This post may contain affiliate links, which means I may receive a commission for purchases made through the links. I will only recommend products that I have personally used! Learn more on my Disclosure page!

Slashing your boat insurance premium doesn’t require a mysterious formula—just a blend of smart choices, safety measures, and strategic timing. By raising deductibles, bundling with other policies, completing boater‑safety courses, installing anti‑theft gear, and more, you can typically cut costs by 15–30% without compromising coverage. Below, you’ll find ten richly detailed, research‑backed methods—each one explained in depth—to help you navigate the insurance waters and dock at the best possible rate. Here are the 10 Tips for Lowering Your Boat Insurance Premium.

1. Raise Your Deductible to Reduce Your Premium

Opting for a higher deductible means you shoulder more of the initial cost if you file a claim—but in exchange, insurers reward you with lower annual premiums. According to industry data, every $500 you increase your deductible can trim your premium by roughly 5–10%, Insurance Advisors Of St. Louis. Striking the right balance requires assessing your personal emergency fund: if you can comfortably cover a larger out‑of‑pocket expense, boosting your deductible is one of the most straightforward levers to pull for immediate savings.

2. Bundle Your Boat Policy with Other Insurance

Insurance companies prize multi‑policy customers. Bundling your boat insurance with your auto, home, or renters policy can unlock discounts of 10–20% on each line of coverage. This “multiline” approach not only simplifies billing and renewals but also creates negotiating power: when renewal time comes, you can leverage your bundled relationship for additional savings or perks, such as waived fees or enhanced roadside assistance.

3. Take an Accredited Boating Safety Course

Demonstrating seamanship through a state‑approved or recognized boating safety course reduces insurer risk. Carriers like Progressive and GEICO offer discounts up to 15% for certificate holders, while specialized marine underwriters—BoatUS and Travelers—extend credits for completion of U.S. Power Squadron or U.S. Coast Guard Auxiliary programs: Travelers Insurance, BoatUS Foundation. Beyond the premium relief, these courses sharpen navigation skills, emergency response, and weather‑reading abilities—benefits that extend well beyond your wallet.

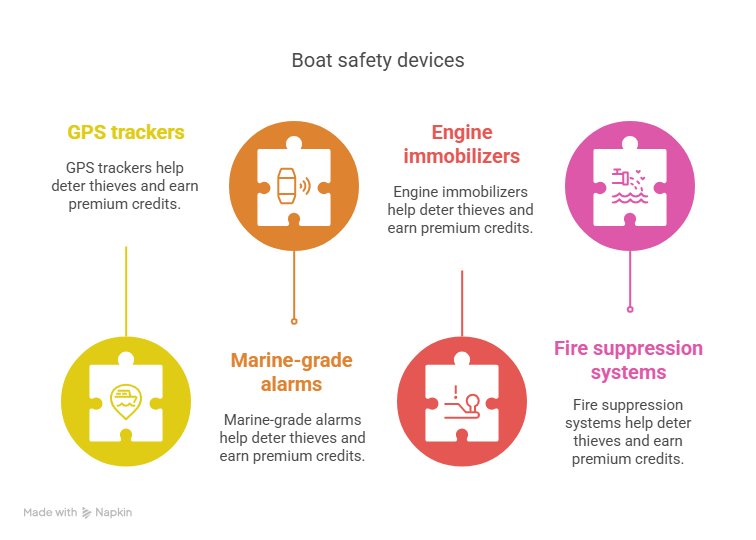

4. Install Safety and Anti‑Theft Devices

Bolstering your boat with GPS trackers, marine‑grade alarms, engine immobilizers, and fire suppression systems not only deters thieves but also earns you premium credits. Insurers such as Ansay & Associates and Progressive typically offer 5–12% off when you equip your vessel with approved anti‑theft or safety gear. Document installation with photographs and equipment receipts to ensure your discount is applied—and keep maintenance logs to show the devices remain operational year‑round.

5. Maintain a Spotless Boating Record

Just as a clean driving record lowers auto insurance, a claim‑ and violation‑free boating history can lead to meaningful savings. Progressive notes discounts of 5–10% for boaters with no at‑fault claims or comprehensive losses over 12 months, while specialty brokers recommend log‑keeping to validate safe operation and regular maintenance. Logging each trip, recording weather conditions, and performing routine inspections help substantiate your low‑risk profile at renewal time.

6. Opt for Seasonal “Lay‑Up” Coverage

If your boating season is limited—say, four to six months annually—consider “lay‑up” or “winterization” coverage during the off‑season. This pared‑down policy suspends liability and collision coverages while maintaining protection against theft, fire, and natural disasters. Lay‑up credits can slice premiums by 30–50% compared to year‑round plans (Sound Choice Insurance). Ensure your vessel meets lay‑up criteria (e.g., winterized engine, ashore storage) to qualify for the full discount.

