This post may contain affiliate links, which means I may receive a commission for purchases made through the links. I will only recommend products that I have personally used! Learn more on my Disclosure page!

One moment, you’re a proud boat dealer showcasing sleek new vessels to excited customers, the next, a sudden torrent of rain or a freak surge in the nearby river threatens to turn your entire stock into a half-submerged nightmare. These abrupt, water-driven perils—alongside more ordinary mishaps like slips on a damp pier or engine malfunctions during a demo ride—reveal why regular business boat insurance often isn’t enough in the marine world. When you handle floating assets, “just in case” transforms into a critical necessity. That’s where boat dealer insurance stands front and center.

Yet for many boat dealers, the complexities swirl. How do you differentiate a standard retail policy from a specialized marine coverage plan? Which specific policies guard you against environmental hazards, roving inventory, or that unpredictable lightning bolt that chooses to strike your vessel yard on the busiest day of summer? In this comprehensive guide, you’ll discover the essential coverage types tailored to boat dealerships, ways to trim premium costs, and how to sidestep hidden pitfalls—so you can keep your inventory safe and your peace of mind intact.

Understanding Boat Dealer Insurance Essentials

Life on the water differs drastically from life on land. Boats require docking and hauling, engines require specialized maintenance, and weather events can escalate from mild breezes to raging tempests in the blink of an eye. Traditional commercial insurance typically looks at structures and standard business liability, but it seldom stretches to protect expensive floating merchandise or the myriad risks tied to operating near (or on) the water.

Why the Distinction Matters

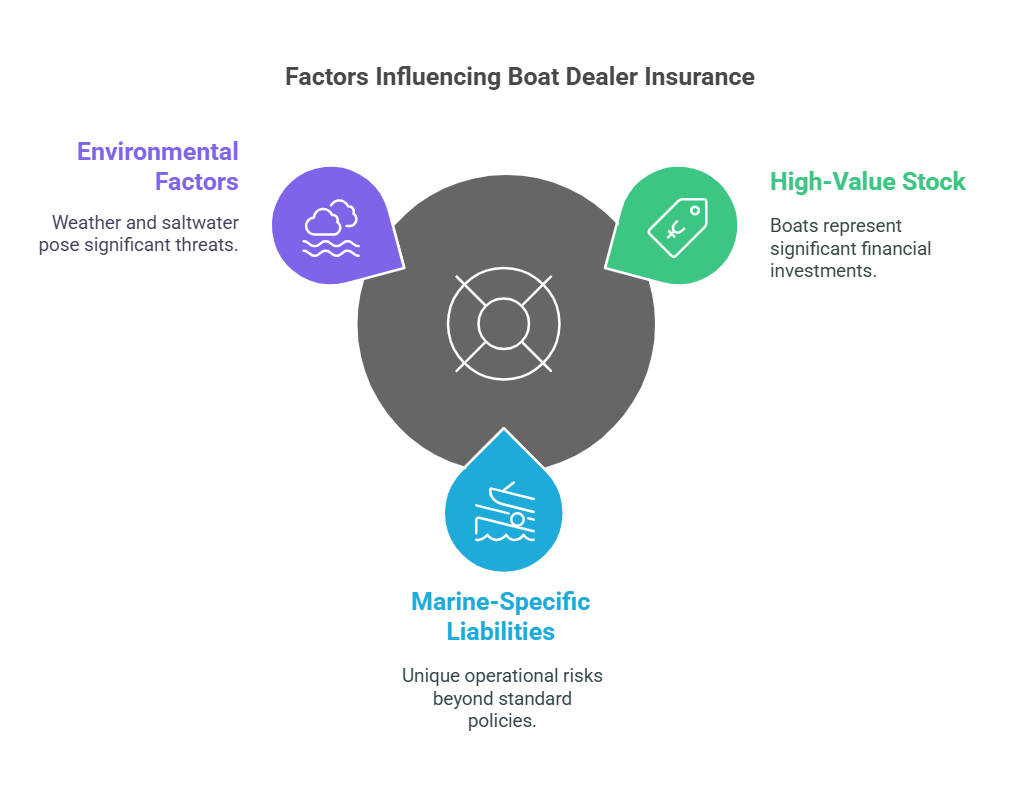

- High-Value Stock

A boat may carry a price tag that dwarfs many common retail items. From a modest fishing craft to a luxury yacht, each vessel represents a substantial investment. Losing multiple boats in a single catastrophic event can devastate your balance sheet if you don’t have the correct policy in place. - Marine-Specific Liabilities

