This post may contain affiliate links, which means I may receive a commission for purchases made through the links. I will only recommend products that I have personally used! Learn more on my Disclosure page!

By the year 2025, the world of marine insurance is primed for an extraordinary leap—one that redefines not only how boat owners receive coverage but also how insurers assess risk, process claims, and interact with customers. The term marine insurance digital-first encapsulates a transformation so profound that traditional underwriting and claim settlement processes now appear outdated by comparison.

In a digital-first era, we witness the melding of AI (Artificial Intelligence), blockchain systems, real-time data analytics, and even the emerging promise of quantum computing. At a time when industry insiders predict that each new day ushers in another breakthrough, many are left wondering: What does this new landscape look like? Why is it happening now? And, crucially, how can stakeholders adapt?

This article delves into the forces driving marine insurance digital-first adoption, the technologies shaping its future, and the far-reaching impact it has on policyholders, brokers, and insurers alike. In essence, it’s a roadmap to the new world of digital transformation in marine insurance, complete with tables, bullet points, and thorough explanations that reflect our evolving understanding of the maritime industry.

Why 2025? The Perfect Storm of Innovation and Necessity

Converging Technologies and Rising Consumer Expectations

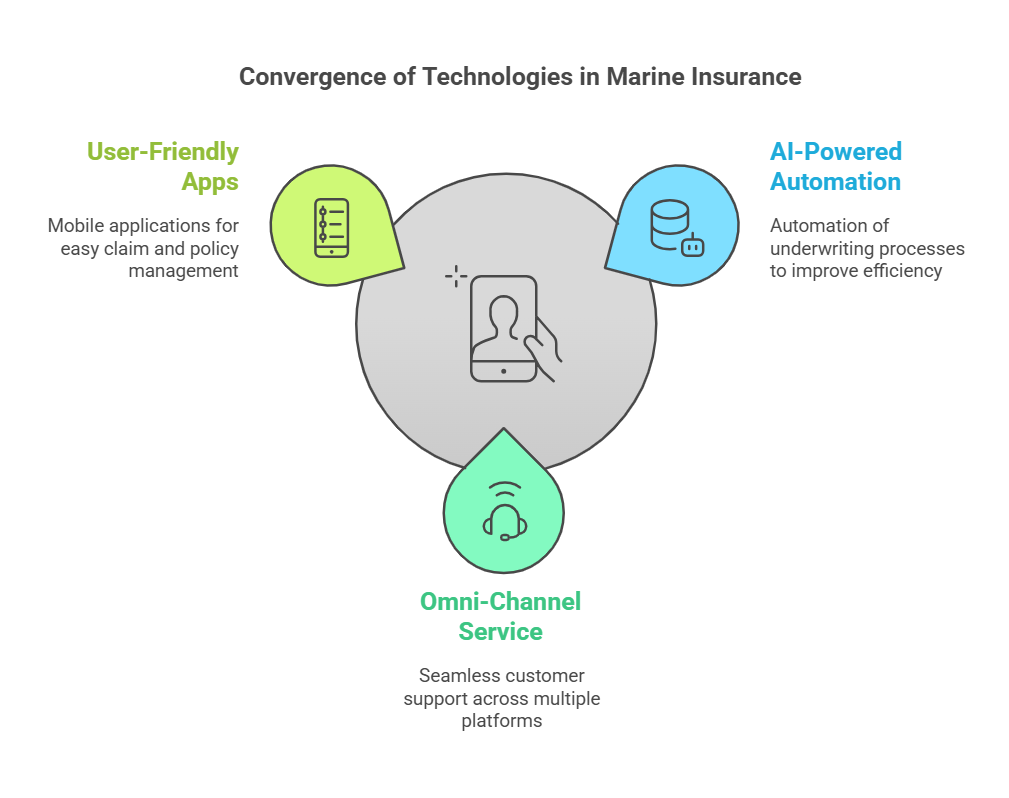

Technological leaps are converging at the exact moment when consumer expectations reach an all-time high. For instance, most people no longer tolerate the idea of waiting days—or, worse, weeks—to receive insurance quotes or claim settlements. Through everyday conveniences like mobile payments and app-driven services, consumers have grown to expect near-instant responses to their queries.