7. Choose Secure Mooring and Storage

Where you dock or store your boat directly influences risk assessments. Facilities with gated access, 24/7 surveillance, and professional staff earn insurers’ trust—and lower rates—compared to private docks or roadside parking (HUB Marine). Enclosed dry‑stack storage can yield the steepest discounts, often 10–15% off standard mooring rates. Before signing a lease, request a certificate of security features from your marina to present to your insurer.

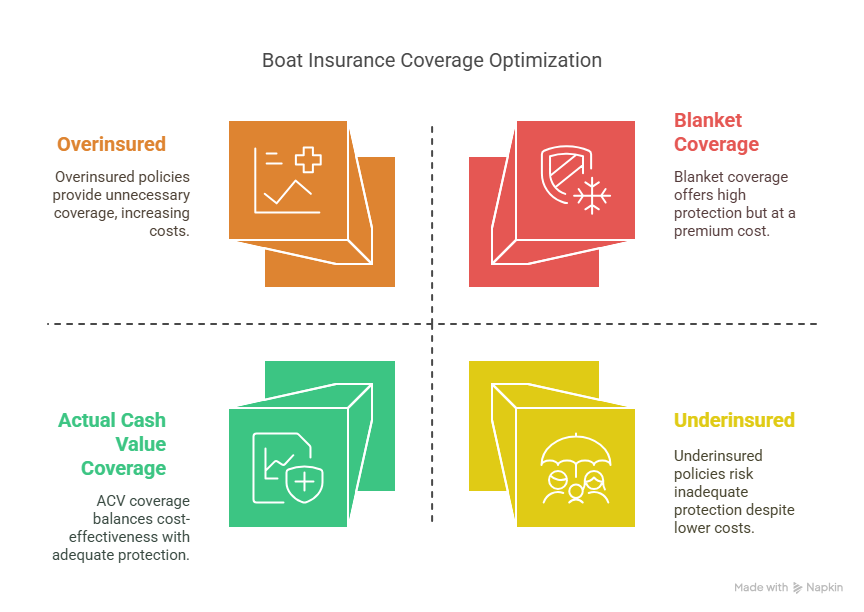

8. Tailor Coverage Limits to Your Vessel’s Value

Blanket coverage may feel safe, but it can also be costly. For older boats with depreciated market values, reducing hull coverage to actual cash value (ACV) rather than replacement cost can trim premiums without exposing you to undue risk (Allstate). Similarly, reassess add‑on options—such as towing, emergency pickup, and personal effects—to ensure you only pay for what you truly need. Regular policy reviews with your agent allow you to align coverage with your boat’s age and condition.

9. Pay Your Premium Annually, Not Monthly

Many insurers tack on fees or interest for installment plans. By paying your full premium upfront, you can avoid these hidden charges—often saving 3–7% of your total cost (The Irish Sun). Budgeting a small monthly “insurance sink fund” can make the lump‑sum payment manageable, and your insurer will reward you with a cleaner bill and potentially enhanced loyalty credits at renewal.

10. Shop Around and Negotiate at Renewal

Boat insurance markets vary widely. Quotes from at least three providers—including mainstream carriers (GEICO, Progressive) and niche marine underwriters (BoatUS, Markel)—help you benchmark rates and coverage options GEICO Nboat. Armed with competing offers, you can negotiate with your current insurer for a match or superior terms. Even a 5% rate reduction achieved through haggling can translate into hundreds of dollars saved.

At‑A‑Glance Comparison of Savings Strategies

| Tip | Typical Savings | Key Providers / Notes |

|---|---|---|

| Higher Deductible | 5–10% per $500 | IASTL, NBOAT |

| Policy Bundling | 10–20% | Progressive, Investopedia Multiline |

| Boater Safety Course | Up to 15% | Progressive, GEICO, BoatUS |

| Anti‑Theft & Safety Devices | 5–12% | Ansay & Associates, Progressive |

| Clean Boating Record | 5–10% | Progressive, SkiSafe |

| Seasonal Lay‑Up Coverage | 30–50% | SoundChoice, Travelers |

| Secure Mooring/Storage | 10–15% | HubMarine, Allstate |

| Adjust Coverage Limits | Varies | Allstate, Travelers FAQs |

| Annual Payment | 3–7% | The Sun |

| Shop & Negotiate | 5–15% | NBOAT, GEICO |

By weaving these ten strategies into your insurance‑renewal playbook, you’ll transform premium negotiations from a guessing game into a precision exercise—freeing up funds for upgrades, maintenance, or that next epic voyage. Safe travels and fair winds!