Boat dealerships don’t merely stock goods in a warehouse. They often transport inventory, hold test drives on open water, and work with complex mechanical systems that occasionally fail in unpredictable ways. Each of these scenarios introduces extra layers of exposure that a typical business policy might gloss over. - Environmental Factors

Hurricanes, floods, and even routine storms can inflict extreme damage on boats, especially if they’re stored outdoors. Salt air accelerates corrosion, while freshwater floods can render engines and electronics useless. A specialized insurance plan aims to manage these unique hazards before they wipe out your business.

Below is a concise table comparing conventional business coverage with boat dealership-specific insurance:

| Coverage Aspect | Standard Business Policy | Specialized Boat Dealer Insurance |

| Inventory Focus | Typically excludes watercraft or limits by length | Covers a broad range of vessels in transit or storage |

| Environmental Hazards | Basic protection (fire, wind) | Tailored for flood, hurricane, corrosion, and salt damage |

| Demo Ride Liability | Often not included | Specifically covers sea trials and water-based testing |

| Marine Equipment | May not insure specialized docks or hoists | Extends to slips, lifts, engine hoists, and other maritime equipment |

Required Coverage Types for Boat Dealers

When planning your insurance portfolio, you’ll likely spot several coverage categories that interlock to form a robust safety net. While the exact bundle varies based on location, inventory size, and operational style, a few policy types generally stand as indispensable.

Property and Inventory Coverage

Overview

Property coverage goes well beyond the building where you greet customers. For a boat dealer, it often includes storage racks, docks, specialized equipment, and of course, the boats themselves. Whether you keep a flotilla of smaller day cruisers or a handful of million-dollar yachts, ensuring they’re adequately insured can spell the difference between a temporary setback and bankruptcy if disaster strikes.

Key Features

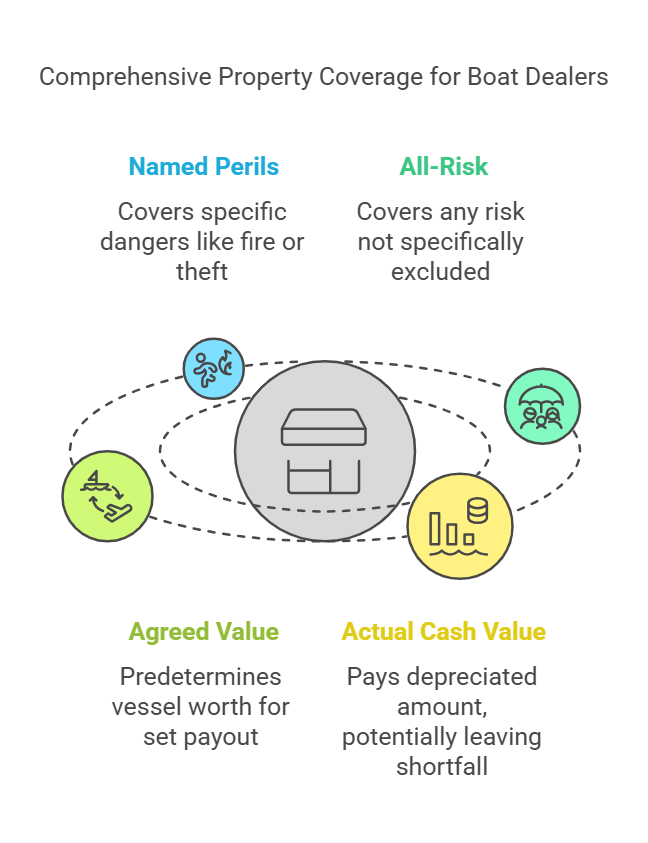

- Named Perils vs. All-Risk

- Named Perils: This approach covers specific dangers, like fire or theft, explicitly listed in the policy.

- All-Risk: Broader, covering any risk not specifically excluded.