In marine insurance digital-first strategies, this on-demand culture is met head-on by:

- AI-powered automation: Rapid underwriting that no longer relies on extensive manual processes.

- Omni-channel customer service: Seamless transitions between phone, chat, and email support so that no one is left waiting on hold.

- User-friendly mobile applications: Streamlined platforms for filing claims, updating policy details, and even receiving reminders about vessel maintenance.

This consumer-centric evolution has compelled insurers to modernize. Gone are the days when marine insurance was deemed too niche for digital upgrades. Instead, universal demands for speed, transparency, and customer-focused solutions have ignited a sense of urgency across the industry.

The IoT (Internet of Things) Factor

To truly appreciate why 2025 marks a turning point, consider the rise of IoT devices within maritime environments. Previously, sophisticated onboard sensors were reserved for large commercial fleets. Today, even recreational boats often come equipped with GPS tracking, engine health monitors, and weather sensors that transmit data in real time.

| IoT Feature | Benefit |

| GPS Tracking | Enables precision tracking and routing |

| Engine Health Monitors | Alerts owners to mechanical issues early |

| Weather Sensors | Delivers up-to-date climate conditions |

| Hull Integrity Trackers | Detects micro-damage or structural stress |

Such comprehensive data inflow allows underwriters to tailor policies with unprecedented accuracy, resulting in dynamic premiums that can fluctuate based on actual vessel usage and risk exposure. Meanwhile, claims can be validated more effectively because real-time data logs often provide an indisputable record of when, where, and how an incident occurred.

Cyber Threats Meet Cyber Solutions

The digitalization of marine insurance introduces a paradox: the more processes migrate online, the more vulnerable insurers become to cyber attacks. This vulnerability might involve anything from hacking policyholder data to disabling critical underwriting systems. Ironically, the solution to these looming threats can also be found in digital technology.

- Blockchain-based storage safeguards against tampering and ensures records remain verified and unalterable.

- Advanced encryption standards secure sensitive financial and identification data.

- AI-driven security detects suspicious activity in real time, closing system vulnerabilities before a breach occurs.

The interplay between higher cyber risk and robust digital defenses forms yet another catalyst compelling the entire industry to modernize. In this sense, we find insurers locked in a race against both cybercriminals and their own technological inertia. Those who proactively invest in cybersecurity now will be much better positioned to thrive in the new environment.