FAQ: Tips for Lowering Your Boat Insurance Premium

Below are the questions boat owners most frequently search online when looking to reduce their insurance costs—each answer is grounded in industry data and expert guidance.

1. How does raising my deductible reduce my boat insurance premium?

Opting for a higher deductible—the out‑of‑pocket amount you cover before insurance pays—signals to underwriters that you’ll handle smaller losses yourself, reducing their risk. Industry analysis shows that for every $500 increase in deductible, you can save about 5–10% on your premium (https://www.boatus.com). Before choosing, ensure you have sufficient emergency funds to cover that deductible in case of a claim.

2. Can I save by bundling my boat policy with other insurance?

Yes. “Multiline” discounts reward customers who purchase multiple policies from the same carrier. Bundling boat insurance with auto or homeowners insurance typically yields 10–20% off each policy (https://www.boatus.com). Beyond savings, bundling simplifies billing and gives you leverage to negotiate additional perks—such as waived fees—at renewal.

3. What boating safety courses qualify for insurance discounts?

Insurers frequently honor certificates from state‑approved and nationally recognized programs. Discounts up to 15% are common for courses like the U.S. Coast Guard Auxiliary, U.S. Power Squadron, and those approved by the National Association of State Boating Law Administrators (NASBLA) (Travelers Insurance, Bryden and Sullivan). These courses not only lower premiums but also sharpen your navigation, emergency response, and weather‑reading skills.

4. Which safety and anti‑theft devices can lower my premium?

Approved devices include GPS trackers, engine immobilizers, marine‑grade alarms, and automatic fire‑suppression systems. Carriers such as Ansay & Associates and Progressive offer 5–12% credits when you document installation of these items (Independent Insurance Agents, Markel Insurance). Maintain logs and receipts as proof—insurers may audit to confirm ongoing functionality.

5. How important is my boating record in calculating premiums?

Just as auto insurers reward safe drivers, boat insurers discount accident‑ and claim‑free histories. A spotless record for 12–36 months can reduce premiums by 5–10% (https://www.boatus.com, Independent Insurance Agents). Keeping a trip log—detailing dates, routes, and maintenance checks—helps validate your low‑risk profile at renewal.

6. What is lay‑up coverage and how much can I save?

Lay‑up (or seasonal) coverage suspends liability and collision protections while retaining fire, theft, and natural‑disaster coverage when your boat is stored ashore. Premiums for lay‑up periods are typically 30–50% lower than full‑season policies (Sound Choice Insurance, https://www.skisafe.com). To qualify, vessels usually must be winterized and kept in approved storage.

7. Does where I store or moor my boat affect my insurance cost?

Absolutely—storage security directly impacts risk assessments. Storing in a guarded marina or enclosed dry‑stack facility can earn 10–15% discounts compared to private docks or trailer storage (https://www.boatus.com, Boat Ed). Before locking in rates, obtain written confirmation of security features (gates, lighting, surveillance) to show your insurer.

8. Should I adjust coverage limits for older boats?

Yes. If your vessel’s market value has depreciated, reducing hull coverage to actual cash value (ACV) rather than replacement‑cost basis can trim premiums without exposing you to undue risk (TGH Insurance, Power & Motoryacht). Periodically review add‑ons (towing, personal effects) and remove those you no longer need.

9. Is it better to pay my premium annually or monthly?

Paying in full upfront typically avoids installment fees and interest charges, yielding a 3–7% discount on your total premium (Travelers Insurance). If a lump‑sum payment is challenging, set aside small monthly amounts in a dedicated “insurance fund” to capture the annual‑payment savings.

10. How often should I shop around or negotiate my boat insurance?

Boat insurance markets fluctuate. It’s wise to get quotes from at least three providers—including mainstream carriers (GEICO, Progressive) and marine specialists (BoatUS, Markel)—every 12–18 months (The Hull Truth, Allstate). Use competitive offers as leverage to negotiate rate matches or improved coverage with your current insurer.

11. Are there any additional lesser‑known discounts available?

Yes. Some insurers offer credits for:

- Paperless billing or automatic payments

- Memberships in boating clubs or marine associations (Independent Insurance Agents)

- Hybrid/electric boat incentives as part of green‑fleet programs (Travelers Insurance)

12. What other factors can influence my boat insurance premium?

Several variables play a role beyond the basics:

- Boat type and horsepower: Faster, high‑performance vessels cost more to insure (Boat Ed).

- Geographic cruising area: Coverage in hurricane or theft‑prone regions commands higher rates (https://www.boatus.com).

- Owner experience and age: Seasoned, certified captains often secure lower rates.

- Credit score (where permitted): In some states, better credit can reduce premiums (kiplinger.com).

By understanding and proactively managing these elements, you can tailor your policy to achieve the lowest sustainable premium while maintaining the protection you need.