- Agreed Value vs. Actual Cash Value

- Agreed Value: Predetermines the worth of each vessel, ensuring you receive a set payout.

- Actual Cash Value: Pays the depreciated amount, which might leave you short if a brand-new boat gets damaged.

Real-World Example

A dealer in the Gulf region—where hurricanes roar with little warning—suffered the loss of a small fleet due to storm surge. While the building’s primary insurance covered interior damage, the biggest relief came from a specialized marine property policy. It compensated for the waterlogged hulls and rendered electronics that were stacked in a nearby outdoor staging area.

General Liability

Overview

General liability addresses the broad array of accidents that can occur on your dealership’s property or because of your business operations. Someone might trip over a coil of rope in your showroom. A forklift driver might accidentally knock a boat off its stand, damaging a customer’s car parked nearby. These incidents can be wildly expensive if your coverage isn’t designed to absorb such hits.

Coverage Points

- Third-Party Bodily Injury: Pays for medical expenses and legal fees if a customer or visitor gets hurt on your premises.

- Property Damage: Handles incidents where dealership activities damage someone else’s property—like a fender bender involving a forklift.

- Legal Fees and Settlements: Offers defense if you face lawsuits alleging negligence or unsafe conditions.

Marine Floater Policy

Overview

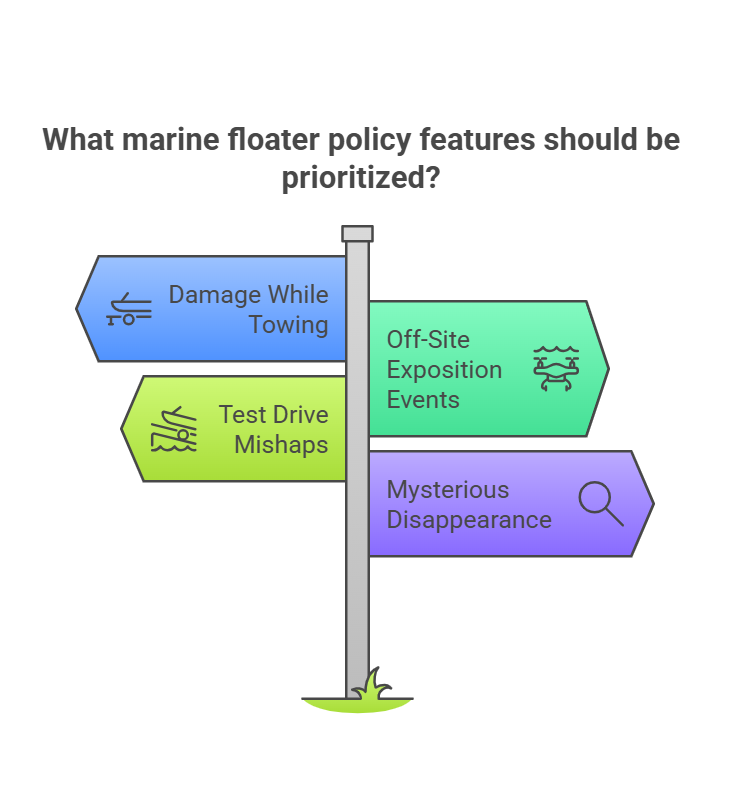

Marine floater coverage is your best friend for boats in transit. If your dealership frequently shuttles vessels between storage facilities, boat shows, or customers’ docks for demos, you want a policy that travels with them.

What It Typically Covers

- Damage While Towing: If you’re hauling boats on trailers and something goes wrong.

- Events at Off-Site Expositions: Theft or vandalism at a boat show can create havoc unless you have extended coverage.

- Test Drive Mishaps: Collisions, groundings, or engine damage occurring while clients are evaluating a prospective purchase.

Bullet Points for Consideration

- Choose coverage that accounts for “mysterious disappearance,” a polite insurance term for thefts that leave few clues.

- Verify whether your policy limits shift when a vessel is stored at a customer’s location overnight or over a weekend.

Additional Insurance Considerations

Professional Liability (Errors & Omissions)

Professional liability can seem like an afterthought, but the moment a claim arises about misinformation—like exaggerated fuel efficiency or misstated engine horsepower—this coverage becomes a game-changer. Especially if your team provides consultative advice on boat modifications, financing arrangements, or extended warranties, any error could land you in a pricey dispute.