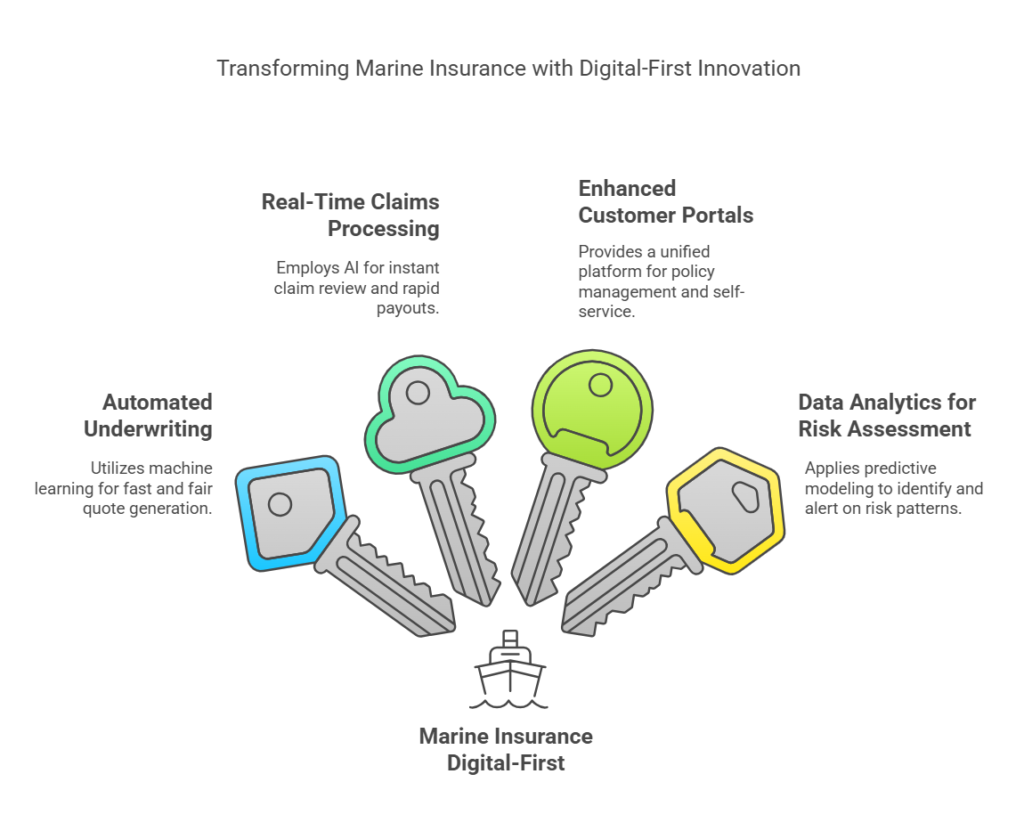

Defining “Marine Insurance Digital-First”

Moving to a digital-first model implies that every facet of marine insurance, from initial quote generation to final claim settlement, revolves around digital channels. Rather than employing technology as an afterthought or an enhancement to existing paper-based processes, a digital-first approach places technology at the core of insurance operations.

Core Components

- Automated Underwriting

- Speed: Machine-learning algorithms can crunch vast volumes of data within seconds, issuing quotes faster than any manual process.

- Fairness: Reduces human bias by relying on data, not gut instinct or outmoded heuristics.

- Real-Time Claims Processing

- Instant Review: Claims are scanned by AI that checks photo or video evidence against historical data.

- Rapid Payouts: Digital wallets or online transfer methods expedite settlement for policyholders.

- Enhanced Customer Portals

- Single Dashboard: Policyholders can file claims, review policy details, and engage in live chats all in one place.

- Self-Service Tools: Allows boat owners to make minor changes to coverage terms, upgrade or downgrade certain features, and view usage statistics at their convenience.

- Data Analytics for Risk Assessment

- Predictive Modeling: Identifies patterns that signal increased likelihood of accidents, theft, or mechanical malfunctions.

- Proactive Alerts: Notifies owners and insurers alike when certain risk thresholds are met.

A Quick Overview in Table Format

| Digital-First Feature | Example | Value Proposition |

| Automated Underwriting | Algorithms that evaluate policy risk in real time | Faster quotes, minimal human error |

| Real-Time Claims Processing | AI reviewing video and photo evidence post-incident | Rapid payouts, reduced administrative overhead |

| Enhanced Customer Portals | Smartphone apps for policy tracking and adjustments | Centralized interface, customer convenience |

| Data Analytics for Risk | Predictive modeling based on usage and IoT sensor data | Personalized rates, proactive warnings |

The Tech Driving the Revolution

1. Artificial Intelligence (AI)

AI’s role in marine insurance digital-first processes cannot be overstated. It’s the “brain” behind many cutting-edge features:

- Chatbots: These can handle routine questions about coverage limits, premium structures, and renewal timelines, freeing up human agents to tackle more nuanced concerns.

- Machine Learning: Through pattern recognition, AI can predict mechanical failures or potential collisions, enabling insurers to refine coverage options or offer preventive maintenance plans.

AI can even transform how insurers view claims. Instead of dealing with a backlog of unresolved cases, an AI system cross-references incident photos with a database of past claims to gauge damage severity. This approach drastically lowers claim-processing times and enhances consistency in payouts.

