premium. This coverage protects fishing gear, tools, safety equipment, and other personal items you keep on your boat.

Some policies distinguish between permanently attached equipment and portable items. Electronics that are wired into your boat might have better coverage than portable GPS units or tackle boxes.

Expensive items like high-end fishing reels or electronics might need to be specifically listed on your policy to receive full coverage. This is called scheduling items, and it usually requires appraisals for very valuable equipment.

Consider keeping an inventory of your boat’s contents with photos and receipts. This documentation helps tremendously if you need to file a claim for stolen or damaged personal property.