Scenarios to Think About

- A customer alleges they purchased a boat based on misleading details regarding maximum passenger capacity.

- Someone sues over improper guidance on how to winterize a vessel, leading to engine failure in the spring.

Workers’ Compensation

The marine environment can be risky for employees. Whether they’re climbing scaffolding to manage inventory or balancing on slippery decks, one misstep can cause a serious injury. Workers’ compensation covers medical bills, rehabilitation costs, and a portion of lost wages if an employee gets hurt on the job.

Risk Factors

- Heavy lifting of engines or rigging equipment

- Operating forklifts and hoists near water

- Performing mechanical tasks in tight, awkward areas

Business Interruption Coverage

Imagine a scenario where your main office and display area become uninhabitable after a severe storm. You not only lose potential sales, but you also must keep paying your staff and rent on the property. Business interruption coverage steps in to compensate for the income you miss out on during recovery, ensuring you can pay bills, maintain your workforce, and keep your business afloat—both literally and figuratively.

Cyber Liability

Boat dealerships increasingly rely on digital platforms, online inventory management, and electronic payments. Hackers, ransomware, and phishing schemes pose real threats. A robust cyber liability policy can help with the fallout from data breaches, including legal notifications to affected customers and potential settlement costs if personal information gets compromised.

Table: Key Coverage Add-Ons

| Coverage Type | Primary Benefit | Potential Risks Without It |

| Professional Liability | Helps resolve claims of misrepresentation | Costly lawsuits, reputation damage |

| Workers’ Compensation | Covers staff injuries and lost wages | Major out-of-pocket expenses, possible legal violations |

| Business Interruption | Replaces lost income during mandatory shutdowns | Inability to pay fixed costs, potential layoffs |

| Cyber Liability | Covers data breach costs and cyberattack recovery | Customer data lawsuits, ruinous system downtime |

Risk Management for Boat Dealers

Insurance is a vital piece of the puzzle, but preventing claims before they happen can keep your premiums manageable and your operations humming. A proactive strategy merges robust safety measures with staff training and thorough record-keeping.

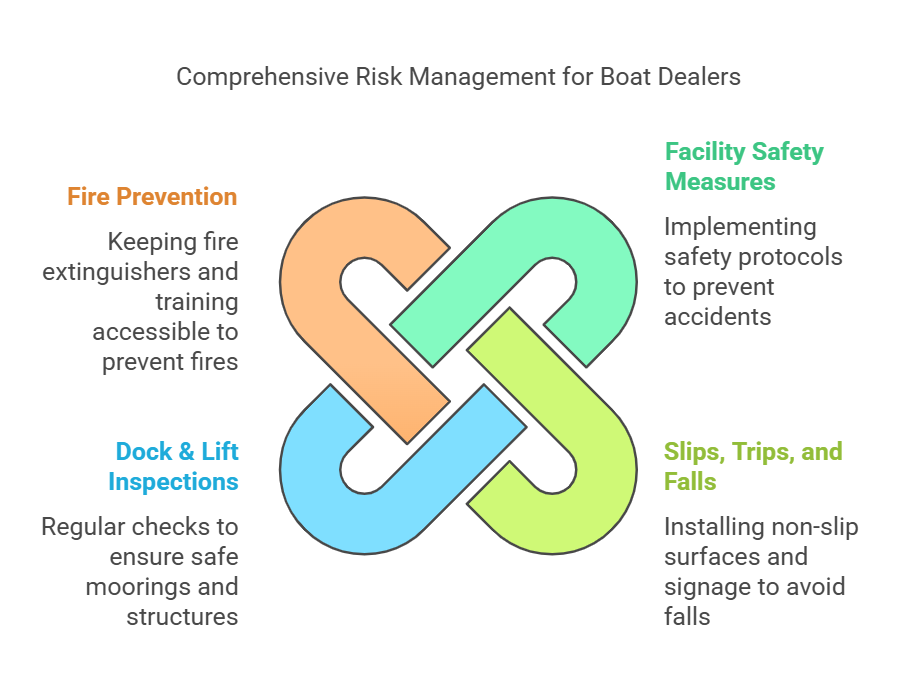

Facility Safety Measures

- Slips, Trips, and Falls

Install non-slip mats, ensure adequate lighting, and add prominent signage for wet floors or low-clearance areas. Even a minor misstep can bring a costly lawsuit. - Dock & Lift Inspections

Regularly inspect moorings, docks, and lifts. Corroded cables or compromised structures can cause extensive damage to boats and humans alike. - Fire Prevention

Where there are engines, there’s a risk of sparks. Keep fire extinguishers accessible, update your alarm systems, and train employees in basic fire response.