2. Blockchain

While blockchain has been a buzzword in financial technology for years, its usefulness in marine insurance is increasingly evident:

- Smart Contracts: Self-executing codes that release payments automatically when agreed-upon conditions—like weather conditions that match storm damage—are met.

- Immutable Ledger: A tamper-proof record of all transactions and policy details that significantly reduces fraud.

In a future where ephemeral documents and unverified claims can derail entire operations, blockchain injects an element of trust and certainty into the process.

3. Quantum Computing

Quantum computing is still an emerging technology, but it promises to disrupt the foundations of data analytics. Traditional supercomputers might take years—or even centuries—to analyze the staggeringly large data sets generated by global shipping routes, weather patterns, and IoT sensor readouts. Quantum systems, however, can theoretically run thousands of simulations in parallel, pinpointing risk factors with surgical precision.

- Ultra-Fast Modeling: Quantum computers could make it possible to generate highly customized insurance premiums almost instantly.

- Complex Problem Solving: They can handle cryptographic challenges, further enhancing security measures like encryption and blockchain verification.

Though widespread commercial adoption of quantum computing may still be some years out, the thought of a future where insurers run millions of risk assessments per second underscores just how dramatic this digital-first shift could become.

Benefits for Every Stakeholder

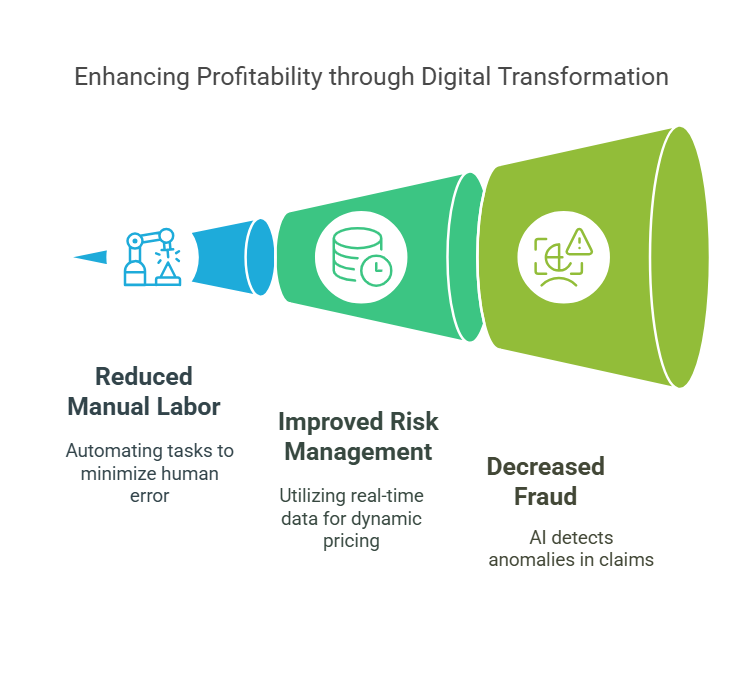

For Insurers: Efficiency and Profitability

When an insurer adopts a marine insurance digital-first model, the shift usually results in better underwriting decisions and lower operational costs. By employing AI for tasks like claims review:

- Reduced Manual Labor: Less reliance on paper-based documentation and human data entry.

- Improved Risk Management: Real-time monitoring of vessels allows for dynamic pricing strategies, ensuring premiums remain competitive.

- Decreased Fraud: AI cross-checks new claims against existing records, flagging anomalies that require further investigation.

This enhanced operational efficiency often translates into higher profit margins. It also empowers insurance companies to invest more in customer-facing tools, fueling a virtuous cycle of improvement and modernization.

For Brokers: A Competitive Edge

Brokers who embrace digital-first strategies position themselves as forward-thinking consultants rather than mere middlemen. Their value proposition intensifies through:

- Faster Quote Generation: Automated systems deliver quotes to prospective clients with minimal delay.

- Unified Client Profiles: Robust data platforms allow brokers to gain holistic views of each client’s coverage, claims history, and ongoing risks.