Demo Ride Precautions

Customers eager to take a boat for a spin on open water introduce all sorts of unpredictable dynamics. Reduce risk with clear guidelines:

- Mandatory Safety Gear: Life jackets for everyone on board, along with functioning emergency signals or flares.

- Check the Weather: A sudden squall can catch even seasoned boaters off guard. Establish a rule to halt demo rides when conditions get dicey.

- Signed Waivers: A simple but powerful document clarifying the potential risks and releasing your dealership from certain liabilities if the unexpected occurs.

Documentation and Record-Keeping

In the event a claim does arise, thorough records can be your lifeline:

- Boat Service Logs: Detailed entries on any maintenance or repairs.

- Incident Reports: Comprehensive forms that capture injuries or damage, even if they seem trivial at first glance.

- Staff Training Records: Proof that employees received marine safety or forklift training can substantially reduce your liability in a lawsuit.

Selecting the Right Insurance Provider

All coverage is not equal. Insurance carriers with little experience in marine markets might not grasp the nuances of boat dealer insurance—leading to coverage gaps or messy claim disputes when disaster strikes.

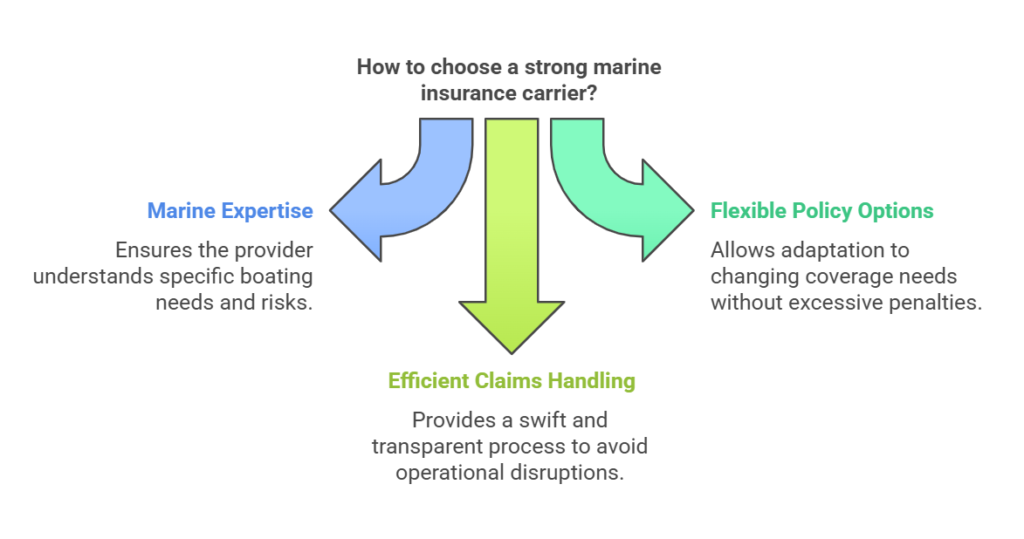

Traits of a Strong Marine Insurance Carrier

- Marine Expertise

Look for providers that have a track record in the boating industry. They should understand the difference between a pontoon and a trawler, as well as the unique exposures each carries. - Flexible Policy Options

Your coverage needs may evolve. If you expand from 10 vessels to 50, or if you add a second waterfront property, your carrier should accommodate these shifts without penalizing you excessively. - Efficient Claims Handling

A swift and transparent claims process can spare you countless headaches. Check reviews or ask for references. If an insurer often drags claims out for months, it could disrupt your entire operation.

Red Flags

- Overly Generic Policies

A plan that looks suspiciously broad might mean it lacks crucial marine riders or sub-limits. - Poor Communication

If your agent can’t promptly explain coverage details, that confusion may double during a claim. - No Reference to Environmental Risk

Floods, hurricanes, or even routine storms are part of a boat dealer’s world. Ignoring them in policy documents signals a red-flag oversight.

Cost Factors and Premium Management

Getting the right insurance isn’t about shelling out money blindly. There are strategic ways to keep costs manageable while securing robust protection.

Premium Influencers

- Geographic Location

Coastal dealerships typically face higher premiums due to hurricanes, corrosion risks, and storm surge exposure. Inland operations might see lower rates but could face flood risks near major rivers. - Inventory Value and Composition

Stocking a handful of small fishing boats is one thing; a collection of luxury yachts worth millions of dollars each is another. The higher your overall inventory value, the higher the premium. - Claims History

A spotless record can help you negotiate favorable rates. Multiple claims over a short period often trigger surcharges or policy restrictions.

Strategies for Cost Reduction

- Bundle Coverages

Many insurers reward you with reduced rates when you combine multiple lines—like general liability, property insurance, and auto coverage—under one provider. - Enhanced Security Measures

Installing robust surveillance systems, alarm-triggered locks, or GPS trackers on high-value boats can slash theft-related premiums. - Staff Training Programs

A well-trained workforce that follows safety protocols is less likely to cause accidents, giving insurers confidence and often leading to lower rates. - High Deductibles

Taking on a slightly higher deductible means you assume a bit more risk, but it can noticeably reduce your monthly or annual premium.

Claims Process and Management

When calamity strikes—be it a theft, a storm-related event, or an accident during a test run—the claims process becomes your focal point. Handling it methodically can expedite settlement and prevent drawn-out disputes.

Steps for Streamlined Claims

- Immediate Damage Control

Protect the damaged boat or property from further harm. Document the situation with clear photos or video, noting the date and extent of any destruction. - Notify Your Insurer Promptly

Quick reporting lays the groundwork for a smoother process. Some policies impose strict reporting windows, and missing them can jeopardize your claim. - Collect Evidence

If it’s an incident on the water, gather witness statements. For a fire or theft, compile police or fire department reports. - Engage in Dialogue

Maintain open communication with the claims adjuster. If the initial settlement offer seems inadequate, gather repair estimates or third-party appraisals to bolster your case. - Final Resolution

Once you agree on a payout, confirm that all relevant expenses—like towing, storage, or environmental clean-up—are included before finalizing.

Pro Tip for Large Claims

If you’re dealing with a high-stakes incident—like widespread damage to a fleet—a public adjuster might be worth considering. They advocate on your behalf (not the insurer’s) and can help ensure you receive the maximum claim settlement. Although they take a fee, they can offset that cost by uncovering coverages or amounts you might otherwise miss.