- Specialized Expertise: By understanding advanced technologies and digital underwriting models, brokers can guide clients through complexities, adding crucial advisory value.

Additionally, brokers who partner with innovative insurance providers are more likely to stand out in a saturated market, attracting a broader client base seeking the fastest and most transparent coverage options.

For Boat Owners: Peace of Mind and Convenience

Boat owners stand to gain the most from a marine insurance digital-first transformation. No longer do they have to cope with convoluted policy documents or labyrinthine claim procedures. Instead:

- Instant Claims: Through dedicated mobile apps, owners can submit pictures of damage, input relevant details, and receive near-immediate feedback.

- Predictive Alerts: AI systems might alert owners when weather patterns suggest an imminent hazard, or when onboard sensors detect mechanical issues that need urgent attention.

- Customizable Policies: Data-driven underwriting allows for flexible coverage that can be expanded or scaled back depending on usage frequency, boat type, and navigational areas.

Moreover, boat owners benefit from the security that blockchain-based solutions offer—ensuring that personal and financial information remains safeguarded. This dual benefit of convenience plus robust security fosters deeper trust in digital marine insurance systems, encouraging more boat owners to come aboard.

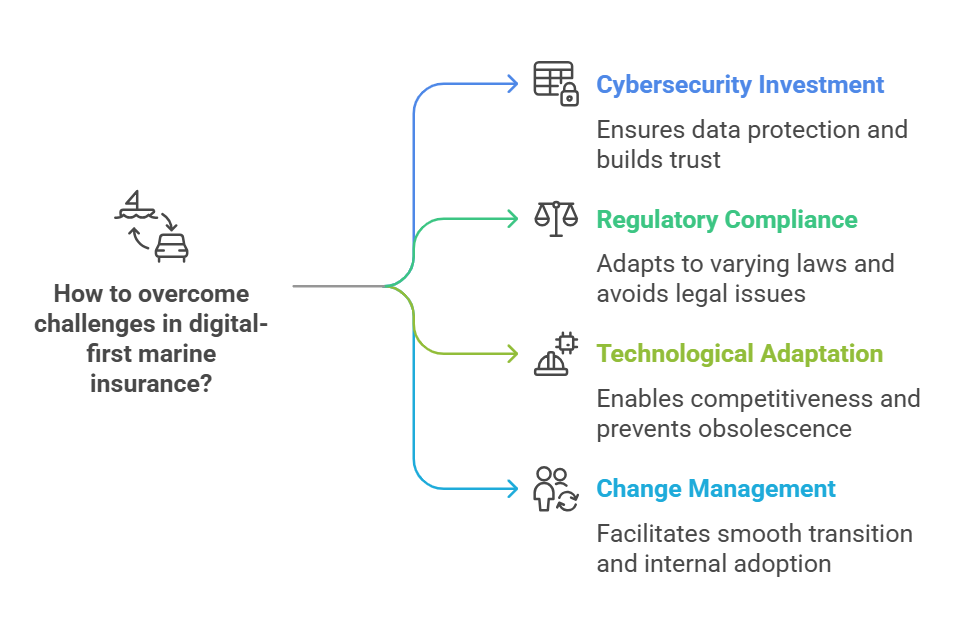

Overcoming Challenges: Turbulent Waters Ahead

Even with all its promises, the path to digital-first marine insurance is not without its obstacles.

- Cybersecurity Risks

As insurers store larger quantities of data online, they must invest in cutting-edge intrusion detection systems and encryption protocols. A single breach can undermine trust, trigger legal repercussions, and incur hefty financial losses. - Regulatory Hurdles

Marine insurance laws vary widely across regions, and regulators often take time to update existing legislation to reflect new technological realities. Insurers must work closely with legal experts and governmental bodies to ensure compliance. - Technological Disparities

Not every insurer or broker has the capital or expertise to make an immediate leap. Smaller firms risk being left behind if they cannot adapt their systems to a digital-first model quickly enough. - Human Resistance to Change

Traditionalists might see digital platforms as complex or impersonal. Investing in employee training and change management programs ensures internal adoption remains as seamless as possible.

Addressing the Cybersecurity Conundrum

An effective strategy to mitigate cyber threats involves multiple layers of defense and thorough employee education. For example:

- Zero-Trust Architecture: No user or device is automatically trusted; continuous verification is required for every request.

- Security Drills: Regular simulations of phishing attacks or ransomware attempts ensure staff members remain vigilant.

- Insurance for Cyber Risks: A meta-layer of insurance coverage that protects insurers themselves from catastrophic cyber events.

By taking these steps, insurers can reassure customers, brokers, and underwriters that sensitive data and funds remain in safe hands.

Peering Into the Future: Beyond 2025

Augmented Reality (AR) and Virtual Reality (VR) may soon evolve from gimmicks to vital tools in marine insurance. Imagine surveyors who no longer need to visit vessels in person to assess damage. Instead, they could use AR to visualize boat structures in real time, overlaying crucial data such as probable weak points, historical maintenance records, and potential cost estimates for repairs.

Ongoing AI and Machine Learning Advancements

AI will continue to refine:

- Risk Prediction Models: Identifying increasingly subtle warning signs, potentially preventing accidents before they happen.

- Personalized Recommendations: Tailoring coverage to match each individual’s usage habits, whether they’re weekend yachtsmen or full-time cruisers exploring remote waters.

- Claims Fraud Detection: Spotting anomalies in supporting documentation or user-submitted images that even experienced human inspectors might miss.

The Rise of Maritime Tech Startups

Where large legacy insurers sometimes struggle with bureaucratic inertia, startups often excel. New entrants into the digital-first marine insurance space—like Roamly, cited for their customer-focused and data-driven approach—are nimble, tech-savvy, and eager to disrupt established models. Many will experiment with novel solutions, potentially partnering with established insurers to offer hybrid packages that blend the best of both worlds.

Case Studies in Marine Insurance Digital-First

Case Study 1: Roamly’s Real-Time Underwriting

Roamly has turned heads with its rapid underwriting model. Utilizing AI algorithms that tap into public maritime databases and real-time weather feeds, Roamly can deliver policy quotes often in under 15 minutes. This speed is particularly beneficial for spontaneous boat buyers who don’t want to wait for coverage to finalize. Early data suggests a significant reduction in fraudulent claims as well, thanks to the robust AI scanning procedures.

Case Study 2: Blockchain-Powered Claims in Asia

In parts of Asia, a consortium of insurance providers teamed up to pilot a blockchain-based claims processing network. After a severe storm season, policyholders found their claims processed in record time—some within hours—because smart contracts automatically validated weather conditions and location data. This streamlined approach not only boosted customer satisfaction but also drastically cut administrative overhead.