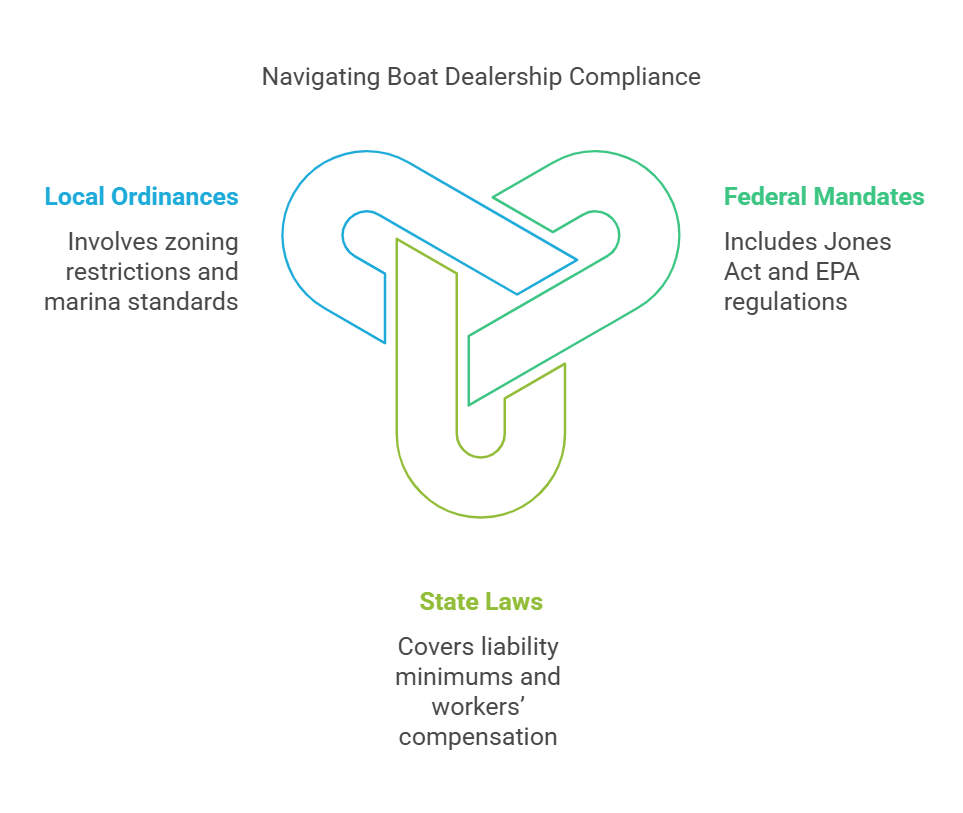

Legal Requirements and Compliance

Aside from smart business practices, you must also meet federal, state, and local regulations regarding boat dealer operations and insurance levels.

Federal Mandates

- Jones Act

If your dealership operates its own vessels or employs crew for transport, be aware of possible maritime worker protection requirements. - EPA Regulations

Spills or discharges could trigger environmental penalties. Keep proper pollution coverage and follow disposal guidelines for oil, fuel, and other fluids.

State Laws

- Liability Minimums

Some coastal states demand a minimum liability threshold—such as $300,000 or $1 million—when vessels are part of your inventory. - Workers’ Compensation

Almost every state enforces worker protection requirements if you have employees, though specifics differ widely.

Local Ordinances

- Zoning Restrictions

Local guidelines might limit where you can store boats or how you manage fuel. - Marina and Dock Standards

Regional agencies often have rules about docking structures, so confirm your property meets relevant codes.

Failing to meet these obligations can trigger hefty fines or business shutdowns, so it’s prudent to keep up with evolving requirements. A savvy attorney or specialized insurance agent can help align your coverage with all necessary regulations.

Conclusion

The world of boat dealer insurance is a layered tapestry of policies, best practices, and proactive safety measures. Unlike standard business coverage, a marine-focused approach accounts for environmental volatility, costly watercraft, and the inherent thrill—and risk—of demo rides. The right policy can be the difference between a minor setback and a total operational freeze in the aftermath of a hurricane, flood, lawsuit, or accidental collision.

Start by identifying the biggest vulnerabilities in your dealership. Maybe your location is hurricane-prone, or perhaps you maintain an immense inventory of high-end vessels that need all-risk coverage. Next, verify that you have robust liability protection—both general and professional—to handle everything from slip-and-fall accidents to allegations of misrepresentation. Don’t forget about transporting boats or offering test drives on the water. A specialized floater policy can safeguard you from financial ruin should an unexpected event derail your plans.

Equally crucial is having a solid risk management program. A well-run operation makes you more attractive to insurance providers, often resulting in more comprehensive coverage at better rates. Simple, consistent practices like conducting regular dock checks, implementing staff safety training, and diligently tracking boat repairs or modifications can work wonders to prevent mishaps.

Finally, choose your insurance provider wisely. Seek a carrier that genuinely comprehends the marine space—one that can expedite claims, offer flexible coverage as your dealership expands, and provide options that align with your region’s regulatory demands. Keep a sharp eye for red flags: vague policy wording, unclear limitations, or a history of glacially slow claim payouts. In short, look for a partner with both maritime know-how and an eagerness to tailor coverage to your evolving needs.

In the unpredictable intersection of water, weather, and business, preparedness reigns supreme. From covering luxurious yachts to safeguarding simpler fishing boats, from ensuring demo rides to defending against cyber threats, your dealership thrives on layers of protection. Equipped with comprehensive boat dealer insurance, you can face the open water of commerce with confidence, ready to navigate any squall—literal or figurative—that might come your way.