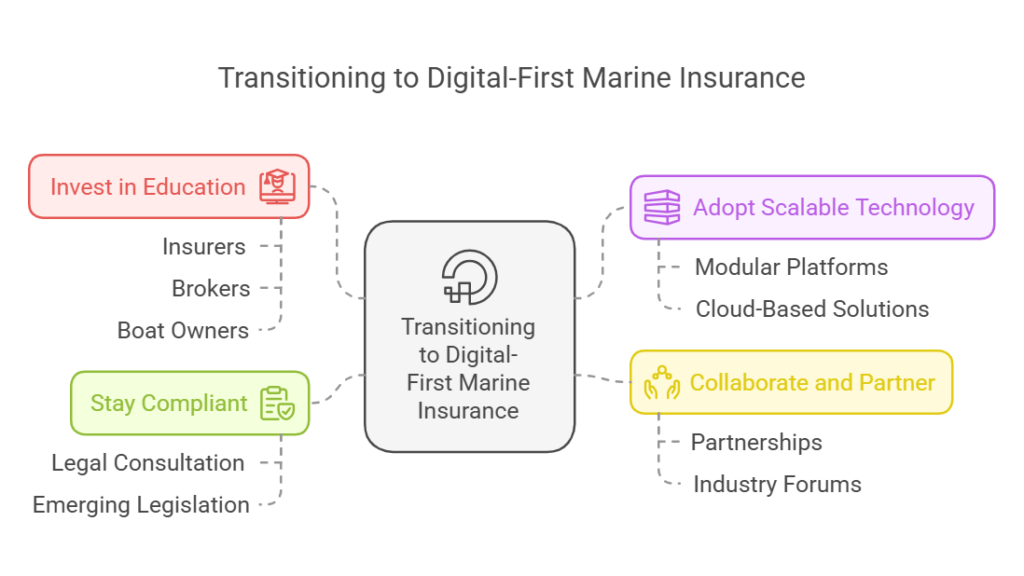

Preparing for the Shift to Marine Insurance Digital-First

Whether you are an insurer, a broker, or a boat owner, here are crucial steps to position yourself for success in this rapidly evolving landscape:

- Invest in Education

- Insurers: Train underwriters, claims adjusters, and support staff in AI tools and cybersecurity best practices.

- Brokers: Learn how to interpret IoT data so you can better advise clients.

- Boat Owners: Familiarize yourself with the basics of digital claims filing and data privacy safeguards.

- Adopt Scalable Technology

- Choose modular platforms that can integrate easily with third-party APIs or emerging technologies like blockchain.

- Smaller firms can opt for cloud-based solutions that reduce the burden of maintaining in-house servers.

- Collaborate and Partner

- Look for partnerships with startups or established tech firms to co-develop solutions.

- Engage in industry-wide forums or associations that promote standards and best practices for digital insurance.

- Stay Compliant

- Consult with legal experts on regional regulations concerning data storage, usage of blockchain, and AI-driven underwriting.

- Keep an eye on emerging legislation around digital ID verification and personal data protection.

Bullet Point Tips for Boat Owners

- Ensure Your Vessel Is IoT-Ready: Add trackers or sensors that might lower your premium by providing real-time risk data.

- Compare Policies: Digital platforms let you quickly compare multiple offers; use them to secure a better rate.

- Ask About Cybersecurity: Confirm that your insurer uses encryption and robust protocols to protect your personal data.

- Look for Bundles: Some insurers offer bundled coverage that combines general liability, hull coverage, and even specialized equipment insurance under one digital dashboard.

Word of Caution: Navigating Regulatory Waters

Despite the clear advantages, governments and regulatory bodies sometimes take a cautious approach to the widespread adoption of emerging technologies, especially in financially and logistically intricate areas like marine insurance. This cautiousness might manifest as:

- Delayed Approval Timelines: New underwriting models or digital claims processes may require extensive review.

- Data Residency Requirements: Regulations that mandate data be stored and processed within the same jurisdiction where a policyholder resides.

- Additional Licensing: Brokers and insurers could be subject to new certifications or compliance mandates specifically tied to digital insurance offerings.

Staying ahead demands vigilant monitoring of regulatory updates and an ability to pivot quickly when new rules come into effect.

Final Thoughts: Embrace the Wave of Change

By the time 2025 arrives, marine insurance digital-first strategies will no longer be experimental or niche. They will be industry standard, reshaping customer expectations and competitive landscapes alike. The interplay of AI, blockchain, quantum computing, and IoT has already begun dismantling outdated processes, replacing them with faster, smarter, and more transparent systems.

For insurers, this transformation paves the way to heightened profitability and operational excellence. For brokers, it ushers in a new era of advisory opportunities, where timely insights can seal deals and nurture long-term client relationships. And for boat owners, it offers the ultimate trifecta: peace of mind, convenience, and cost-effectiveness.

If you’re ready to catch this wave, consider exploring innovative digital insurance providers like Roamly, known for their commitment to digital transformation in marine insurance. As technology evolves, so too must our solutions and expectations. In an environment where speed and transparency often spell the difference between a minor inconvenience and a crisis, embracing digital-first principles is not just smart—it’s absolutely essential for anyone looking to thrive in the modern maritime world.